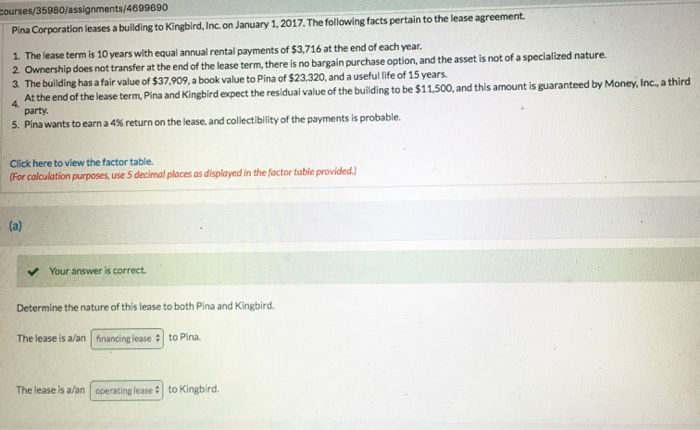

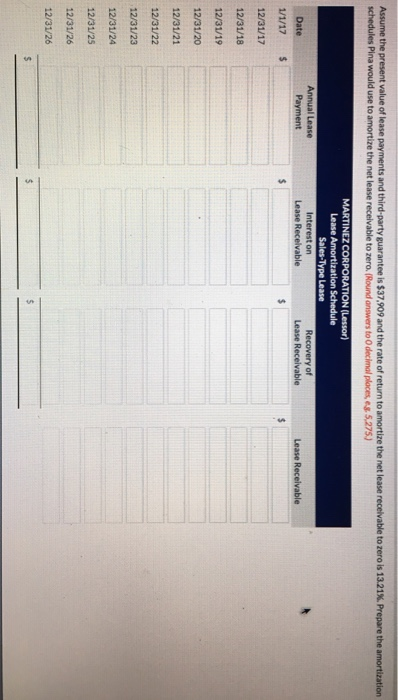

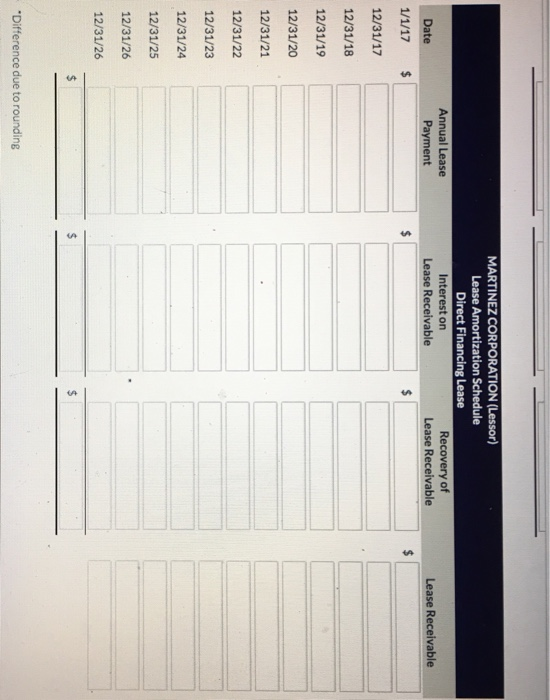

courses/35980/assignments/4699696 Pina Corporation leases a building to Kingbird, Inc on January 1, 2017. The following facts pertain to the lease agreement. 1. The lease term is 10 years with equal annual rental payments of $3,716 at the end of each year. 2 Ownership does not transfer at the end of the lease term, there is no bargain purchase option, and the asset is not of a specialized nature 3. The building has a fair value of $37,909, a book value to Pina of $23,320, and a useful life of 15 years. At the end of the lease term, Pina and Kingbird expect the residual value of the building to be $11.500, and this amount is guaranteed by Money, Inc., a third party 5. Pina wants to earn a 4% return on the lease, and collectibility of the payments is probable. Click here to view the factor table. (For calculation purposes, use 5 decimal places as displayed in the factor table provided.) (a) Your answer is correct. Determine the nature of this lease to both Pina and Kingbird. The lease is a/an financing lease: to Pina. The lease is a/an operating lease to Kingbird. Assume the present value of lease payments and third-party guarantee is $37,909 and the rate of return to amortize the net lease receivable to zero is 13.21%. Prepare the amortization schedules Pina would use to amortize the net lease receivable to zero. (Round answers to decimal places, s. 5.275) MARTINEZ CORPORATION (Lessor) Lease Amortization Schedule Sales-Type Lease Interest on Recovery of Lease Receivable Lease Receivable Annual Lease Payment Lease Receivable Date 1/1/17 12/31/17 12/31/18 12/31/19 12/31/20 12/31/21 12/31/22 12/31/23 12/31/24 12/31/25 12/31/26 12/31/26 MARTINEZ CORPORATION (Lessor) Lease Amortization Schedule Direct Financing Lease Interest on Recovery of Lease Receivable Lease Receivable Annual Lease Payment Date 1/1/17 Lease Receivable 12/31/17 12/31/18 12/31/19 12/31/20 12/31/21 12/31/22 12/31/23 12/31/24 12/31/25 12/31/26 12/31/26 "Difference due to rounding courses/35980/assignments/4699696 Pina Corporation leases a building to Kingbird, Inc on January 1, 2017. The following facts pertain to the lease agreement. 1. The lease term is 10 years with equal annual rental payments of $3,716 at the end of each year. 2 Ownership does not transfer at the end of the lease term, there is no bargain purchase option, and the asset is not of a specialized nature 3. The building has a fair value of $37,909, a book value to Pina of $23,320, and a useful life of 15 years. At the end of the lease term, Pina and Kingbird expect the residual value of the building to be $11.500, and this amount is guaranteed by Money, Inc., a third party 5. Pina wants to earn a 4% return on the lease, and collectibility of the payments is probable. Click here to view the factor table. (For calculation purposes, use 5 decimal places as displayed in the factor table provided.) (a) Your answer is correct. Determine the nature of this lease to both Pina and Kingbird. The lease is a/an financing lease: to Pina. The lease is a/an operating lease to Kingbird. Assume the present value of lease payments and third-party guarantee is $37,909 and the rate of return to amortize the net lease receivable to zero is 13.21%. Prepare the amortization schedules Pina would use to amortize the net lease receivable to zero. (Round answers to decimal places, s. 5.275) MARTINEZ CORPORATION (Lessor) Lease Amortization Schedule Sales-Type Lease Interest on Recovery of Lease Receivable Lease Receivable Annual Lease Payment Lease Receivable Date 1/1/17 12/31/17 12/31/18 12/31/19 12/31/20 12/31/21 12/31/22 12/31/23 12/31/24 12/31/25 12/31/26 12/31/26 MARTINEZ CORPORATION (Lessor) Lease Amortization Schedule Direct Financing Lease Interest on Recovery of Lease Receivable Lease Receivable Annual Lease Payment Date 1/1/17 Lease Receivable 12/31/17 12/31/18 12/31/19 12/31/20 12/31/21 12/31/22 12/31/23 12/31/24 12/31/25 12/31/26 12/31/26 "Difference due to rounding