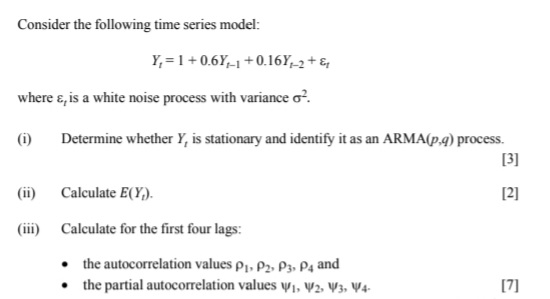

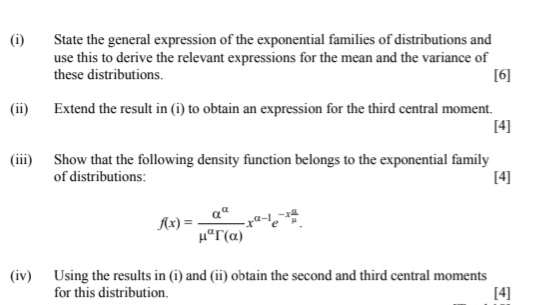

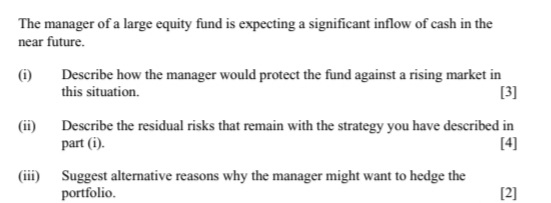

Question

Correct ones please. 1 An investor measures the utility of her wealth using the utility function U(w) = ln(w) for w > 0. (i) Derive

Correct ones please.

1 An investor measures the utility of her wealth using the utility function U(w) = ln(w)

for w > 0.

(i) Derive the absolute and relative risk aversions for this investor's utility

function, and the first derivative of each. [4]

(ii) Comment on what this tells us about the proportion of her assets that this

investor will invest in risky assets. [2]

The investor has 100 available to invest in two possible assets, Asset A and Asset B.

The future value of Asset A depends on an uncertain future event.Every 1 invested in Asset A will be worth 1.30 with probability 0.75 and 0.40

with probability 0.25.

Asset B is risk-free, so every 1 invested in Asset B will always be worth 1.

The investor does not discount future asset values when making investment decisions.

She decides to invest a proportion a of her wealth in Asset A and the remaining

proportion 1 - a in Asset B.

(iii) Express her expected utility of wealth in terms of a. [2]

(iv) Determine the amount that she should invest in each of Asset A and B to

maximise her expected utility, using your result from part (iii).

2.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

What Every Environmentalist Needs To Know About Capitalism

Authors: Fred Magdoff, John Bellamy Foster

1st Edition

1583672419, 9781583672419