Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Create a Death Bond Diagram PROFITING FROM MORTALITY By: Goldstein, Matthew, Business Week, 7/30/2007, Issue 40-44 Death bends may be the most macabre investment scheme

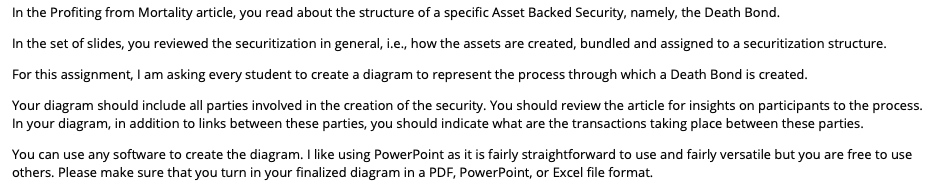

Create a Death Bond Diagram

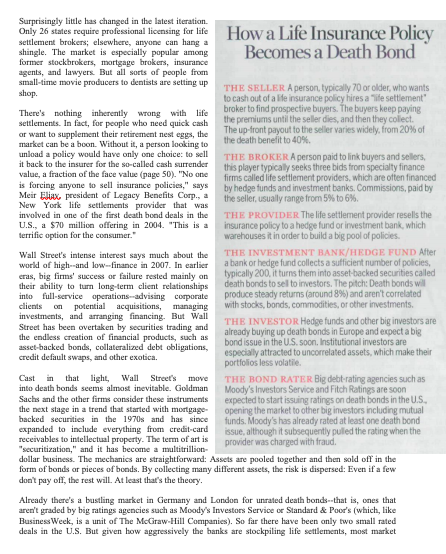

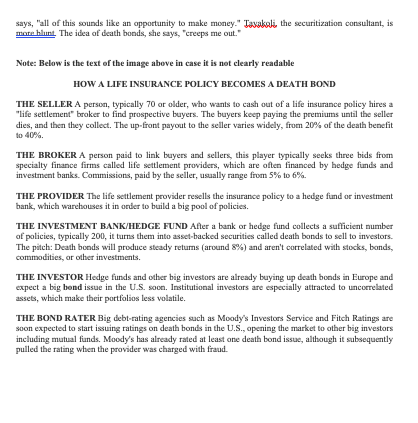

PROFITING FROM MORTALITY By: Goldstein, Matthew, Business Week, 7/30/2007, Issue 40-44 Death bends may be the most macabre investment scheme ever devised by Wall Street In May, as the subprime mortgage market was cracking, many of the biggest players in finance gathered at a conference in New York to talk about the next exotic investment coming down the pike: death bonds. When the event was held two years ago, just 250 people showed up. This time, nearly 600 descended on the Sheraton Hotel & Towers for the three-day confab, including delegations from Bear Stearns, Deutsche Bank, Lehman Brothers, Merrill Lynch, UBS, Wachovia, Wells Fargo, and other big firms. They flocked to seminars with titles such as "Legislative Review," milled about the exhibition hall picking up the usual conference swag, and buzzed at luncheons and a Carnegie Hall gala about the big push into the market being made by Cantor Fitzgerald, a major hond-trading shop. With all the happy banter, you wouldn't have known they were there to learn about new and imaginative ways to profit from people dying Death bond is shorthand for a gentler term the industry prefers: life settlement-backed security. Whatever the name, it's as macabre an investing concept as Wall Street has ever cooked up. Some 90 million Americans own life insurance, but many of them find the premiums too expensive; others would simply prefer to cash in early. "Life settlements" are arrangements that offer people the chance to sell their policies to investors, who keep paying the premiums until the sellers die and then collect the payout. For the investors it's a ghoulish actuarial gamble: The quicker the death, the more profit is reaped. Most of the transactions are done by small local firms called life settlement providers, which in the past have typically sold the policies to hedge funds. Now, Wall Street sees huge profits in buying policies, throwing them into a pool, dividing the pool into bonds, and selling the bonds to pension funds, college endowments, and other professional investors. If the market develops as Wall Street expects, ordinary mutual funds will soon be able to get in on the action, too. But the investment banks are wading into murky waters. The life settlements industry increasingly finds itself in the grip of dubious characters devising audacious and in some cases illegal schemes to make money. Many are targeting elderly people with deceptive sales pitches--so many that the National Association of Securities Dealers has issued a warning about abusive practices. Others are promising investors unrealistic returns or misleading them about the risks. Some are doing both. That didn't discourage the high-powered guests at the New York conference, though. As they tossed back cocktails and dined on pan-seared filet mignon, they enthused about the market's possibilities. "Wall Street firms are here because they know this is an asset class that isn't going away," says David C. Doer, president and CEO of Life-Exchange Inc., an electronic platform for trading life settlements. "There's big potential." The truth is, at this early stage, there's no way of knowing how popular death bonds might become. Wall Street's innovation machine has turned out both huge hits and big flops over the years. But the growth the underlying market for life settlements has been torrid so far. In 2005 about $10 billion worth were transacted, according to Sanford C. Bernstein & Co., up from virtually nothing in 2001. Industry analysts say this number rose to $15 billion in 2006, and could double this year, to $30 billion. Over the next few decades, as the ranks of retirees swell, Bernstein predicts that the face value of life settlement deals will top $160 billion a year in today's dollars. Death bonds will never approach the size of the mortgage market, which saw $1.9 trillion of securities issued last year. But if Wall Street achieves its goal of turning most of the life settlements created each year into death bonds, the market could rival the size of today's junk-bond market, where issuance totaled $128 billion in 2006, up from $56 billion in 1996, according to market Watcher Dualogic Investment banks have already drawn up their sales pitches to well-heeled institutional customers. Firms say death bonds should return around 8% a year, right between the expected returns of stocks and Treasury bonds. Moreover, they're "uncorrelated assets," meaning their performance