Question: create a SWOT table, each cell of which is limited to at most five important factors. create a SWOT table, each cell of which is

create a SWOT table, each cell of which is limited to at most five important factors.

create a SWOT table, each cell of which is limited to at most five important factors.

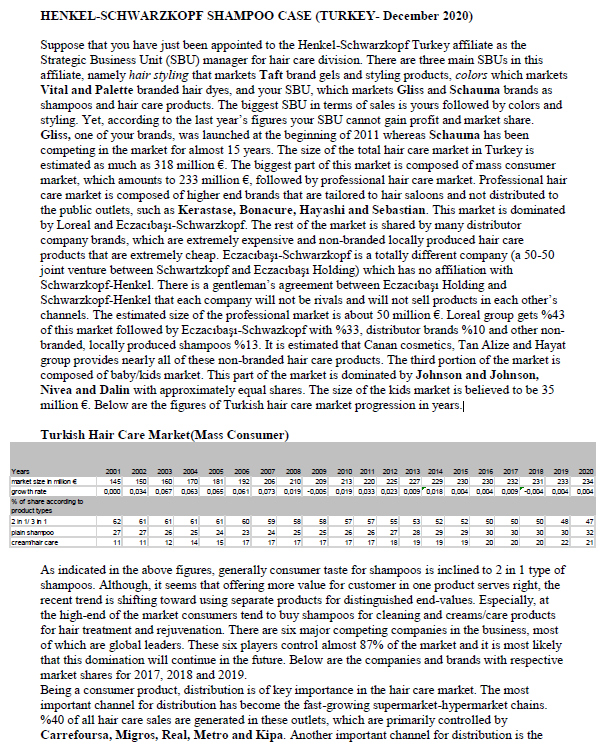

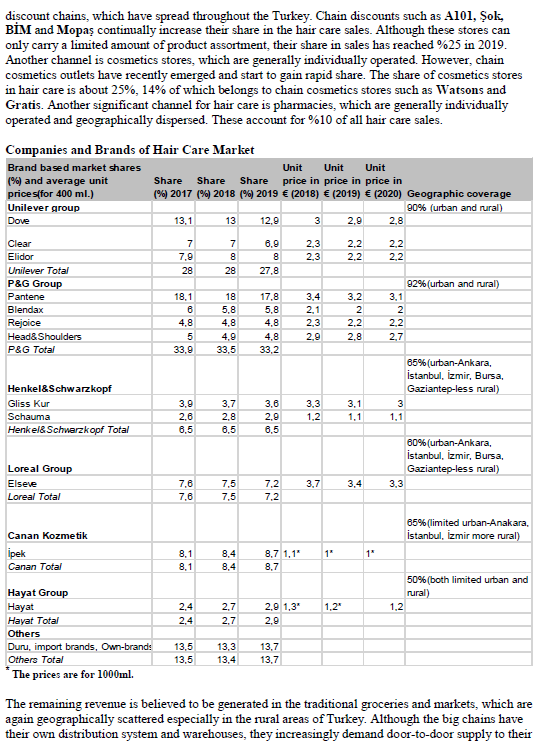

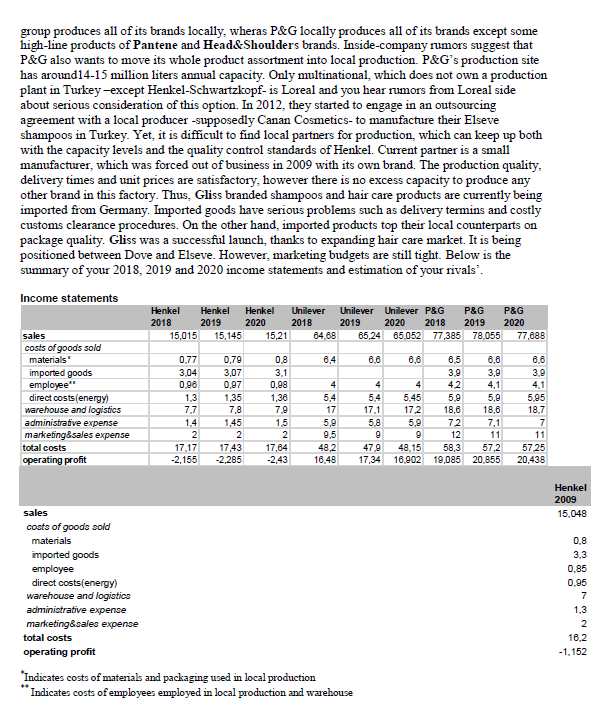

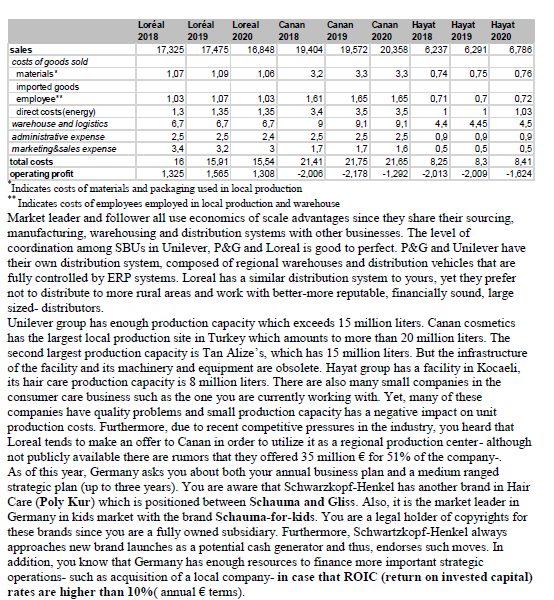

HENKEL-SCHWARZKOPF SHAMPOO CASE (TURKEY- December 2020) Suppose that you have just been appointed to the Henkel-Schwarzkopf Turkey affiliate as the Strategic Business Unit (SBU) manager for hair care division. There are three main SBUs in this affiliate, namely hair styling that markets Taft brand gels and styling products, colors which markets Vital and Palette branded hair dyes, and your SBU, which markets Gliss and Schauma brands as shampoos and hair care products. The biggest SBU in terms of sales is yours followed by colors and styling. Yet, according to the last year's figures your SBU cannot gain profit and market share. Gliss, one of your brands, was launched at the beginning of 2011 whereas Schauina has been competing in the market for almost 15 years. The size of the total hair care market in Turkey is estimated as much as 318 million . The biggest part of this market is composed of mass consumer market, which amounts to 233 million , followed by professional hair care market. Professional hair care market is composed of higher end brands that are tailored to hair saloons and not distributed to the public outlets, such as Kerastase, Bonacure, Hayashi and Sebastian. This market is dominated by Loreal and Eczacba-Schwarzkopf. The rest of the market is shared by many distributor company brands, which are extremely expensive and non-branded locally produced hair care products that are extremely cheap. Eczacba-Schwarzkopf is a totally different company (a 50-50 joint venture between Schwartzkopf and Eczacba Holding) which has no affiliation with Schwarzkopf-Henkel. There is a gentleman's agreement between Eczacba Holding and Schwarzkopf-Henkel that each company will not be rivals and will not sell products in each other's channels. The estimated size of the professional market is about 50 million . Loreal group gets %43 of this market followed by Eczacba-Schwazkopf with %33, distributor brands %10 and other non- branded, locally produced shampoos %13. It is estimated that Canan cosmetics, Tan Alize and Hayat group provides nearly all of these non-branded hair care products. The third portion of the market is composed of baby/kids market. This part of the market is dominated by Johnson and Johnson, Nivea and Dalin with approximately equal shares. The size of the kids market is believed to be 35 million . Below are the figures of Turkish hair care market progression in years./ Turkish Hair Care Market(Mass Consumer) 2001 2002 2003 2004 2005 2006 2007 145 150 160 170 181 192 205 0,000 0,034 0.067 0.053 0,065 0,061 0.073 2009 2009 2010 2011 2012 2013 2014 2015 2016 2017 2010 2019 2020 210 209 213 220 225 227 229 230 230 231 233 234 0,019 -0,005 0,019 0,033 0,023 0,009 0.018 0.004 0.004 0,009 -0,004 0,004 0.004 Years market szen min growth rate % of share according to product types 2 in 131 pisin shampoo creamhaircare 61 61 51 61 60 59 58 58 57 55 52 53 28 19 50 30 20 SO 30 20 29 19 50 30 20 48 30 47 32 11 12 14 15 17 17 17 17 17 18 19 As indicated in the above figures, generally consumer taste for shampoos is inclined to 2 in 1 type of shampoos. Although, it seems that offering more value for customer in one product serves right, the recent trend is shifting toward using separate products for distinguished end-values. Especially, at the high-end of the market consumers tend to buy shampoos for cleaning and creams/care products for hair treatment and rejuvenation. There are six major competing companies in the business, most