Create a general ledger using the given transactions.

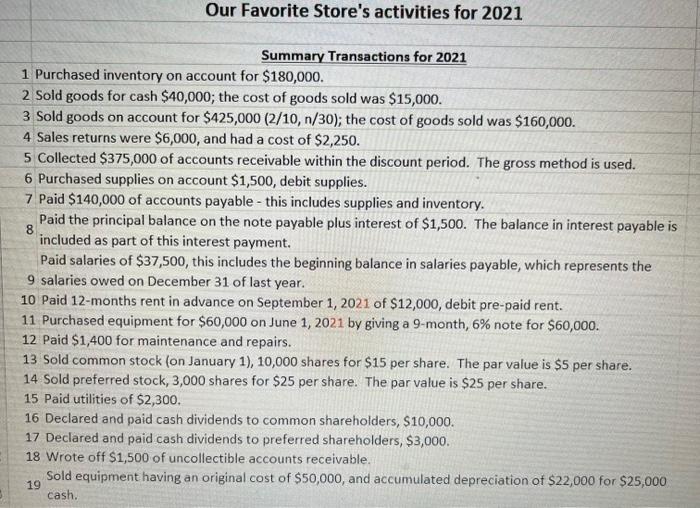

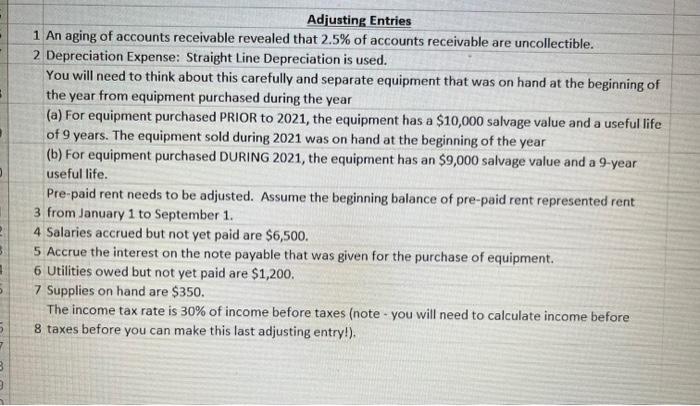

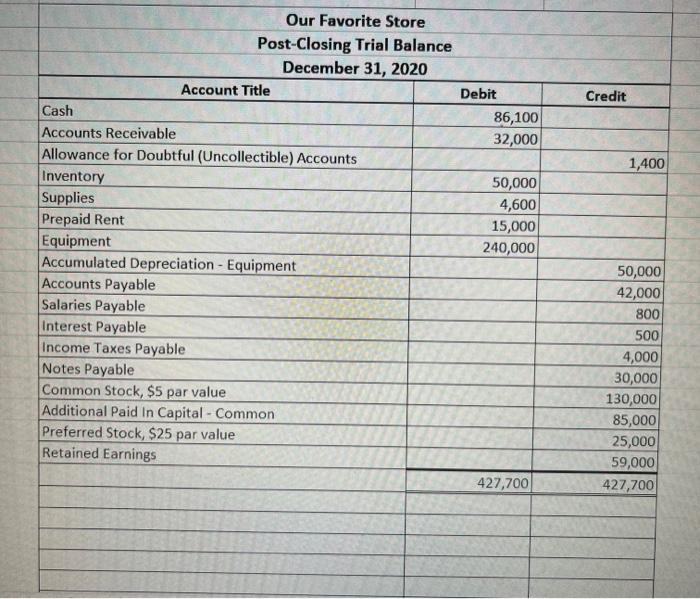

Our Favorite Store's activities for 2021 Summary Transactions for 2021 1 Purchased inventory on account for $180,000. 2 Sold goods for cash $40,000; the cost of goods sold was $15,000. 3 Sold goods on account for $425,000(2/10,n/30); the cost of goods sold was $160,000. 4 Sales returns were $6,000, and had a cost of $2,250. 5 Collected $375,000 of accounts receivable within the discount period. The gross method is used. 6 Purchased supplies on account $1,500, debit supplies. 7 Paid $140,000 of accounts payable - this includes supplies and inventory. 8 Paid the principal balance on the note payable plus interest of $1,500. The balance in interest payable is included as part of this interest payment. Paid salaries of $37,500, this includes the beginning balance in salaries payable, which represents the 9 salaries owed on December 31 of last year. 10 Paid 12-months rent in advance on September 1, 2021 of $12,000, debit pre-paid rent. 11 Purchased equipment for $60,000 on June 1,2021 by giving a 9-month, 6% note for $60,000. 12 Paid $1,400 for maintenance and repairs. 13 Sold common stock (on January 1), 10,000 shares for $15 per share. The par value is $5 per share. 14 Sold preferred stock, 3,000 shares for $25 per share. The par value is $25 per share. 15 Paid utilities of $2,300. 16 Declared and paid cash dividends to common shareholders, $10,000. 17 Declared and paid cash dividends to preferred shareholders, $3,000. 18 Wrote off $1,500 of uncollectible accounts receivable. 19 Sold equipment having an original cost of $50,000, and accumulated depreciation of $22,000 for $25,000 cash. Adjusting Entries 1 An aging of accounts receivable revealed that 2.5% of accounts receivable are uncollectible. 2 Depreciation Expense: Straight Line Depreciation is used. You will need to think about this carefully and separate equipment that was on hand at the beginning of the year from equipment purchased during the year (a) For equipment purchased PRIOR to 2021, the equipment has a $10,000 salvage value and a useful life of 9 years. The equipment sold during 2021 was on hand at the beginning of the year (b) For equipment purchased DURING 2021, the equipment has an $9,000 salvage value and a 9-year useful life. Pre-paid rent needs to be adjusted. Assume the beginning balance of pre-paid rent represented rent 3 from January 1 to September 1. 4 Salaries accrued but not yet paid are $6,500. 5 Accrue the interest on the note payable that was given for the purchase of equipment. 6 Utilities owed but not yet paid are $1,200. 7 Supplies on hand are $350. The income tax rate is 30% of income before taxes (note - you will need to calculate income before 8 taxes before you can make this last adjusting entry!). Our Favorite Store Post-Closing Trial Balance December 31, 2020 \begin{tabular}{|l|r|r|} \hline \multicolumn{1}{|c|}{ Account Title } & \multicolumn{1}{c|}{ Debit } & \multicolumn{1}{c|}{ Credit } \\ \hline Cash & 86,100 & \\ \hline Accounts Receivable & 32,000 & \\ \hline Allowance for Doubtful (Uncollectible) Accounts & & 1,400 \\ \hline Inventory & 50,000 & \\ \hline Supplies & 4,600 & \\ \hline Prepaid Rent & 15,000 & \\ \hline Equipment & 240,000 & \\ \hline Accumulated Depreciation - Equipment & & 50,000 \\ \hline Accounts Payable & & 42,000 \\ \hline Salaries Payable & & 800 \\ \hline Interest Payable & & 500 \\ \hline Income Taxes Payable & & 4,000 \\ \hline Notes Payable & & 30,000 \\ \hline Common Stock, \$5 par value & & 130,000 \\ \hline Additional Paid In Capital - Common & & 85,000 \\ \hline Preferred Stock, \$25 par value & & 25,000 \\ \hline Retained Earnings & & 59,000 \\ \hline & & 427,700 \\ \hline & & \\ \hline & & \\ \hline & & \\ \hline \end{tabular}