isn't tied to what's happening in other markets. After all, death rates don't rise or fall based on what's happening to commodities, say. Lincorrelated assets like these are highly prized in an increasingly connected global financial system. It all sounds great, except that many of the life settlements that Wall Street firms are buying fall into categories ranging from sketchy to toxic. "They are creating a very risky product," says Janet Taxakali, a Chicago financial consultant who specializes in advising clients an asset-backed investments. They may be planning to sell them to sophisticated investors, but they could be coping in people who don't appreciate the risk." Many life settlement providers, for example, are trying to lure people who don't even hold insurance. In this tail-wagging-the-dog scenario, speculators take out policies on the individuals' behalf, pay them something up front, cover the premiums, and then wait for the people to die so they can collect. At the most outlandish extreme, one outfit devised a plan involving the population of the Federation of St. Kitts and Nevis in the Caribbean. Investors, meanwhile, have been burned by operators who have misrepresented the profit potential on deals. Two men now awaiting trial in California hatched an allegedly fraudulent scheme aimed at the entire congregation of a black church in South Central Los Angeles. They promised investors 25% annual retums because African Americans die carlier than other racial groups-an ugly pitch that prosecutors say averstated the upside potential. Even some of the biggest life settlement firms operate under a cloud. Philadelphia's Coventry First, for example, faces civil charges from the New York Attorney General's office and is in danger of being barred from doing business in Florida. It denies any wrongdoing. The eight-year-old industry certainly has an ignominious history. It grew from the shards of the so-called siatical business, which imploded in the late 1990s amid allegations of fraudulent dealings with AIDS patients and other terminally ill people. The word viatical comes from viaticum, a religious term for the communion given to a person near death. As AIDS spread during the 1980s, patients turned to the viatical settlements market to unlock insurance money to pay for care. But advances in medicine in the 1990s extended patients' lives, making siaticals less profitable for the buyers. At the same time, the industry was rife with abusive sales practices that drew the attention of prosecutors. By 1999, business had all but dried up How a Life Insurance Policy Becomes a Death Bond Surprisingly little has changed in the latest iteration Only 26 states require professional licensing for life settlement brokers; elsewhere, anyone can hang a shingle. The market is especially popular among former stockbrokers, mortgage brokers, insurance agents, and lawyers. But all sorts of people from small-time movie producers to dentists are setting up shop. THE SELLER A person, typically 70 or older, who wants to cash out of a life insurance policy hires a "life settlement" There's nothing inherently wrong with life broker to find prospective buyers. The buyers keep paying settlements. In fact, for people who need quick cash the premiums until the seller dies, and then they colect. or want to supplement their retirement est eggs, the The up-front payout to the seller varies widely, from 20% of market can be a boon. Without it, a person looking to the death benefit to 40% unload a policy would have only one choice to sell THE BROKERA person paid to link buyers and sellers, it back to the insurer for the so-called cash surrender this player typically seeks three bids from specialty finance value, a fraction of the face value (page 50). "No one firms called life settlement providers, which are often financed is forcing anyone to sell insurance policies," says by hedge funds and investment banks. Commissions, paid by Meir Elix president of Legacy Benefits Corp., a New York life settlements provider that was the seller, usually range from 5% to 6%. involved in one of the first death bond deals in the THE PROVIDER The life settlement provider resells the U.S., a $70 million offering in 2004. "This is a insurance policy to a hedge fund or investment bank, which terrific option for the consumer." warehouses it in order to build a big pool of policies. Wall Street's intense interest says much about the THE INVESTMENT BANK/HEDGE FUND After world of high- and low-finance in 2007. In earlier a bank or hedge fund collects a sufficient number of policies, eras, big firms' success or failure rested mainly on typically 200, it turns them into asset-backed securities called their ability to turn long-term client relationships death bonds to sel to investors. The pitch: Death bonds wil