of which are global leaders. These six players control almost 87% of the market and it is most likely that this domination will continue in the future. Below are the companies and brands with respective market shares for 2017, 2018 and 2019. Being a consumer product, distribution is of key importance in the hair care market. The most important channel for distribution has become the fast-growing supermarket-hypermarket chains. %40 of all hair care sales are generated in these outlets, which are primarily controlled by Carrefoursa, Migros, Real, Metro and Kipa. Another important channel for distribution is the discount chains, which have spread throughout the Turkey. Chain discounts such as A101, ok, BM and Mopas continually increase their share in the hair care sales. Although these stores can only carry a limited amount of product assortment, their share in sales has reached %25 in 2019. Another channel is cosmetics stores, which are generally individually operated. However, chain cosmetics outlets have recently emerged and start to gain rapid share. The share of cosmetics stores in hair care is about 25%, 14% of which belongs to chain cosmetics stores such as Watsons and Gratis. Another significant channel for hair care is pharmacies, which are generally individually operated and geographically dispersed. These account for %10 of all hair care sales. Companies and Brands of Hair Care Market Brand based market shares Unit Unit Unit (%) and average unit Share Share Share price in price in price in prices(for 400 ml.) (%) 2017 (%) 2018 (%) 2019 (2018) (2019) (2020) Geographic coverage Unilever group 90% (urban and rural) Dove 13,1 13 12,9 3 2.9 2,8 7 7,9 28 7 8 28 6,9 8 27,8 2,3 2,3 2.2 2.2 2.2 2.2 Clear Elidor Unilever Total P&G Group Pantene Blendax Rejoice Head&Shoulders P&G Total 3,2 17.8 5,8 18.1 6 4.8 5 33,9 18 5,8 4,8 4,9 33,5 3.4 2.1 2,3 2,9 92% (urban and rural) 3,1 2 2.2 2,7 2,2 2.8 4,8 33.2 Henkel&Schwarzkopf Gliss Kur Schauma Henkel&Schwarzkopf Total 65% (urban-Ankara, stanbul, zmir, Bursa, Gaziantep-less rural) 3 1,1 3.9 2.6 8,5 3,7 2.8 6.5 3.6 2.9 8,5 3.3 1,2 3.1 1.1 Loreal Group Elseve Loreal Total 60%(urban-Ankara, stanbul, zmir, Bursa, Gaziantep-less rural) 3,3 7.6 3,7 3,4 7.6 7,5 7,5 7,2 7.2 65% (limited urban-Anakara, stanbul, Izmir more rural) Canan Kozmetik pek Canan Total 1" 1" 8.1 8.1 8,4 8.4 8.7 1.1" 8,7 50%(both limited urban and rural) 1,2 1,2" 2.4 2,4 2.7 2.7 2.9 1.3 2.9 Hayat Group Hayat Hayat Total Others Duru, import brands, Own-brands Others Total The prices are for 1000ml. 13,5 13,5 13,3 13.4 13,7 13.7 The remaining revenue is believed to be generated in the traditional groceries and markets, which are again geographically scattered especially in the rural areas of Turkey. Although the big chains have their own distribution system and warehouses, they increasingly demand door-to-door supply to their stores to cut costs. Especially after Migros Group's acquisition by Anadolu Group, the strategy followed by the new owner seems to be cost leadership. Thus, Migros group recently intensified its demands for such a system. For now, you are not paying for distribution to the stores of Migros group, but they demand either a payment (500,000 annual) to contime current system or arrange a new distribution system that can assure reliable and timely supply of each store by your team. It is estimated that a medium ranged ERP package including software, hardware -servers, handware, RFID etc.