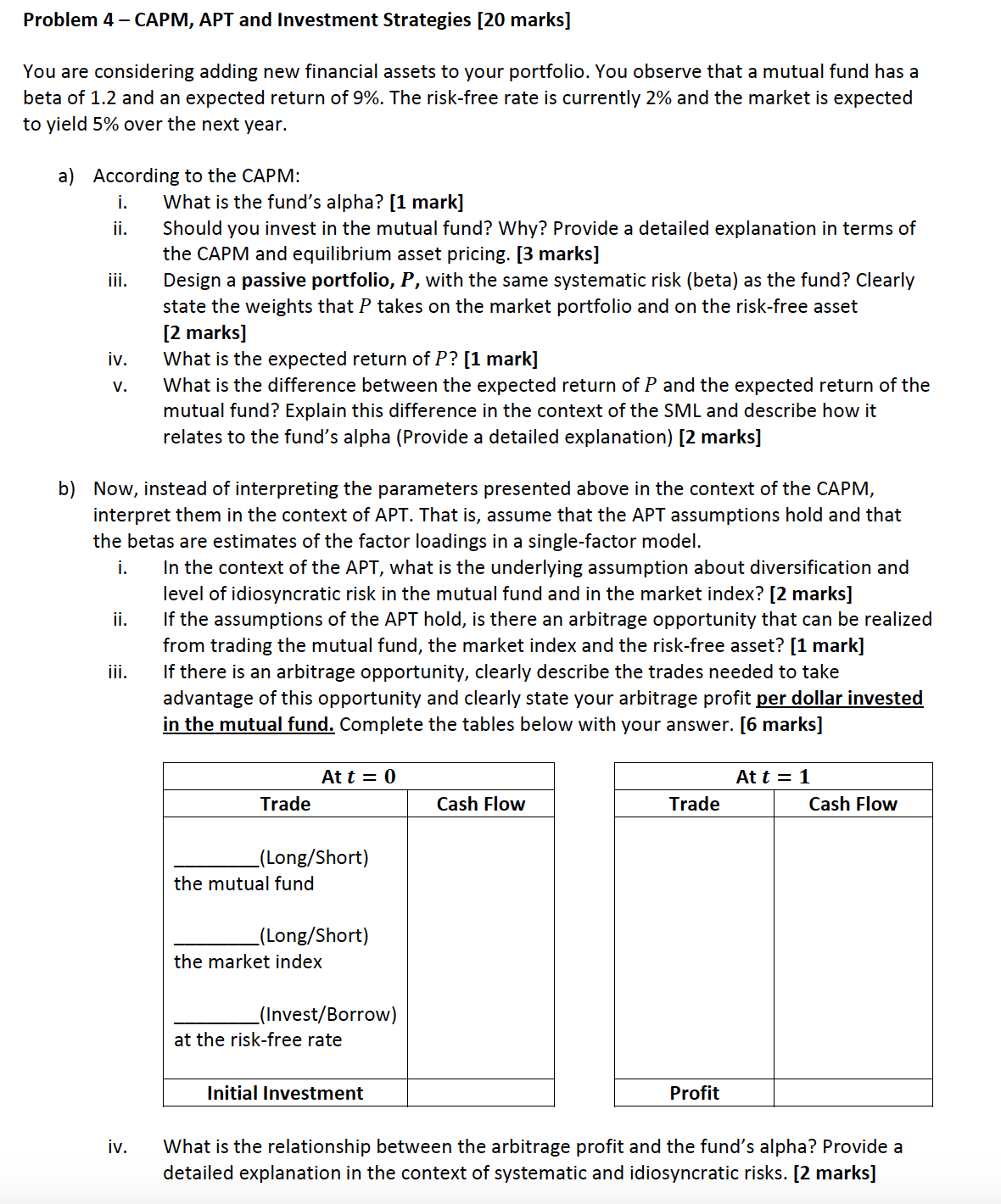

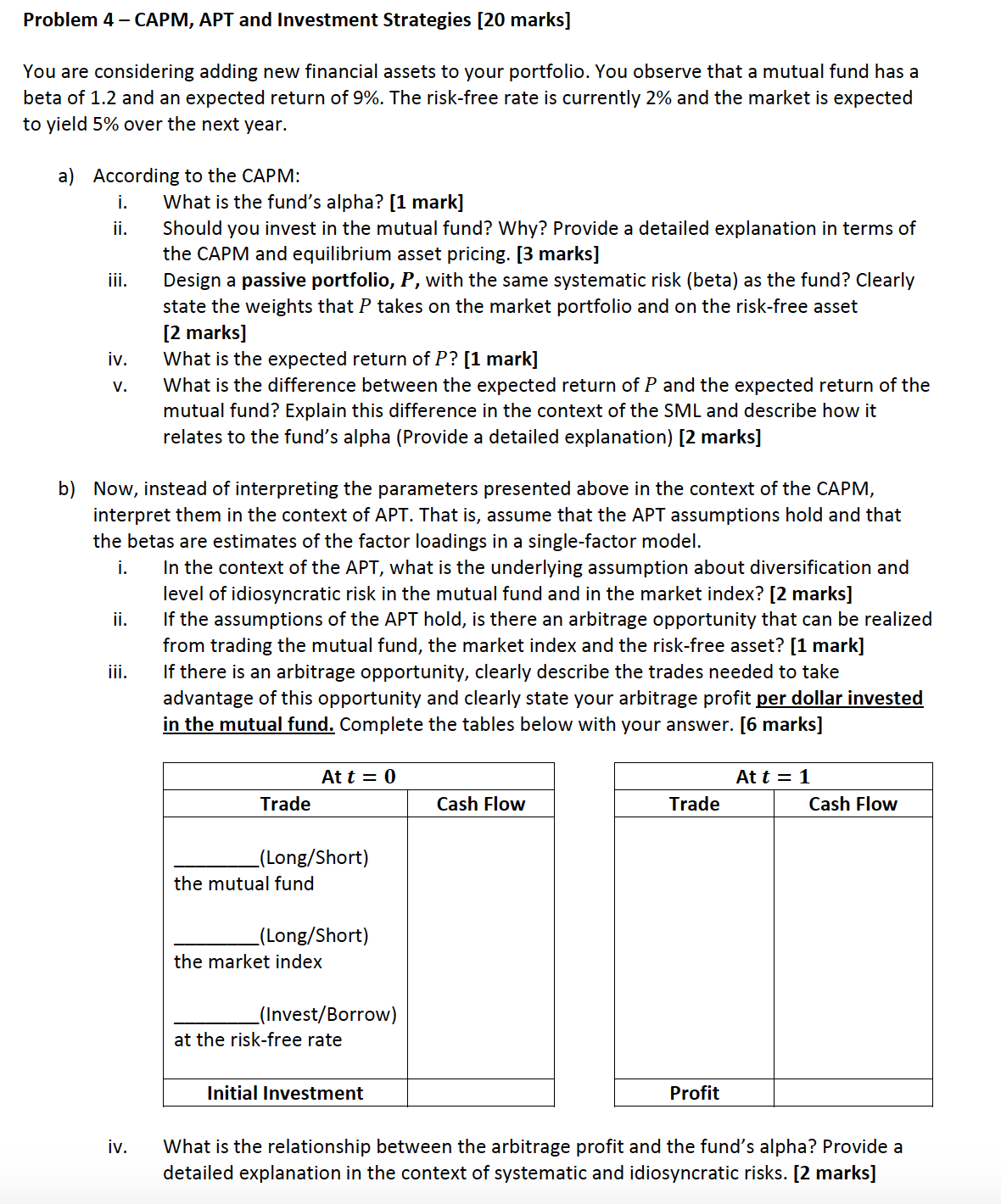

Question

Could someone help me with b)? The answer for a) is: (A) Given, Beta of mutual fund: 1.5 Expected Return of mutual fund: 9% Risk

Could someone help me with b)?

The answer for a) is: (A)

Given,

Beta of mutual fund: 1.5

Expected Return of mutual fund: 9%

Risk free rate 1%

Market Return 5%

1) Fund's Alpha

Alpha = Expected return - CAPM return

CAPM return = risk free rate + Beta (Market return - risk free

return)=0.01 + 1.5*(0.05-0.01)

CAPM return = risk free rate + Beta (Market return - risk free

return)=0.01 + 1.5*(0.05-0.01) 7.00%

Alpha = 9% - 7% = 2%

2) Yes, we should invest in a fund as it is generating positive

alpha that means it is generating returns higher than the systematic risk

involved in the fund due to superior investing.

3) Passive portfolio

As passive portfolio is a porfolio based on market index. Beta

of such passive portfolio invested 100% in the market is 1. The required beta

of the mutual fund is 1.5 so this portfolio needs to be invested more in market

by borrowing at risk free rate.

So to get the beta of 1.5 foloowing weights are required:

150% on market portfolio

-50% on riskfree asset

4) Return on passive portfolio

Return = 1.5*(5%) -0.5*(1%) = 7%

5) Difference between the returns:

Difference = Expected return on mutual fund - Expected Return on

passive fund = 9% - 7% = 2%

This difference arises because mutual fund is generating higher

return than the systematic return undertaken because of positive alpha but the

passive fund is just generating the required return according to the level of

the systematic risk undertaken.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments Analysis and Management

Authors: Charles P. Jones

12th edition

978-1118475904, 1118475909, 1118363299, 978-1118363294