into full-service operations--advising corporate produce steady returns (around 8%) and aren't correlated clients on potential acquisitions, managing with stocks, bonds, commodities, or other investments investments, and arranging financing. But Wall THE INVESTOR Hedge funds and other big investors are Street has been overtaken by securities trading and already buying up death bonds in Europe and expect a big the endless creation of financial products, such as asset-backed bonds, collateralized debt obligations, bond issue in the U.S. soon, Institutional investors are especially attracted to uncorrelated assets, which make their credit default swaps, and other exotica. portfolios less volatile Cast that light, Wall Street's move THE BOND RATER Big debt-rating agencies such as into death bonds seems almost inevitable. Goldman Moody's Investors Service and Fitch Ratings are soon Sachs and the other firms consider these instruments expected to start issuing ratings on death bonds in the U.S. the next stage in a trend that started with mortgage opening the market to other big investors including mutual hacked securities in the 1970s and has since funds. Moody's has already rated at least one death bond expanded to include everything from credit card issue, although it subsequently pulled the rating when the receivables to intellectual property. The term of art is provider was charged with fraud. "securitization, and it has become a multitrillion dollar business. The mechanics are straightforward: Assets are pooled together and then sold off in the form of bonds or pieces of bonds. By collecting many different assets, the risk is dispersed: Even if a few don't pay off, the rest will. At least that's the theory. Already there's a bustling market in Germany and London for unrated death bonds -- that is, ones that aren't graded by big ratings agencies such as Moody's Investors Service or Standard & Poor's (which, like Business Week, is a unit of The McGraw-Hill Companies). So far there have been only two small rated deals in the U.S. But given how aggressively the banks are stockpiling life settlements, most market watchers expect big, rated deals to become commonplace soon, at which point mutual funds can dive in. "The product just lends itself to securitizations, like what has been done with mortgage-backed securities," says Philippe Halstadt, who heads the new "longevity derivatives" group at Bear Stearns & Co. Cantor Fitzgerald, one of Wall Street's saviest bond-trading shops, is rolling out an electronic trading platform for life settlements and, ultimately, death bands. The best platform has been in the works for more than a year and is a major priority inside Cantar, say insiders. But the push into increasingly complicated securitizations carries with it ever greater risk. That's what Wall Street is dealing with now as bonds backed by pools of subprime mortgages blow up left and right. A surge in defaults on these riskiest of loans is battering the hedge funds that invested--and the banks that arranged packaged, and sold them. In June, two Bear Stearns hedge funds that bet on bonds backed by subprime loans collapsed, sparking panic on Wall Street about the health of other risky investments Tavukali says the same kinds of missteps are bound to happen with death bonds. But Wall Street is good at justifying its moves into new lines of business, however iffy they might seem, notes Kenneth C. Ecoexiss, a professor of finance at New York University's Stem School of Business and a former JPMorgan Chase & Co. investment banker: "At the end of the day, what Wall Street does best is figuring out what investors might want and structuring products to meet those needs." And its own needs. That's not to say it isn't aware of appearances. Wall Street is doing its best both to polish the life settlement industry's image and to downplay its own direct involvement. The New York conference was put on by the Life Insurance Settlement Assn. (LISA), an organization of market players that began as the Viatical Association of America in 1994, changed its name to the Viatical & Life Settlement Assn. in 2000, and then dropped the "viatical" altogether three years ago. In an attempt to put even more distance between Wall Street and the old viatical crowd, six investment houses, including Bear Stearns, Credit Suisse, Goldman Sachs, and UBS, in March formed a trade group called the Institutional Life Markets Assn. to lobby for "best practices" and "appropriate regulation." Until some degree of legitimacy is in place, firms will keep as low a profile as possible. Goldman Sachs, for example, came close last year to acquiring San Diego's Life Settlement Solutions Inc., a large provider, but backed out at the last minute, according to people familiar with the potential deal. Instead, Goldman, which