Could you help me to do an exercise with data at the choice of a company following the requests of the previous sheets? Mc Donald's

Could you help me to do an exercise with data at the choice of a company following the requests of the previous sheets?

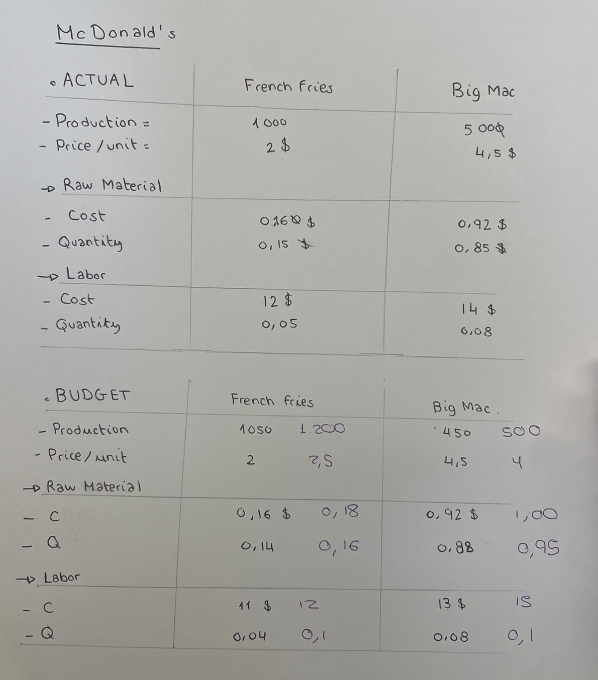

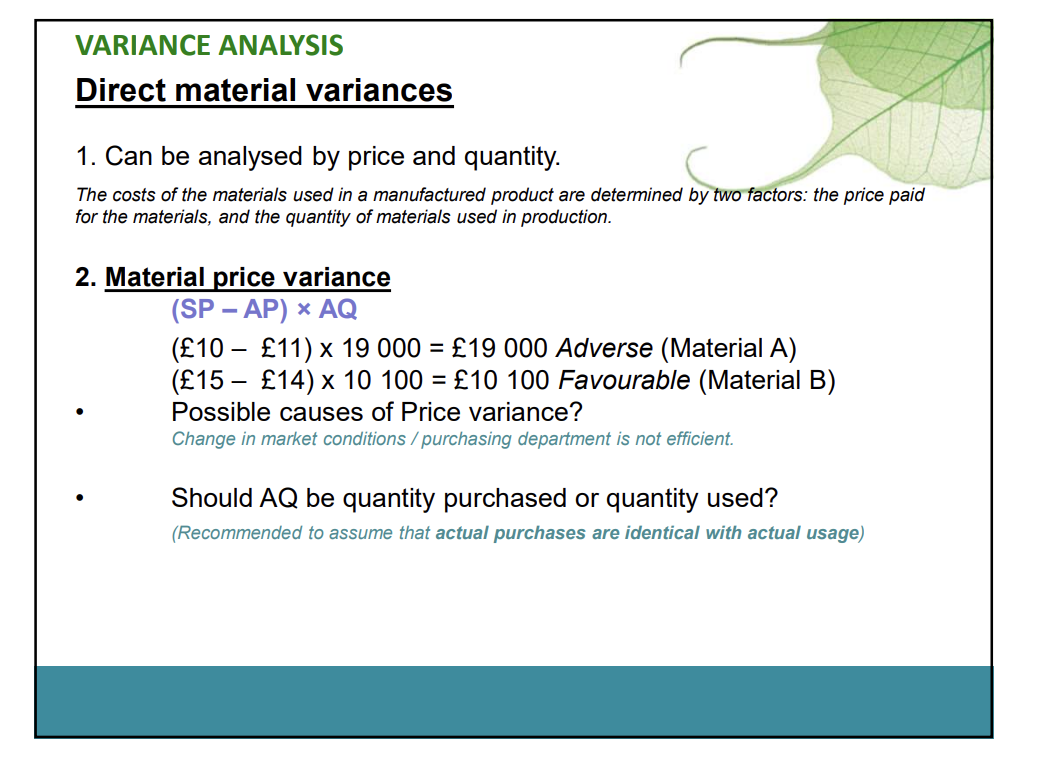

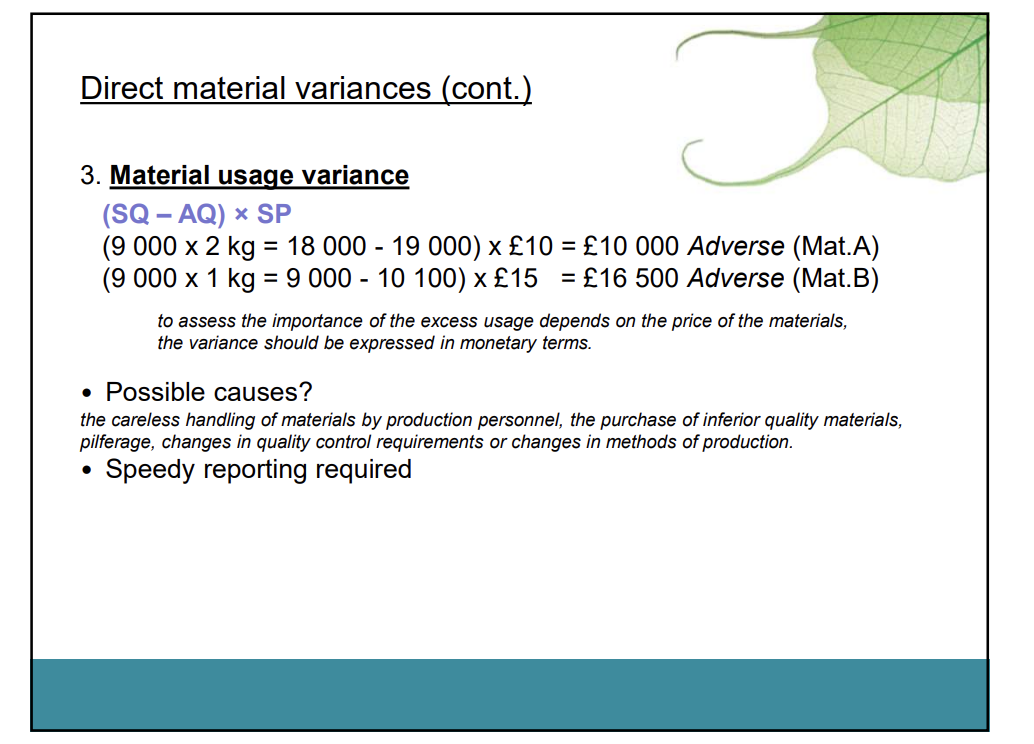

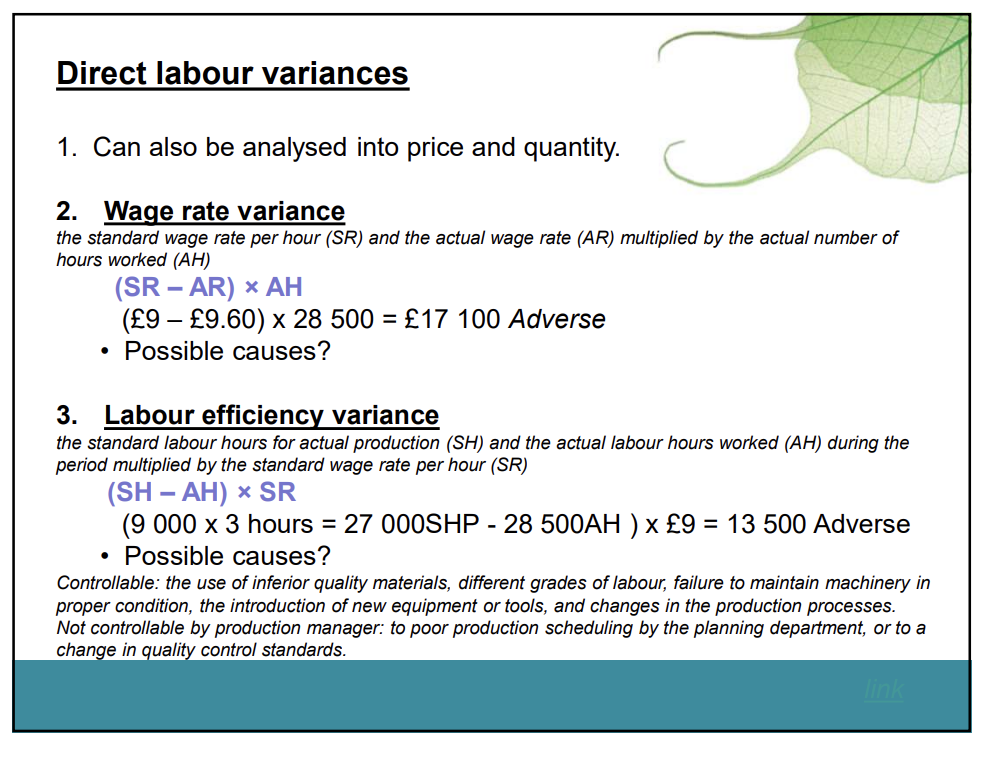

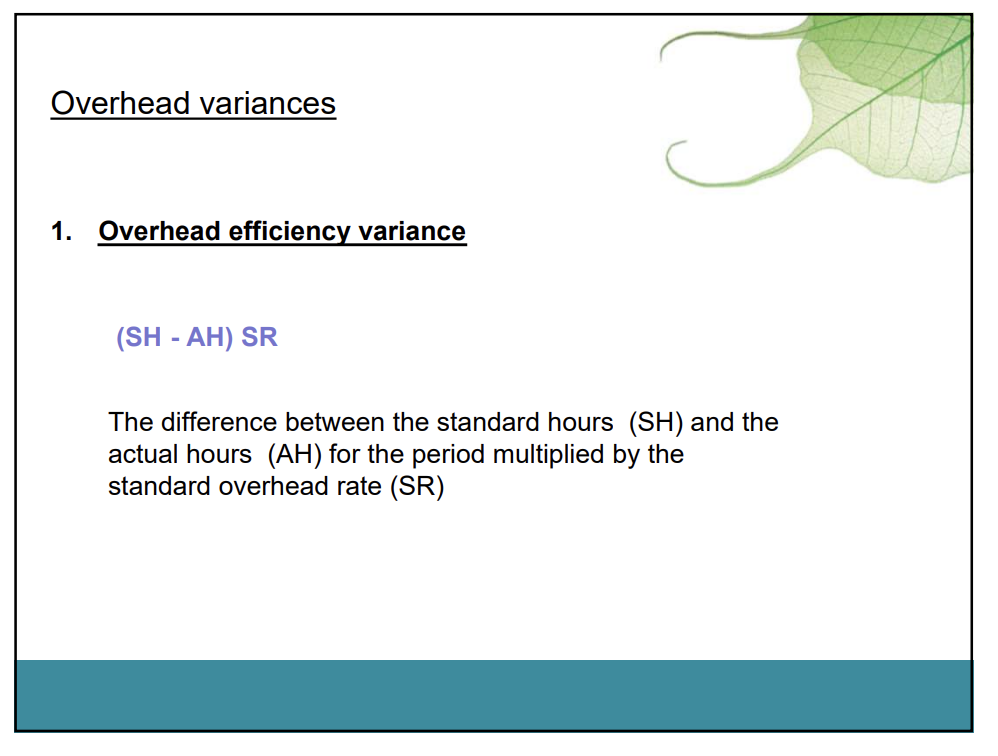

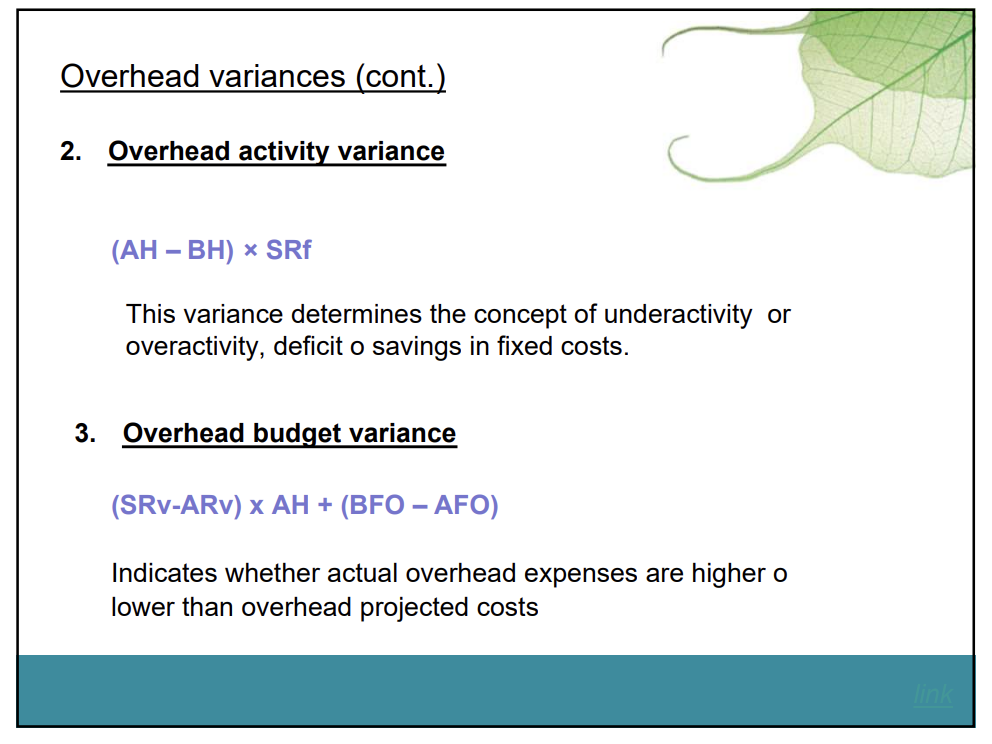

Mc Donald's ACTUAL French Fries Big Mac - Production = 1 000 5 ood - Price / unit = 2 4 4, 5 $ Raw Material - Cost 0 160 $ 0/ 92 1 - Quantity 0, 15 + O, 85 4 - Labor - Cost 12 $ - Quantity 14 $ 0, 05 6108 BUDGET French Fries Big Mac - Production 1050 1. 200 . 450 SOO - Price / unit 2 2, 5 4 5 4 Raw Material C 0, 16 $ 0, 18 0. 