-, installation) may cost around 900.000 and installation of a distribution network (including regional warehouses, motorized vehicles) may cost around 10 million . You should also consider that this installation will bring about %15 reduction in annual costs of operating the distribution network at your current size, of course). Currently your business is operated in stanbul. You have a big warehouse in Tuzla, Orhanl, where you keep the entire inventory of your company. Two personnel is working there and from time to time you outsource temporary workers to help warehouse sorting and arranging promotion products- such as producing two-in-one packages-. The distribution from your warehouse is either to chain stores or to your wholesaler/distributor. In order to reach geographically remote areas you are working with a distributor to sell markets, groceries, pharmacies and cosmetics stores. The distributor is responsible for delivering supplies and carries the necessary levels of inventory. Yet, you know that the distributor is complaining about carrying too much inventory and there are rumors about his financial condition in the market. According to your market analysis, if the distributor goes bankrupt alternative distributorship arrangements will probably cost you %8-10 more. In order to assure delivery, in-store shelf display, in-store promotions and other CRM activities you have a sales force that is composed of 30 sales people. These are grouped in Marmara, Aegean Mediterranean, Black Sea Ankara and East Anatolia Regions. Together with the 15 people in the stanbul office your total workforce is 45. At first glance your human resources seem adequate, yet the turnover is a bit high Among marketeers average tenure is 3 years whereas in sales it is 7 years. Comparisons show that all of your multinational rivals pay at least 20% more in wages. You know that Henkel acts as a reputable brand name in doing business and many of the chain stores treat you with respect because you are a member of Henkel family. However, in reality, Henkel group of companies in Turkey does not provide too much parenting and coordination. Even the closest business lines such as cleaning powders (Persil, Tursil), softeners (Vernel, Perwoll) and cleaning gels (Dixi, Pril) are structured as a separate company (Henkel Household Cleaning Products) and there is only minimal contact between this company and yours. The headquarters of Schwarzkopf-Henkel is located in Germany and the relationship between the parent has its ups and downs. Germany has followed a strategy of multiple foreign market entry in the 1990s, one of which was Turkey. Yet, the conditions and demand levels were not promising due to various politico- economic crises. So, Germany continually cut budgets and the brand equity was negatively affected from this negligence. This view has recently shifted as Turkish market progressed and Henkel group decided to divest its specialty chemical business to concentrate more on consumer goods. As a result, Henkel factory in Gebze, which produced major raw materials for the hair care as well as household cleaning products, was sold to Cognis in 2010. Yet, the deal required continuous and advantageous supply (not in terms of price but in terms of termin dates and supply guarantees) of necessary ingredients to Henkel group of companies for 8 years. You learned that Schauma brand shampoos and hair care products were launched in Turkey in 2004. It was initially targeted for the position of Elidor but the budget cuts after the 2001 crisis prevented achievement of that move and forced the brand to engage in price cuts as a last resort. As of now, Schauma is being marketed as a value-for-money" brand and in order to stay competitive and profitable it is locally produced. Local production is generally cheaper since production technology is simple and ingredients are cheap-also you still have advantages from Cognis-. Your intelligence data on the financials of competitors also reveal clues that the local production is cheaper. Unilever group produces all of its brands locally, wheras P&G locally produces all of its brands except some high-line products of Pantene and Head&Shoulders brands. Inside-company rumors suggest that P&G also wants to move its whole product assortment into local production. P&G's production site has around14-15 million liters annual capacity. Only multinational, which does not own a production plant