Answered step by step

Verified Expert Solution

Question

1 Approved Answer

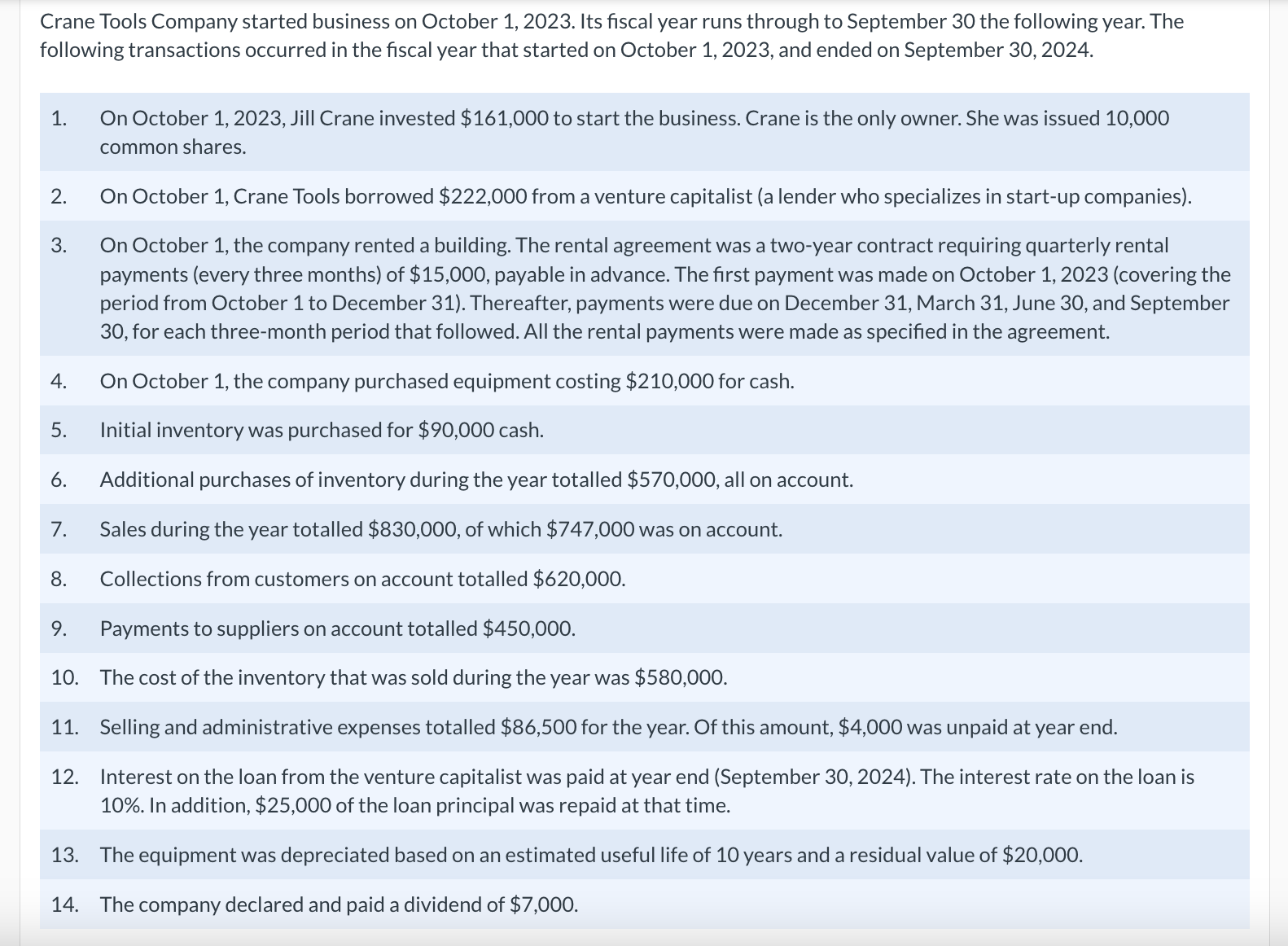

Crane Tools Company started business on October 1, 2023. Its fiscal year runs through to September 30 the following year. The following transactions occurred in