92 t 1/00 - 0, 14 0, 16 O, 8% 0,95 -> Labor - C 41 4 12 13 $ IS 0/04 0108VARIANCE ANALYSIS Direct material variances 1. Can be analysed by price and quantity. The costs of the materials used in a manufactured product are determined by\"two factors the price paid for the materials, and the quantity of materials used in production. 2. Material price variance (SP - AP) x AQ (10 - 11) x 19 000 = 19 000 Adverse (Material A) (E15 14) x 10 100 = 10 100 Favourable (Material B) Possible causes of Price variance? Change in market conditions / purchasing department is not efficient. Should AQ be quantity purchased or quantity used? (Recommended to assume that actual purchases are identical with actual usage) Direct material variances (cont.) 3. Material usage variance (SQ-AQ) x SP (9000 x 2 kg=18000-19 000) x 10 = 10 000 Adverse (Mat.A) (9000 x1kg=9000-10100)x15 =16 500 Adverse (Mat.B) to assess the importance of the excess usage depends on the price of the materials, the variance should be expressed in monetary terms. Possible causes? the careless handling of materials by production personnel, the purchase of inferior quality materials pilferage, changes in quality control requirements or changes in methods of production. Speedy reporting required Direct labour variances 1. Can also be analysed into price and quantity. 2. Wage rate variance the standard wage rate per hour (SR) and the actual wage rate (AR) multiplied by the actual number of hours worked (AH) (SR - AR) x AH (9 9.60) x 28 500 = 17 100 Adverse * Possible causes? 3. Labour efficiency variance the standard labour hours for actual production (SH) and the actual labour hours worked (AH) during the period multiplied by the standard wage rate per hour (SR) (SH - AH) x SR (9 000 x 3 hours = 27 000SHP - 28 500AH ) x 9 = 13 500 Adverse * Possible causes? Controllable: the use of inferior quality materials, different grades of labour, failure to maintain machinery in proper condition, the introduction of new equipment or tools, and changes in the production processes. Not controllable by production manager: to poor production scheduling by the planning department, or to a change in quality control standards. Overhead variances 1. Overhead efficiency variance (SH - AH) SR The difference between the standard hours (SH) and the actual hours (AH) for the period multiplied by the standard overhead rate (SR) Overhead variances (cont.) 2. Overhead activity variance (AH - BH) x SRf This variance determines the concept of underactivity or overactivity, deficit o savings in fixed costs. 3. Overhead budget variance (SRV-ARV) x AH + (BFO - AFO) Indicates whether actual overhead expenses are higher o lower than overhead projected costs link

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance