Answered step by step

Verified Expert Solution

Question

1 Approved Answer

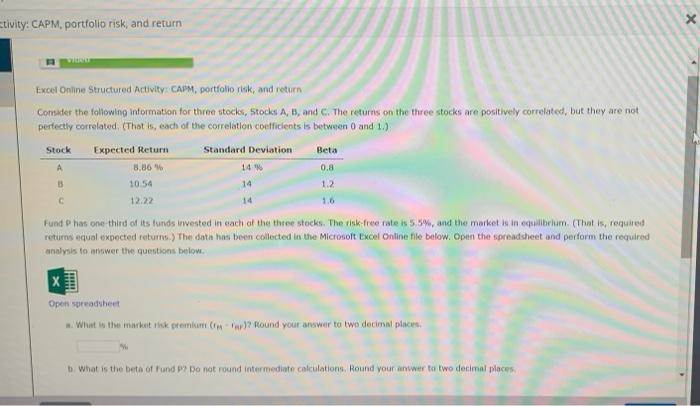

could use some help please. thank you! stivity: CAPM, portfolio risk, and return Excel Online Structured Activity: CAPM, portfolio risk, and return Consider the following

could use some help please. thank you!

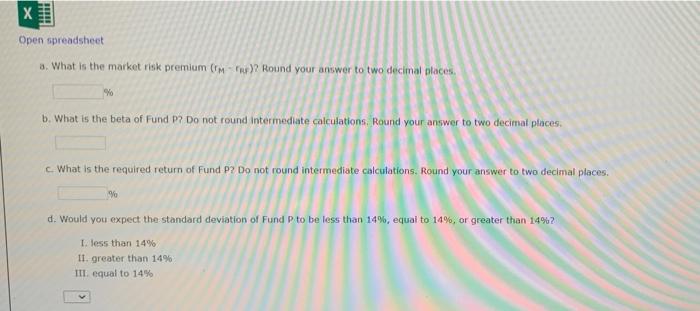

stivity: CAPM, portfolio risk, and return Excel Online Structured Activity: CAPM, portfolio risk, and return Consider the following information for three stocks, Stock A, B, and C. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) Stock A Expected Return 8.86 10:54 12.22 Standard Deviation 14 14 Beta 0.8 1.2 1.6 B 14 Fund has one third of its funds invested in each of the three stocks. The risk-free rate is 5,5%, and the market is in equilibrium. (That is required returns equal expected returns.) The data has been collected in the Microsoft Excel Online file below. Open the spreadsheet and perform the required analysis to answer the questions below. TH Open spreadsheet Winto the marketisk premium Cm ? Round your answer to two decimal places What is the beta of Fund ? Do not found intermediate calculations, Round your awer to two decimal places TH X Open spreadsheet 3. What is the market risk premium M.)? Round your answer to two decimal places b. What is the beta of Fund P? Do not round Intermediate calculations. Round your answer to two decimal places. c. What is the required return of Fund P? Do not round intermediate calculations. Round your answer to two decimal places. 9 d. Would you expect the standard deviation of Fund P to be less than 14%, equal to 14%, or greater than 14%2 1. less than 14% II. greater than 14% III equal to 14% Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Global Finance At Risk

Authors: S. Sen

1st Edition

1349420492, 978-1349420490