Answered step by step

Verified Expert Solution

Question

1 Approved Answer

could you please do all of these questions , thank you so much , i really appreciate it. thumb up for sure. :) (a) The

could you please do all of these questions , thank you so much , i really appreciate it. thumb up for sure. :)

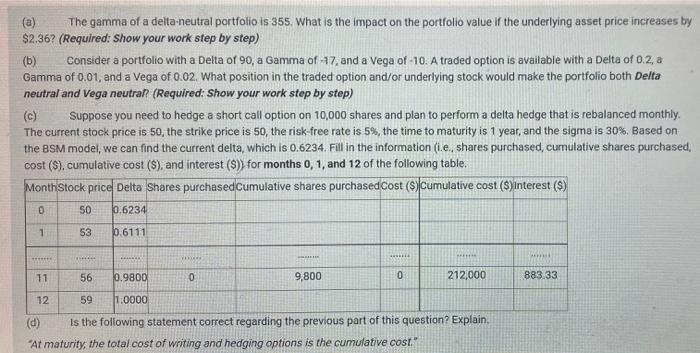

(a) The gamma of a delta-neutral portfolio is 355. What is the impact on the portfolio value if the underlying asset price increases by $2.36? (Required: Show your work step by step) (b) Consider a portfolio with a Delta of 90, a Gamma of -17, and a Vega of -10. A traded option is available with a Delta of 0.2, a Gamma of 0.01, and a Vega of 0.02. What position in the traded option and/or underlying stock would make the portfolio both Delta neutral and Vega neutral? (Required: Show your work step by step) (c) Suppose you need to hedge a short call option on 10,000 shares and plan to perform a delta hedge that is rebalanced monthly. The current stock price is 50, the strike price is 50, the risk-free rate is 5%, the time to maturity is 1 year, and the sigma is 30%. Based on the BSM model, we can find the current delta, which is 0.6234. Fill in the information (i.e., shares purchased, cumulative shares purchased, cost ($), cumulative cost ($), and interest ($)) for months 0, 1, and 12 of the following table. MonthStock price Delta Shares purchased Cumulative shares purchased Cost ($) Cumulative cost ($) interest ($) 0 50 0.6234 1 53 0.6111 www wi ****** 11 56 0.9800 0 9,800 0 212,000 883.33 12 59 1.0000 Is the following statement correct regarding the previous part of this question? Explain. (d) "At maturity, the total cost of writing and hedging options is the cumulative cost." (a) The gamma of a delta-neutral portfolio is 355. What is the impact on the portfolio value if the underlying asset price increases by $2.36? (Required: Show your work step by step) (b) Consider a portfolio with a Delta of 90, a Gamma of -17, and a Vega of -10. A traded option is available with a Delta of 0.2, a Gamma of 0.01, and a Vega of 0.02. What position in the traded option and/or underlying stock would make the portfolio both Delta neutral and Vega neutral? (Required: Show your work step by step) (c) Suppose you need to hedge a short call option on 10,000 shares and plan to perform a delta hedge that is rebalanced monthly. The current stock price is 50, the strike price is 50, the risk-free rate is 5%, the time to maturity is 1 year, and the sigma is 30%. Based on the BSM model, we can find the current delta, which is 0.6234. Fill in the information (i.e., shares purchased, cumulative shares purchased, cost ($), cumulative cost ($), and interest ($)) for months 0, 1, and 12 of the following table. MonthStock price Delta Shares purchased Cumulative shares purchased Cost ($) Cumulative cost ($) interest ($) 0 50 0.6234 1 53 0.6111 www wi ****** 11 56 0.9800 0 9,800 0 212,000 883.33 12 59 1.0000 Is the following statement correct regarding the previous part of this question? Explain. (d) "At maturity, the total cost of writing and hedging options is the cumulative cost Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance And Investments

Authors: Keith Redhead

1st Edition

0415428629, 978-0415428620