in Turkey-except Henkel-Schwartzkopf-is Loreal and you hear rumors from Loreal side about serious consideration of this option. In 2012, they started to engage in an outsourcing agreement with a local producer -supposedly Canan Cosmetics-to manufacture their Elseve shampoos in Turkey. Yet, it is difficult to find local partners for production, which can keep up both with the capacity levels and the quality control standards of Henkel. Current partner is a small manufacturer, which was forced out of business in 2009 with its own brand. The production quality, delivery times and unit prices are satisfactory, however there is no excess capacity to produce any other brand in this factory. Thus, Gliss branded shampoos and hair care products are currently being imported from Germany. Imported goods have serious problems such as delivery termins and costly customs clearance procedures. On the other hand, imported products top their local counterparts on package quality. Gliss was a successful launch, thanks to expanding hair care market. It is being positioned between Dove and Elseve. However, marketing budgets are still tight. Below is the summary of your 2018, 2019 and 2020 income statements and estimation of your rivals. Income statements Henkel Henkel Unilever Unilever Unilever P&G 2018 2019 2019 2018 2019 sales 15,015 65,052 costs of goods sold materials imported goods employee" direct costs(energy) warehouse and logistics administrative expense marketing&sales expense total costs operating profit Henkel 2020 15,21 2018 64,68 2020 65,24 P&G P&G 2020 77,385 78,055 77,688 15,145 6,4 6.6 6,6 0.77 304 0.98 1.3 7.7 1.4 2 17,17 -2,155 0.79 3,07 0,97 1,35 7,8 0.8 3.1 0.98 1.38 7.9 4 5,4 17 5,9 9,5 482 16.48 1,45 6.5 6,6 3.9 3,9 42 4,1 5.9 5,9 18,6 18,6 72 7,1 12 11 58,3 57,2 19,085 20.855 4 5.4 17.1 5,8 9 479 17,34 6.6 3.9 4,1 5.95 18.7 7 11 57 25 20.438 5.45 172 5,9 9 48,15 16,902 1,5 2 17,64 2 17,43 -2,285 Henkel 2009 15.048 sales costs of goods sold materials imported goods employee direct costs(energy) warehouse and logistics administrative expense marketing sales expense total costs operating profit 0.8 3,3 0.85 0,95 7 1.3 2 10.2 -1,152 *Indicates costs of materials and packaging used in local production Indicates costs of employees employed in local production and warehouse Loral Loral Loreal Canan Canan Canan Hayat Hayat 2018 2019 2020 2018 2019 2020 2018 2019 17,325 17,475 16,848 19,404 19,572 20.358 8.237 6.291 1,07 1,09 1,06 32 3,3 3,3 0.74 0,75 1,03 1,3 6.7 1,07 1,35 6.7 2,5 1,03 1,35 6.7 1,61 3,4 9 1,65 3.5 9.1 1,65 3,5 9,1 0,71 1 4,4 0.9 0,7 1 4,45 0,9 0.72 1.03 4,5 2.4 3.4 0.5 0.5 16 1,325 15,91 1,565 15,54 1,308 1,7 21.41 -2006 1,6 21,65 -1.292 0.5 8,41 -1.824 Hayat 2020 sales 6,786 costs of goods sold materials 0.76 imported goods employee" direct costs(energy warehouse and logistics administrative expense 2,5 2.5 25 2,5 0,9 marketing&sales expense 3.2 3 total costs 21,75 8,25 8,3 operating profit -2,178 -2,013 -2,000 Indicates costs of materials and packaging used in local production * Indicates costs of employees employed in local production and warehouse Market leader and follower all use economics of scale advantages since they share their sourcing manufacturing, warehousing and distribution systems with other businesses. The level of coordination among SBUs in Unilever, P&G and Loreal is good to perfect. P&G and Unilever have their own distribution system, composed of regional warehouses and distribution vehicles that are fully controlled by ERP systems. Loreal has a similar distribution system to yours, yet they prefer not to distribute to more rural areas and work with better-more reputable, financially sound, large sized- distributors. Unilever group has enough production capacity which exceeds 15 million liters. Canan cosmetics has the largest local production site in Turkey which amounts to more than 20 million liters. The second largest production capacity is Tan Alizes, which