Answered step by step

Verified Expert Solution

Question

1 Approved Answer

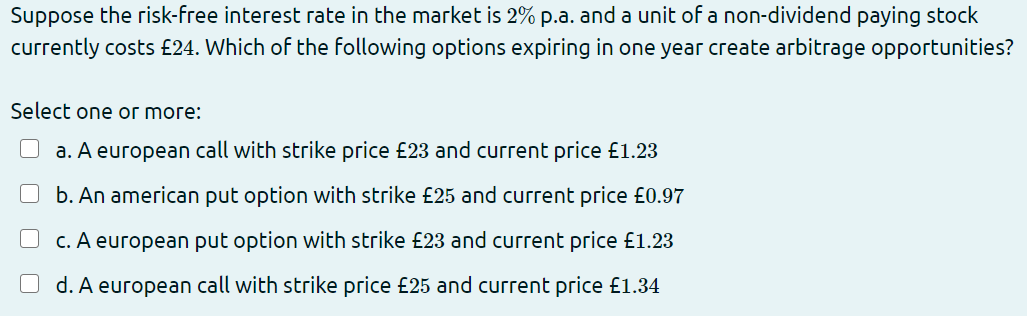

Could you please solve this question? Thank you. Suppose the risk-free interest rate in the market is 2% p.a. and a unit of a non-dividend

Could you please solve this question? Thank you.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Reporting Standards A Practical Guide

Authors: Hennie Van Greuning, Darrel Scott, Simonet Terblanche

6th Edition

0821384287, 978-0821384282