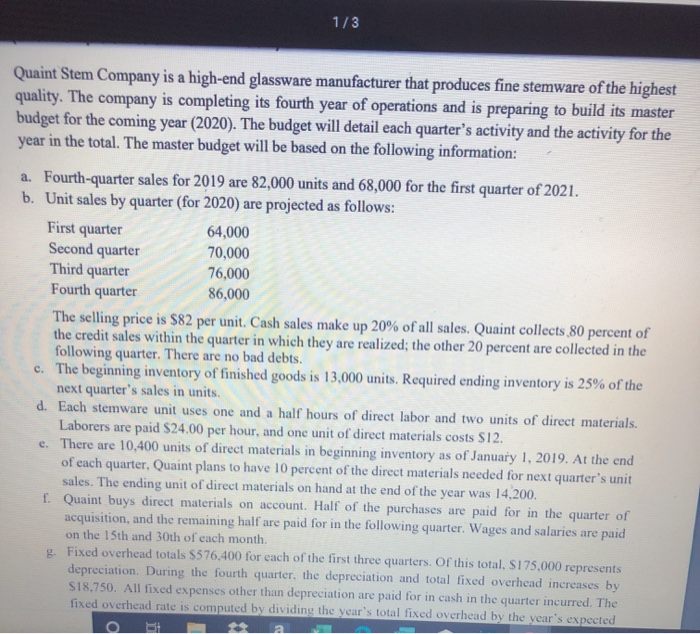

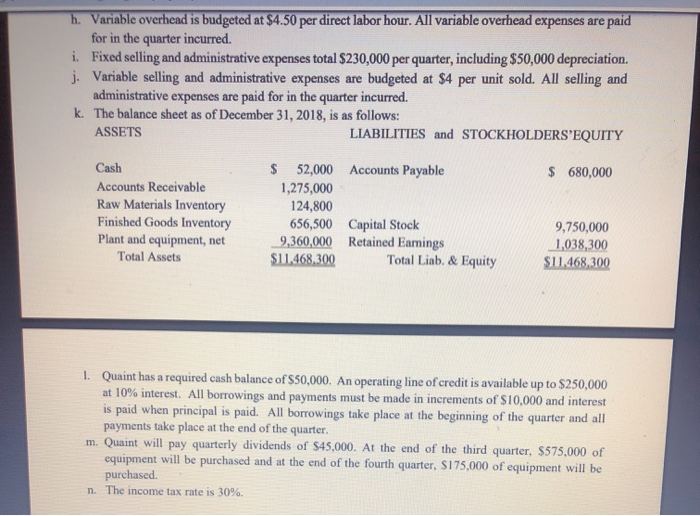

Cost of Goods Sold Budget Quarter 3 Year 67 68 69 Direct materials used 70 Direct labor used 71 Overhead 72 Budgeted manufacturing costs 73 Beginning finished goods 74 Cost of goods available for sale 75 Less: Ending finished goods 76 Budgeted cost of goods sold Selling and Administrative Budget Quarter Year 81 Planned sales in units 82 Variable selling and admin exp per unit 83 Total variable expense 84 Fixed selling and admin expense 85 Total selling and admin expenses 87 Note: depreciation in fixed selling and admin expense 1/3 Quaint Stem Company is a high-end glassware manufacturer that produces fine stemware of the highest quality. The company is completing its fourth year of operations and is preparing to build its master budget for the coming year (2020). The budget will detail each quarter's activity and the activity for the year in the total. The master budget will be based on the following information: a. Fourth-quarter sales for 2019 are 82,000 units and 68,000 for the first quarter of 2021. b. Unit sales by quarter (for 2020) are projected as follows: First quarter 64,000 Second quarter 70,000 Third quarter 76,000 Fourth quarter 86,000 The selling price is $82 per unit. Cash sales make up 20% of all sales. Quaint collects 80 percent of the credit sales within the quarter in which they are realized; the other 20 percent are collected in the following quarter. There are no bad debts. c. The beginning inventory of finished goods is 13,000 units. Required ending inventory is 25% of the next quarter's sales in units. d. Each stemware unit uses one and a half hours of direct labor and two units of direct materials. Laborers are paid $24.00 per hour, and one unit of direct materials costs $12. e. There are 10,400 units of direct materials in beginning inventory as of January 1, 2019. At the end of each quarter. Quaint plans to have 10 percent of the direct materials needed for next quarter's unit sales. The ending unit of direct materials on hand at the end of the year was 14,200. 1. Quaint buys direct materials on account. Half of the purchases are paid for in the quarter of acquisition, and the remaining half are paid for in the following quarter. Wages and salaries are paid on the 15th and 30th of each month. g. Fixed overhead totals S576,400 for each of the first three quarters of this total, S175,000 represents depreciation. During the fourth quarter, the depreciation and total fixed overhead increases by $18.750. All fixed expenses other than depreciation are paid for in cash in the quarter incurred. The fixed overhead rate is computed by dividing the year's total fixed overhead by the year's expected h. Variable overhead is budgeted at $4.50 per direct labor hour. All variable overhead expenses are paid for in the quarter incurred. i. Fixed selling and administrative expenses total $230,000 per quarter, including $50,000 depreciation. j. Variable selling and administrative expenses are budgeted at $4 per unit sold. All selling and administrative expenses are paid for in the quarter incurred. k. The balance sheet as of December 31, 2018, is as follows: ASSETS LIABILITIES and STOCKHOLDERS'EQUITY Accounts Payable $ 680,000 Cash Accounts Receivable