declined to comment for this story, is quietly building up its own subsidiary under the nondescript name Eastport Capital. That unit sent four representatives to the LISA conference It's no wonder that Wall Street is simultaneously attracted and cautious. The alchemy going on in the finance labs is real, but the market for life settlements is deeply troubled. There's a persistent problem with brokers offering lowball prices and failing to disclose transaction costs. The marketing to investors has often been suspect, too. In late 2005, for instance, the big accounting firm KPMG sent a cease-and- desist notice to Kaxbeta. Investment Services Ltd., a London firm that was using KPMG's name in its marketing material for unrated death bonds without permission. A Baadata oflicial didn't retum phone calls seeking comment. A KPMG spokesman says: "We do not endorse or recommend these products." Improper marketing is just one of the things that got two California men into trouble. Next March, Curtis D. Somoza and Robert A. Caberla are scheduled to go on trial in federal court in Los Angeles on charges that they bilked dozens of investors out of tens of millions of dollars in a scheme involving an African American church group in Los Angeles called the Personal Involvement Center. The men, whose lawyers declined to comment, raised $69 million for an investment trust called Persistence Capital, which arranged to buy policies from Transamerica Corp. on the lives of some 2,000 members of the inner-city church. The deal was structured so that Persistence would pay for the premiums, while the $275,000 death benefit on cach policy would be split three ways: $15,000 to the deceased person's family to cover burial costs, $20,000 to the church group, and the remaining $240,000 to the trust. The trust's haul would go toward paying the premiums on the remaining policies and providing payouts to investors. says, "all of this sounds like an opportunity to make money." Taxakali, the securitization consultant, is mote blunt. The idea of death bonds, she says, 'creeps me out." Note: Below is the text of the image above in case it is not clearly readable HOW A LIFE INSURANCE POLICY BECOMES A DEATH BOND THE SELLER A person, typically 70 or older, who wants to cash out of a life insurance policy hires a "life settlement broker to find prospective buyers. The buyers keep paying the premiums until the seller dies, and then they collect. The up-front payout to the seller varies widely, from 20% of the death benefit to 40% THE BROKER A person paid to link buyers and sellers, this player typically seeks three bids from specialty finance firms called life settlement providers, which are often financed by hedge funds and investment banks. Commissions, paid by the seller, usually range from 5% to 6%. THE PROVIDER The life settlement provider resells the insurance policy to a hedge fund or investment bank, which warehouses it in order to build a big pool of policies. THE INVESTMENT BANK/HEDGE FUND After a bank or hedge fund collects a sufficient number of policies, typically 200, it turns them into asset-backed securities called death bonds to sell to investors. The pitch: Death bonds will produce steady returns (around 8%) and aren't correlated with stocks, bands, commodities, or other investments THE INVESTOR Hedge funds and other big investors are already buying up death bonds in Europe and expect a big bond issue in the U.S. soon. Institutional investors are especially attracted to uncorrelated assets, which make their portfolios less volatile, THE BOND RATER Big debt-rating agencies such as Moody's Investors Service and Fitch Ratings are soon expected to start issuing ratings on death bonds in the U.S., opening the market to other big investors including mutual funds. Moody's has already rated at least one death bond issue, although it subsequently pulled the rating when the provider was charged with fraud. In the Profiting from Mortality article, you read about the structure of a specific Asset Backed Security, namely, the Death Bond. In the set of slides, you reviewed the securitization in general, i.e., how the assets are created, bundled and assigned to a securitization structure. For this assignment, I am asking every student to create a diagram to represent the process through which a Death Bond is created. Your diagram should include all parties involved in the creation of the security. You should review the article for insights on participants to the process. In your diagram, in addition to links between these parties, you should indicate what are the transactions taking place between these parties. You can use any software to create the diagram. I like using PowerPoint as it is fairly straightforward to use and fairly versatile but you are free to use others. Please