has 15 million liters. But the infrastructure of the facility and its machinery and equipment are obsolete. Hayat group has a facility in Kocaeli, its hair care production capacity is 8 million liters. There are also many small companies in the consumer care business such as the one you are currently working with Yet, many of these companies have quality problems and small production capacity has a negative impact on unit production costs. Furthermore, due to recent competitive pressures in the industry, you heard that Loreal tends to make an offer to Canan in order to utilize it as a regional production center - although not publicly available there are rumors that they offered 35 million for 51% of the company- As of this year, Germany asks you about both your annual business plan and a medium ranged strategic plan (up to three years). You are aware that Schwarzkopf-Henkel has another brand in Hair Care (Poly Kur) which is positioned between Schauma and Gliss. Also, it is the market leader in Germany in kids market with the brand Schauina-for-kids. You are a legal holder of copyrights for these brands since you are a fully owned subsidiary. Furthermore, Schwartzkopf-Henkel always approaches new brand launches as a potential cash generator and thus, endorses such moves. In addition, you know that Germany has enough resources to finance more important strategic operations, such as acquisition of a local company-in case that ROIC (return on invested capital) rates are higher than 10%( annual terms). HENKEL-SCHWARZKOPF SHAMPOO CASE (TURKEY- December 2020) Suppose that you have just been appointed to the Henkel-Schwarzkopf Turkey affiliate as the Strategic Business Unit (SBU) manager for hair care division. There are three main SBUs in this affiliate, namely hair styling that markets Taft brand gels and styling products, colors which markets Vital and Palette branded hair dyes, and your SBU, which markets Gliss and Schauma brands as shampoos and hair care products. The biggest SBU in terms of sales is yours followed by colors and styling. Yet, according to the last year's figures your SBU cannot gain profit and market share. Gliss, one of your brands, was launched at the beginning of 2011 whereas Schauina has been competing in the market for almost 15 years. The size of the total hair care market in Turkey is estimated as much as 318 million . The biggest part of this market is composed of mass consumer market, which amounts to 233 million , followed by professional hair care market. Professional hair care market is composed of higher end brands that are tailored to hair saloons and not distributed to the public outlets, such as Kerastase, Bonacure, Hayashi and Sebastian. This market is dominated by Loreal and Eczacba-Schwarzkopf. The rest of the market is shared by many distributor company brands, which are extremely expensive and non-branded locally produced hair care products that are extremely cheap. Eczacba-Schwarzkopf is a totally different company (a 50-50 joint venture between Schwartzkopf and Eczacba Holding) which has no affiliation with Schwarzkopf-Henkel. There is a gentleman's agreement between Eczacba Holding and Schwarzkopf-Henkel that each company will not be rivals and will not sell products in each other's channels. The estimated size of the professional market is about 50 million . Loreal group gets %43 of this market followed by Eczacba-Schwazkopf with %33, distributor brands %10 and other non- branded, locally produced shampoos %13. It is estimated that Canan cosmetics, Tan Alize and Hayat group provides nearly all of these non-branded hair care products. The third portion of the market is composed of baby/kids market. This part of the market is dominated by Johnson and Johnson, Nivea and Dalin with approximately equal shares. The size of the kids market is believed to be 35 million . Below are the figures of Turkish hair care market progression in years./ Turkish Hair Care Market(Mass