Answered step by step

Verified Expert Solution

Question

1 Approved Answer

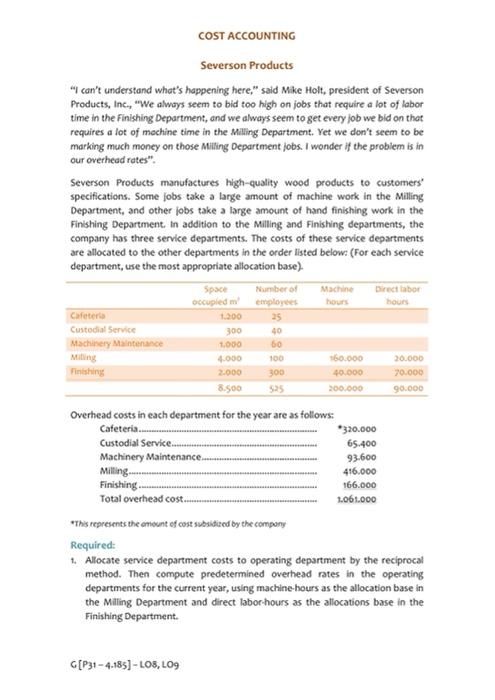

COST ACCOUNTING Severson Products I can't understand what's happening here, said Mike Holt, president of Severson Products, Inc., We always seem to bid too high

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Lease Audits The Essential Guide

Authors: Theodore H Hellmuth

1st Edition

0934055041, 978-0934055048