make sure that you turn in your finalized diagram in a PDF, PowerPoint, or Excel file format. PROFITING FROM MORTALITY By: Goldstein, Matthew, Business Week, 7/30/2007, Issue 40-44 Death bends may be the most macabre investment scheme ever devised by Wall Street In May, as the subprime mortgage market was cracking, many of the biggest players in finance gathered at a conference in New York to talk about the next exotic investment coming down the pike: death bonds. When the event was held two years ago, just 250 people showed up. This time, nearly 600 descended on the Sheraton Hotel & Towers for the three-day confab, including delegations from Bear Stearns, Deutsche Bank, Lehman Brothers, Merrill Lynch, UBS, Wachovia, Wells Fargo, and other big firms. They flocked to seminars with titles such as "Legislative Review," milled about the exhibition hall picking up the usual conference swag, and buzzed at luncheons and a Carnegie Hall gala about the big push into the market being made by Cantor Fitzgerald, a major hond-trading shop. With all the happy banter, you wouldn't have known they were there to learn about new and imaginative ways to profit from people dying Death bond is shorthand for a gentler term the industry prefers: life settlement-backed security. Whatever the name, it's as macabre an investing concept as Wall Street has ever cooked up. Some 90 million Americans own life insurance, but many of them find the premiums too expensive; others would simply prefer to cash in early. "Life settlements" are arrangements that offer people the chance to sell their policies to investors, who keep paying the premiums until the sellers die and then collect the payout. For the investors it's a ghoulish actuarial gamble: The quicker the death, the more profit is reaped. Most of the transactions are done by small local firms called life settlement providers, which in the past have typically sold the policies to hedge funds. Now, Wall Street sees huge profits in buying policies, throwing them into a pool, dividing the pool into bonds, and selling the bonds to pension funds, college endowments, and other professional investors. If the market develops as Wall Street expects, ordinary mutual funds will soon be able to get in on the action, too. But the investment banks are wading into murky waters. The life settlements industry increasingly finds itself in the grip of dubious characters devising audacious and in some cases illegal schemes to make money. Many are targeting elderly people with deceptive sales pitches--so many that the National Association of Securities Dealers has issued a warning about abusive practices. Others are promising investors unrealistic returns or misleading them about the risks. Some are doing both. That didn't discourage the high-powered guests at the New York conference, though. As they tossed back cocktails and dined on pan-seared filet mignon, they enthused about the market's possibilities. "Wall Street firms are here because they know this is an asset class that isn't going away," says David C. Doer, president and CEO of Life-Exchange Inc., an electronic platform for trading life settlements. "There's big potential." The truth is, at this early stage, there's no way of knowing how popular death bonds might become. Wall Street's innovation machine has turned out both huge hits and big flops over the years. But the growth the underlying market for life settlements has been torrid so far. In 2005 about $10 billion worth were transacted, according to Sanford C. Bernstein & Co., up from virtually nothing in 2001. Industry analysts say this number rose to $15 billion in 2006, and could double this year, to $30 billion. Over the next few decades, as the ranks of retirees swell, Bernstein predicts that the face value of life settlement deals will top $160 billion a year in today's dollars. Death bonds will never approach the size of the mortgage market, which saw $1.9 trillion of securities issued last year. But if Wall Street achieves its goal of turning most of the life settlements created each year into death bonds, the market could rival the size of today's junk-bond market, where issuance totaled $128 billion in 2006, up from $56 billion in 1996, according to market Watcher Dualogic Investment banks have already drawn up their sales pitches to well-heeled institutional customers. Firms say death bonds should return around 8% a year, right between the expected returns of stocks and Treasury bonds. Moreover, they're "uncorrelated assets," meaning their performance isn't tied to what's happening in other markets. After all, death rates don't rise or fall based on what's happening to commodities, say. Lincorrelated assets like these are highly prized in an increasingly connected global financial system. It all sounds great, except that many of