Consumer) 2001 2002 2003 2004 2005 2006 2007 145 150 160 170 181 192 205 0,000 0,034 0.067 0.053 0,065 0,061 0.073 2009 2009 2010 2011 2012 2013 2014 2015 2016 2017 2010 2019 2020 210 209 213 220 225 227 229 230 230 231 233 234 0,019 -0,005 0,019 0,033 0,023 0,009 0.018 0.004 0.004 0,009 -0,004 0,004 0.004 Years market szen min growth rate % of share according to product types 2 in 131 pisin shampoo creamhaircare 61 61 51 61 60 59 58 58 57 55 52 53 28 19 50 30 20 SO 30 20 29 19 50 30 20 48 30 47 32 11 12 14 15 17 17 17 17 17 18 19 As indicated in the above figures, generally consumer taste for shampoos is inclined to 2 in 1 type of shampoos. Although, it seems that offering more value for customer in one product serves right, the recent trend is shifting toward using separate products for distinguished end-values. Especially, at the high-end of the market consumers tend to buy shampoos for cleaning and creams/care products for hair treatment and rejuvenation. There are six major competing companies in the business, most of which are global leaders. These six players control almost 87% of the market and it is most likely that this domination will continue in the future. Below are the companies and brands with respective market shares for 2017, 2018 and 2019. Being a consumer product, distribution is of key importance in the hair care market. The most important channel for distribution has become the fast-growing supermarket-hypermarket chains. %40 of all hair care sales are generated in these outlets, which are primarily controlled by Carrefoursa, Migros, Real, Metro and Kipa. Another important channel for distribution is the discount chains, which have spread throughout the Turkey. Chain discounts such as A101, ok, BM and Mopas continually increase their share in the hair care sales. Although these stores can only carry a limited amount of product assortment, their share in sales has reached %25 in 2019. Another channel is cosmetics stores, which are generally individually operated. However, chain cosmetics outlets have recently emerged and start to gain rapid share. The share of cosmetics stores in hair care is about 25%, 14% of which belongs to chain cosmetics stores such as Watsons and Gratis. Another significant channel for hair care is pharmacies, which are generally individually operated and geographically dispersed. These account for %10 of all hair care sales. Companies and Brands of Hair Care Market Brand based market shares Unit Unit Unit (%) and average unit Share Share Share price in price in price in prices(for 400 ml.) (%) 2017 (%) 2018 (%) 2019 (2018) (2019) (2020) Geographic coverage Unilever group 90% (urban and rural) Dove 13,1 13 12,9 3 2.9 2,8 7 7,9 28 7 8 28 6,9 8 27,8 2,3 2,3 2.2 2.2 2.2 2.2 Clear Elidor Unilever Total P&G Group Pantene Blendax Rejoice Head&Shoulders P&G Total 3,2 17.8 5,8 18.1 6 4.8 5 33,9 18 5,8 4,8 4,9 33,5 3.4 2.1 2,3 2,9 92% (urban and rural) 3,1 2 2.2 2,7 2,2 2.8 4,8 33.2 Henkel&Schwarzkopf Gliss Kur Schauma Henkel&Schwarzkopf Total 65% (urban-Ankara, stanbul, zmir, Bursa, Gaziantep-less rural) 3 1,1 3.9 2.6 8,5 3,7 2.8 6.5 3.6 2.9 8,5 3.3 1,2 3.1 1.1 Loreal Group Elseve Loreal Total 60%(urban-Ankara, stanbul, zmir, Bursa, Gaziantep-less rural) 3,3 7.6 3,7 3,4 7.6 7,5 7,5 7,2 7.2 65% (limited urban-Anakara, stanbul, Izmir more rural) Canan Kozmetik pek Canan Total 1" 1" 8.1 8.1 8,4 8.4 8.7 1.1" 8,7 50%(both limited urban and rural) 1,2 1,2" 2.4 2,4 2.7 2.7 2.9 1.3 2.9 Hayat Group Hayat Hayat Total Others Duru, import brands, Own-brands Others Total The prices are for 1000ml. 13,5 13,5 13,3 13.4 13,7 13.7 The remaining revenue is believed to be generated in the traditional groceries and markets, which are again geographically scattered especially in the rural areas of Turkey. Although the big chains have their own distribution system and warehouses, they increasingly demand door-to-door supply to their stores to cut costs. Especially after Migros Group's acquisition by Anadolu Group, the strategy followed by the new owner seems to be cost leadership. Thus, Migros group recently intensified its demands for such a system. For now, you are not paying for distribution to the stores of Migros group, but they demand either a payment (500,000 annual) to contime current system or arrange a new distribution system that can assure reliable and timely supply of each store by your team. It is estimated that a medium ranged ERP package including software, hardware -servers, handware, RFID etc.