Answered step by step

Verified Expert Solution

Question

1 Approved Answer

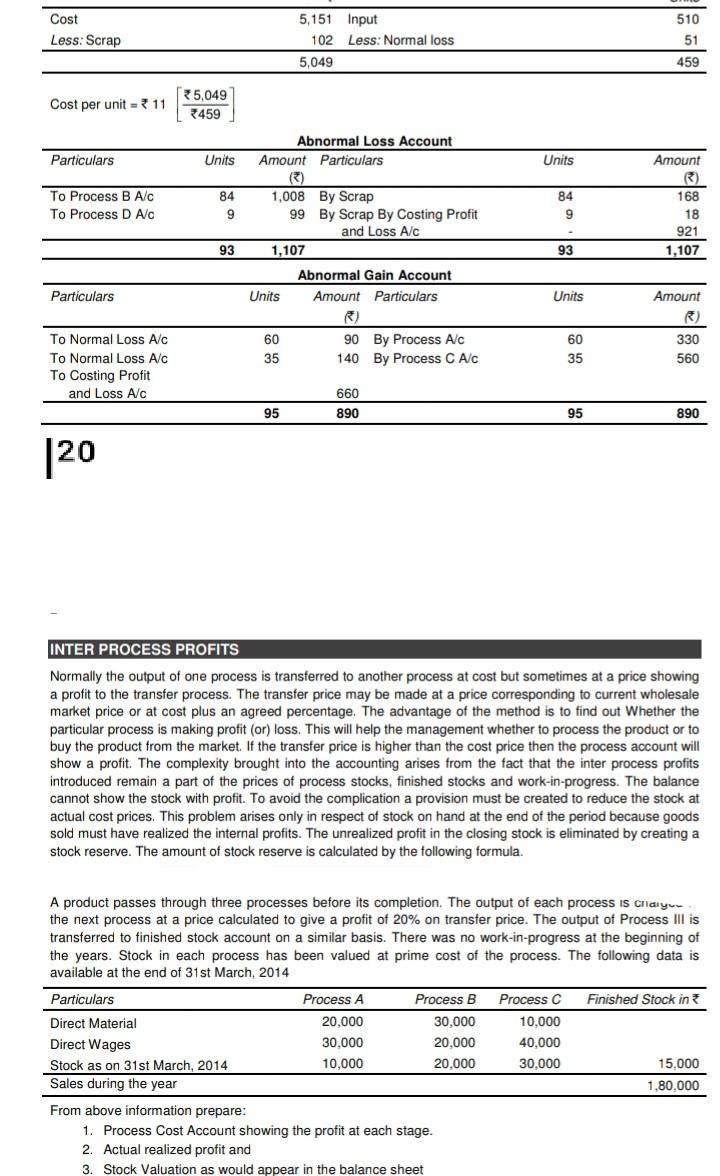

Cost Less: Scrap 5,151 Input 102 Less: Normal loss 5,049 510 51 459 Cost per unit = 11 5,049 3459 Particulars Units Units Amount To

Cost Less: Scrap 5,151 Input 102 Less: Normal loss 5,049 510 51 459 Cost per unit = 11 5,049 3459 Particulars Units Units Amount To Process B A/C To Process D A/C 84 9 Abnormal Loss Account Amount Particulars () 1.008 By Scrap 99 By Scrap By Costing Profit and Loss A/C 1.107 84 9 168 18 921 1,107 93 93 Abnormal Gain Account Amount Particulars Particulars Units Units Amount R 330 560 60 35 90 By Process A/C 140 By Process C A/C 60 35 To Normal Loss Alc To Normal Loss A/C To Costing Profit and Loss A/C 660 890 95 95 890 390 120 INTER PROCESS PROFITS Normally the output of one process is transferred to another process at cost but sometimes at a price showing a profit to the transfer process. The transfer price may be made at a price corresponding to current wholesale market price or at cost plus an agreed percentage. The advantage of the method is to find out whether the particular process is making profit (or) loss. This will help the management whether to process the product or to buy the product from the market. If the transfer price is higher than the cost price then the process account will show a profit. The complexity brought into the accounting arises from the fact that the inter process profits introduced remain a part of the prices of process stocks, finished stocks and work-in-progress. The balance cannot show the stock with profit. To avoid the complication a provision must be created to reduce the stock at actual cost prices. This problem arises only in respect of stock on hand at the end of the period because goods sold must have realized the internal profits. The unrealized profit in the closing stock is eliminated by creating a stock reserve. The amount of stock reserve is calculated by the following formula. A product passes through three processes before its completion. The output of each process is Chaty the next process at a price calculated to give a profit of 20% on transfer price. The output of Process III is transferred to finished stock account on a similar basis. There was no work-in-progress at the beginning of the years. Stock in each process has been valued at prime cost of the process. The following data is available at the end of 31st March, 2014 Particulars Process A Process B Process C Finished Stock in Direct Material 20,000 30,000 10.000 Direct Wages 20,000 40,000 Stock as on 31st March, 2014 10,000 20,000 30,000 15.000 Sales during the year 1,80,000 30.000 From above information prepare: 1. Process Cost Account showing the profit at each stage. 2. Actual realized profit and 3. Stock Valuation as would appear in the balance sheet

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Auditing Issues And Cases

Authors: Michael Chris Knapp

3rd Edition

0538891173, 9780538891172