the life settlements that Wall Street firms are buying fall into categories ranging from sketchy to toxic. "They are creating a very risky product," says Janet Taxakali, a Chicago financial consultant who specializes in advising clients an asset-backed investments. They may be planning to sell them to sophisticated investors, but they could be coping in people who don't appreciate the risk." Many life settlement providers, for example, are trying to lure people who don't even hold insurance. In this tail-wagging-the-dog scenario, speculators take out policies on the individuals' behalf, pay them something up front, cover the premiums, and then wait for the people to die so they can collect. At the most outlandish extreme, one outfit devised a plan involving the population of the Federation of St. Kitts and Nevis in the Caribbean. Investors, meanwhile, have been burned by operators who have misrepresented the profit potential on deals. Two men now awaiting trial in California hatched an allegedly fraudulent scheme aimed at the entire congregation of a black church in South Central Los Angeles. They promised investors 25% annual retums because African Americans die carlier than other racial groups-an ugly pitch that prosecutors say averstated the upside potential. Even some of the biggest life settlement firms operate under a cloud. Philadelphia's Coventry First, for example, faces civil charges from the New York Attorney General's office and is in danger of being barred from doing business in Florida. It denies any wrongdoing. The eight-year-old industry certainly has an ignominious history. It grew from the shards of the so-called siatical business, which imploded in the late 1990s amid allegations of fraudulent dealings with AIDS patients and other terminally ill people. The word viatical comes from viaticum, a religious term for the communion given to a person near death. As AIDS spread during the 1980s, patients turned to the viatical settlements market to unlock insurance money to pay for care. But advances in medicine in the 1990s extended patients' lives, making siaticals less profitable for the buyers. At the same time, the industry was rife with abusive sales practices that drew the attention of prosecutors. By 1999, business had all but dried up How a Life Insurance Policy Becomes a Death Bond Surprisingly little has changed in the latest iteration Only 26 states require professional licensing for life settlement brokers; elsewhere, anyone can hang a shingle. The market is especially popular among former stockbrokers, mortgage brokers, insurance agents, and lawyers. But all sorts of people from small-time movie producers to dentists are setting up shop. THE SELLER A person, typically 70 or older, who wants to cash out of a life insurance policy hires a "life settlement" There's nothing inherently wrong with life broker to find prospective buyers. The buyers keep paying settlements. In fact, for people who need quick cash the premiums until the seller dies, and then they colect. or want to supplement their retirement est eggs, the The up-front payout to the seller varies widely, from 20% of market can be a boon. Without it, a person looking to the death benefit to 40% unload a policy would have only one choice to sell THE BROKERA person paid to link buyers and sellers, it back to the insurer for the so-called cash surrender this player typically seeks three bids from specialty finance value, a fraction of the face value (page 50). "No one firms called life settlement providers, which are often financed is forcing anyone to sell insurance policies," says by hedge funds and investment banks. Commissions, paid by Meir Elix president of Legacy Benefits Corp., a New York life settlements provider that was the seller, usually range from 5% to 6%. involved in one of the first death bond deals in the THE PROVIDER The life settlement provider resells the U.S., a $70 million offering in 2004. "This is a insurance policy to a hedge fund or investment bank, which terrific option for the consumer." warehouses it in order to build a big pool of policies. Wall Street's intense interest says much about the THE INVESTMENT BANK/HEDGE FUND After world of high- and low-finance in 2007. In earlier a bank or hedge fund collects a sufficient number of policies, eras, big firms' success or failure rested mainly on typically 200, it turns them into asset-backed securities called their ability to turn long-term client relationships death bonds to sel to investors. The pitch: Death bonds wil into full-service operations--advising corporate produce steady returns (around 8%) and aren't correlated clients on potential acquisitions, managing with stocks, bonds, commodities, or other investments investments, and arranging financing. But Wall THE INVESTOR Hedge funds and other