-, installation) may cost around 900.000 and installation of a distribution network (including regional warehouses, motorized vehicles) may cost around 10 million . You should also consider that this installation will bring about %15 reduction in annual costs of operating the distribution network at your current size, of course). Currently your business is operated in stanbul. You have a big warehouse in Tuzla, Orhanl, where you keep the entire inventory of your company. Two personnel is working there and from time to time you outsource temporary workers to help warehouse sorting and arranging promotion products- such as producing two-in-one packages-. The distribution from your warehouse is either to chain stores or to your wholesaler/distributor. In order to reach geographically remote areas you are working with a distributor to sell markets, groceries, pharmacies and cosmetics stores. The distributor is responsible for delivering supplies and carries the necessary levels of inventory. Yet, you know that the distributor is complaining about carrying too much inventory and there are rumors about his financial condition in the market. According to your market analysis, if the distributor goes bankrupt alternative distributorship arrangements will probably cost you %8-10 more. In order to assure delivery, in-store shelf display, in-store promotions and other CRM activities you have a sales force that is composed of 30 sales people. These are grouped in Marmara, Aegean Mediterranean, Black Sea Ankara and East Anatolia Regions. Together with the 15 people in the stanbul office your total workforce is 45. At first glance your human resources seem adequate, yet the turnover is a bit high Among marketeers average tenure is 3 years whereas in sales it is 7 years. Comparisons show that all of your multinational rivals pay at least 20% more in wages. You know that Henkel acts as a reputable brand name in doing business and many of the chain stores treat you with respect because you are a member of Henkel family. However, in reality, Henkel group of companies in Turkey does not provide too much parenting and coordination. Even the closest business lines such as cleaning powders (Persil, Tursil), softeners (Vernel, Perwoll) and cleaning gels (Dixi, Pril) are structured as a separate company (Henkel Household Cleaning Products) and there is only minimal contact between this company and yours. The headquarters of Schwarzkopf-Henkel is located in Germany and the relationship between the parent has its ups and downs. Germany has followed a strategy of multiple foreign market entry in the 1990s, one of which was Turkey. Yet, the conditions and demand levels were not promising due to various politico- economic crises. So, Germany continually cut budgets and the brand equity was negatively affected from this negligence. This view has recently shifted as Turkish market progressed and Henkel group decided to divest its specialty chemical business to concentrate more on consumer goods. As a result, Henkel factory in Gebze, which produced major raw materials for the hair care as well as household cleaning products, was sold to Cognis in 2010. Yet, the deal required continuous and advantageous supply (not in terms of price but in terms of termin dates and supply guarantees) of necessary ingredients to Henkel group of companies for 8 years. You learned that Schauma brand shampoos and hair