Crane Tools Company started business on October 1, 2023. Its fiscal year runs through to September 30 the following year. The following transactions occurred in the fiscal year that started on October 1, 2023, and ended on September 30, 2024. 1. On October 1,2023 , Jill Crane invested $161,000 to start the business. Crane is the only owner. She was issued 10,000 common shares. 2. On October 1 , Crane Tools borrowed $222,000 from a venture capitalist (a lender who specializes in start-up companies). 3. On October 1, the company rented a building. The rental agreement was a two-year contract requiring quarterly rental payments (every three months) of $15,000, payable in advance. The first payment was made on October 1, 2023 (covering the period from October 1 to December 31). Thereafter, payments were due on December 31, March 31, June 30, and September 30 , for each three-month period that followed. All the rental payments were made as specified in the agreement. 4. On October 1 , the company purchased equipment costing $210,000 for cash. 5. Initial inventory was purchased for $90,000 cash. 6. Additional purchases of inventory during the year totalled $570,000, all on account. 7. Sales during the year totalled $830,000, of which $747,000 was on account. 8. Collections from customers on account totalled $620,000. 9. Payments to suppliers on account totalled $450,000. 10. The cost of the inventory that was sold during the year was $580,000. 11. Selling and administrative expenses totalled $86,500 for the year. Of this amount, $4,000 was unpaid at year end. 12. Interest on the loan from the venture capitalist was paid at year end (September 30,2024). The interest rate on the loan is 10%. In addition, $25,000 of the loan principal was repaid at that time. 13. The equipment was depreciated based on an estimated useful life of 10 years and a residual value of $20,000. 14. The company declared and paid a dividend of $7,000. Prepare journal entries for each of the transactions and adjustments listed in the problem. (List all debit entries before credit entries. Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.)

Crane Tools Company started business on October 1, 2023. Its fiscal year runs through to September 30 the following year. The following transactions occurred in the fiscal year that started on October 1, 2023, and ended on September 30, 2024. 1. On October 1,2023 , Jill Crane invested $161,000 to start the business. Crane is the only owner. She was issued 10,000 common shares. 2. On October 1 , Crane Tools borrowed $222,000 from a venture capitalist (a lender who specializes in start-up companies). 3. On October 1, the company rented a building. The rental agreement was a two-year contract requiring quarterly rental payments (every three months) of $15,000, payable in advance. The first payment was made on October 1, 2023 (covering the period from October 1 to December 31). Thereafter, payments were due on December 31, March 31, June 30, and September 30 , for each three-month period that followed. All the rental payments were made as specified in the agreement. 4. On October 1 , the company purchased equipment costing $210,000 for cash. 5. Initial inventory was purchased for $90,000 cash. 6. Additional purchases of inventory during the year totalled $570,000, all on account. 7. Sales during the year totalled $830,000, of which $747,000 was on account. 8. Collections from customers on account totalled $620,000. 9. Payments to suppliers on account totalled $450,000. 10. The cost of the inventory that was sold during the year was $580,000. 11. Selling and administrative expenses totalled $86,500 for the year. Of this amount, $4,000 was unpaid at year end. 12. Interest on the loan from the venture capitalist was paid at year end (September 30,2024). The interest rate on the loan is 10%. In addition, $25,000 of the loan principal was repaid at that time. 13. The equipment was depreciated based on an estimated useful life of 10 years and a residual value of $20,000. 14. The company declared and paid a dividend of $7,000. Prepare journal entries for each of the transactions and adjustments listed in the problem. (List all debit entries before credit entries. Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Study Guide To Accompany Financial Accounting In An Economic Context

Authors: Jamie Pratt

6th Edition

0471731110, 978-0471731115