big investors are Street has been overtaken by securities trading and already buying up death bonds in Europe and expect a big the endless creation of financial products, such as asset-backed bonds, collateralized debt obligations, bond issue in the U.S. soon, Institutional investors are especially attracted to uncorrelated assets, which make their credit default swaps, and other exotica. portfolios less volatile Cast that light, Wall Street's move THE BOND RATER Big debt-rating agencies such as into death bonds seems almost inevitable. Goldman Moody's Investors Service and Fitch Ratings are soon Sachs and the other firms consider these instruments expected to start issuing ratings on death bonds in the U.S. the next stage in a trend that started with mortgage opening the market to other big investors including mutual hacked securities in the 1970s and has since funds. Moody's has already rated at least one death bond expanded to include everything from credit card issue, although it subsequently pulled the rating when the receivables to intellectual property. The term of art is provider was charged with fraud. "securitization, and it has become a multitrillion dollar business. The mechanics are straightforward: Assets are pooled together and then sold off in the form of bonds or pieces of bonds. By collecting many different assets, the risk is dispersed: Even if a few don't pay off, the rest will. At least that's the theory. Already there's a bustling market in Germany and London for unrated death bonds -- that is, ones that aren't graded by big ratings agencies such as Moody's Investors Service or Standard & Poor's (which, like Business Week, is a unit of The McGraw-Hill Companies). So far there have been only two small rated deals in the U.S. But given how aggressively the banks are stockpiling life settlements, most market watchers expect big, rated deals to become commonplace soon, at which point mutual funds can dive in. "The product just lends itself to securitizations, like what has been done with mortgage-backed securities," says Philippe Halstadt, who heads the new "longevity derivatives" group at Bear Stearns & Co. Cantor Fitzgerald, one of Wall Street's saviest bond-trading shops, is rolling out an electronic trading platform for life settlements and, ultimately, death bands. The best platform has been in the works for more than a year and is a major priority inside Cantar, say insiders. But the push into increasingly complicated securitizations carries with it ever greater risk. That's what Wall Street is dealing with now as bonds backed by pools of subprime mortgages blow up left and right. A surge in defaults on these riskiest of loans is battering the hedge funds that invested--and the banks that arranged packaged, and sold them. In June, two Bear Stearns hedge funds that bet on bonds backed by subprime loans collapsed, sparking panic on Wall Street about the health of other risky investments Tavukali says the same kinds of missteps are bound to happen with death bonds. But Wall Street is good at justifying its moves into new lines of business, however iffy they might seem, notes Kenneth C. Ecoexiss, a professor of finance at New York University's Stem School of Business and a former JPMorgan Chase & Co. investment banker: "At the end of the day, what Wall Street does best is figuring out what investors might want and structuring products to meet those needs." And its own needs. That's not to say it isn't aware of appearances. Wall Street is doing its best both to polish the life settlement industry's image and to downplay its own direct involvement. The New York conference was put on by the Life Insurance Settlement Assn. (LISA), an organization of market players that began as the Viatical Association of America in 1994, changed its name to the Viatical & Life Settlement Assn. in 2000, and then dropped the "viatical" altogether three years ago. In an attempt to put even more distance between Wall Street and the old viatical crowd, six investment houses, including Bear Stearns, Credit Suisse, Goldman Sachs, and UBS, in March formed a trade group called the Institutional Life Markets Assn. to lobby for "best practices" and "appropriate regulation." Until some degree of legitimacy is in place, firms will keep as low a profile as possible. Goldman Sachs, for example, came close last year to acquiring San Diego's Life Settlement Solutions Inc., a large provider, but backed out at the last minute, according to people familiar with the potential deal. Instead, Goldman, which declined to comment for this story, is quietly building up its own subsidiary under the nondescript name Eastport Capital. That unit sent four representatives to the LISA conference It's no wonder that Wall Street is simultaneously attracted and cautious. The alchemy going