Raw Materials Inventory Finished Goods Inventory Plant and equipment, net Total Assets $ 52,000 1,275,000 124,800 656,500 9,360,000 $11.468,300 Capital Stock Retained Earings Total Liab. & Equity 9,750,000 1,038,300 $11.468,300 1. Quaint has a required cash balance of $50,000. An operating line of credit is available up to $250,000 at 10% interest. All borrowings and payments must be made in increments of $10,000 and interest is paid when principal is paid. All borrowings take place at the beginning of the quarter and all payments take place at the end of the quarter. m. Quaint will pay quarterly dividends of $45,000. At the end of the third quarter, $575,000 of equipment will be purchased and at the end of the fourth quarter, S175,000 of equipment will be purchased n. The income tax rate is 30%. Unit production cost for ending inventory budget Direct Materials Direct Labor Variable Overhead Fixed Overhead Total cost per unit Total finished goods at the end of year Total ending finished goods inventory 12.00 24.00 4.50 7.75 48.25 17000 8,20,250 40 last year next year Sales Budget Quarter 2 64,000 70,000 76,000 82 82 5,248,000 5,740,000 6,232,000 4 86,000 9 Units 0 Unit selling price 11 Budgeted sales Year 296,000 82 24,272.000 82 7,052,000 12 13 Production Budget Quarter 68,000 15 16 Sales in units 17 Desired ending inventory 18 Total needs 19 Less: Beginning inventory 20 Units to be produced 21 64,000 17,500 81,500 13,000 68,500 70,000 19,000 89,000 17,500 71,500 76,000 21,500 97 500 19.000 78500 86,000 17,000 103,000 21,500 81,500 Year 296,000 17 000 313,000 13,000 300.000 Direct Materials Purchases Budget Quarter 24 25 Units to be produced 68,500 71,500 Year 20 non 78.500 81 500 Direct Materials Purchases Budget Quarter Year 300,000 68,500 71,500 78,500 81,500 25 Units to be produced 26 Direct materials per unit 27 Production needs 28 Desired ending inventory 29 Total needs 30 Less: Beginning inventory 31 Direct materials to be purchased 32 Cost per unit 33 Total material purchase cost 137,000 14,300 151,300 10,400 140,900 143,000 15,700 158,700 14,300 144,400 157,000 16,300 173,300 15,700 157,600 12 1.891.200 163,000 14,200 177,200 16,300 160,900 M 12 .930.800 600,000 14,200 614,200 10,400 603,800 12 7.245.600 12 1,690,800 1.732.800 1 Direct Labor Budget 36 Quarter 3 78,500 38 Units to be produced 39 Direct labor time per unit in hours 40 Total hours needed 41 Auran wan ner hour 68,500 1.5 102.750 2400 1.5 71,500 1.5 107,250 24.00 Year 300,000 1.5 450,000 81,500 1.5 122,250 24.00 117.750 2400 Direct Labor Budget Quarter 71,500 1.5 38 Units to be produced 39 Direct labor time per unit in hours 40 Total hours needed 41 Average wage per hour 42 Total direct labor cost 68,500 1.5 102,750 24.00 2,486,000 78,500 1.5 117,750 24.00 2.826,000 107 250 24.00 2,574.000 Year 300,000 1.5 450,000 24.00 10,800,000 81,500 15 122,250 24.00 2,934,000 A5 47 Budgeted direct labor hours 48 Variable overhead rate 49 Budgeted variable overhead 50 Budgeted fixed overhead 51 Total overhead Overhead Budget Quarter 3 102,750 107 250 117,750 450 4.50 4.50 462,375 482,625 529,875 576,400 576,400 576.400 1,038,775 1059 025 1,106,275 122,250 4.50 550,125 595 150 1.145 275 Year 450,000 4.50 2,025,000 2,324 350 4 349 350 52 53 Note depreciation in foed overhead