on in the finance labs is real, but the market for life settlements is deeply troubled. There's a persistent problem with brokers offering lowball prices and failing to disclose transaction costs. The marketing to investors has often been suspect, too. In late 2005, for instance, the big accounting firm KPMG sent a cease-and- desist notice to Kaxbeta. Investment Services Ltd., a London firm that was using KPMG's name in its marketing material for unrated death bonds without permission. A Baadata oflicial didn't retum phone calls seeking comment. A KPMG spokesman says: "We do not endorse or recommend these products." Improper marketing is just one of the things that got two California men into trouble. Next March, Curtis D. Somoza and Robert A. Caberla are scheduled to go on trial in federal court in Los Angeles on charges that they bilked dozens of investors out of tens of millions of dollars in a scheme involving an African American church group in Los Angeles called the Personal Involvement Center. The men, whose lawyers declined to comment, raised $69 million for an investment trust called Persistence Capital, which arranged to buy policies from Transamerica Corp. on the lives of some 2,000 members of the inner-city church. The deal was structured so that Persistence would pay for the premiums, while the $275,000 death benefit on cach policy would be split three ways: $15,000 to the deceased person's family to cover burial costs, $20,000 to the church group, and the remaining $240,000 to the trust. The trust's haul would go toward paying the premiums on the remaining policies and providing payouts to investors. says, "all of this sounds like an opportunity to make money." Taxakali, the securitization consultant, is mote blunt. The idea of death bonds, she says, 'creeps me out." Note: Below is the text of the image above in case it is not clearly readable HOW A LIFE INSURANCE POLICY BECOMES A DEATH BOND THE SELLER A person, typically 70 or older, who wants to cash out of a life insurance policy hires a "life settlement broker to find prospective buyers. The buyers keep paying the premiums until the seller dies, and then they collect. The up-front payout to the seller varies widely, from 20% of the death benefit to 40% THE BROKER A person paid to link buyers and sellers, this player typically seeks three bids from specialty finance firms called life settlement providers, which are often financed by hedge funds and investment banks. Commissions, paid by the seller, usually range from 5% to 6%. THE PROVIDER The life settlement provider resells the insurance policy to a hedge fund or investment bank, which warehouses it in order to build a big pool of policies. THE INVESTMENT BANK/HEDGE FUND After a bank or hedge fund collects a sufficient number of policies, typically 200, it turns them into asset-backed securities called death bonds to sell to investors. The pitch: Death bonds will produce steady returns (around 8%) and aren't correlated with stocks, bands, commodities, or other investments THE INVESTOR Hedge funds and other big investors are already buying up death bonds in Europe and expect a big bond issue in the U.S. soon. Institutional investors are especially attracted to uncorrelated assets, which make their portfolios less volatile, THE BOND RATER Big debt-rating agencies such as Moody's Investors Service and Fitch Ratings are soon expected to start issuing ratings on death bonds in the U.S., opening the market to other big investors including mutual funds. Moody's has already rated at least one death bond issue, although it subsequently pulled the rating when the provider was charged with fraud. In the Profiting from Mortality article, you read about the structure of a specific Asset Backed Security, namely, the Death Bond. In the set of slides, you reviewed the securitization in general, i.e., how the assets are created, bundled and assigned to a securitization structure. For this assignment, I am asking every student to create a diagram to represent the process through which a Death Bond is created. Your diagram should include all parties involved in the creation of the security. You should review the article for insights on participants to the process. In your diagram, in addition to links between these parties, you should indicate what are the transactions taking place between these parties. You can use any software to create the diagram. I like using PowerPoint as it is fairly straightforward to use and fairly versatile but you are free to use others. Please make sure that you turn in your finalized diagram in a PDF, PowerPoint, or Excel file formatStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting For Construction Frameworks Productivity Cost And Performance

Authors: Rick Best, Jim Meikle

1st Edition

1138293970, 978-1138293977