care products were launched in Turkey in 2004. It was initially targeted for the position of Elidor but the budget cuts after the 2001 crisis prevented achievement of that move and forced the brand to engage in price cuts as a last resort. As of now, Schauma is being marketed as a value-for-money" brand and in order to stay competitive and profitable it is locally produced. Local production is generally cheaper since production technology is simple and ingredients are cheap-also you still have advantages from Cognis-. Your intelligence data on the financials of competitors also reveal clues that the local production is cheaper. Unilever group produces all of its brands locally, wheras P&G locally produces all of its brands except some high-line products of Pantene and Head&Shoulders brands. Inside-company rumors suggest that P&G also wants to move its whole product assortment into local production. P&G's production site has around14-15 million liters annual capacity. Only multinational, which does not own a production plant in Turkey-except Henkel-Schwartzkopf-is Loreal and you hear rumors from Loreal side about serious consideration of this option. In 2012, they started to engage in an outsourcing agreement with a local producer -supposedly Canan Cosmetics-to manufacture their Elseve shampoos in Turkey. Yet, it is difficult to find local partners for production, which can keep up both with the capacity levels and the quality control standards of Henkel. Current partner is a small manufacturer, which was forced out of business in 2009 with its own brand. The production quality, delivery times and unit prices are satisfactory, however there is no excess capacity to produce any other brand in this factory. Thus, Gliss branded shampoos and hair care products are currently being imported from Germany. Imported goods have serious problems such as delivery termins and costly customs clearance procedures. On the other hand, imported products top their local counterparts on package quality. Gliss was a successful launch, thanks to expanding hair care market. It is being positioned between Dove and Elseve. However, marketing budgets are still tight. Below is the summary of your 2018, 2019 and 2020 income statements and estimation of your rivals. Income statements Henkel Henkel Unilever Unilever Unilever P&G 2018 2019 2019 2018 2019 sales 15,015 65,052 costs of goods sold materials imported goods employee" direct costs(energy) warehouse and logistics administrative expense marketing&sales expense total costs operating profit Henkel 2020 15,21 2018 64,68 2020 65,24 P&G P&G 2020 77,385 78,055 77,688 15,145 6,4 6.6 6,6 0.77 304 0.98 1.3 7.7 1.4 2 17,17 -2,155 0.79 3,07 0,97 1,35 7,8 0.8 3.1 0.98 1.38 7.9 4 5,4 17 5,9 9,5 482 16.48 1,45 6.5 6,6 3.9 3,9 42 4,1 5.9 5,9 18,6 18,6 72 7,1 12 11 58,3 57,2 19,085 20.855 4 5.4 17.1 5,8 9 479 17,34 6.6 3.9 4,1 5.95 18.7 7 11 57 25 20.438 5.45 172 5,9 9 48,15 16,902 1,5 2 17,64 2 17,43 -2,285 Henkel 2009 15.048 sales costs of goods sold materials imported goods employee direct costs(energy) warehouse and logistics administrative expense marketing sales expense total costs operating profit 0.8 3,3 0.85 0,95 7 1.3 2 10.2 -1,152 *Indicates costs of materials and packaging used in local production Indicates costs of employees employed in local production and warehouse Loral Loral Loreal Canan Canan Canan Hayat Hayat 2018 2019 2020 2018 2019 2020 2018 2019 17,325 17,475 16,848 19,404 19,572 20.358 8.237 6.291 1,07 1,09 1,06 32 3,3 3,3 0.74 0,75 1,03 1,3 6.7 1,07 1,35 6.7 2,5 1,03 1,35 6.7 1,61 3,4 9 1,65 3.5 9.1 1,65 3,5 9,1 0,71 1 4,4 0.9 0,7 1 4,45 0,9 0.72 1.03 4,5 2.4 3.4 0.5 0.5 16 1,325 15,91 1,565 15,54 1,308 1,7 21.41 -2006 1,6 21,65 -1.292 0.5 8,41 -1.824 Hayat 2020 sales 6,786 costs of goods sold materials 0.76 imported goods employee" direct costs(energy warehouse and logistics administrative expense 2,5 2.5 25 2,5 0,9 marketing&sales expense 3.2 3 total costs 21,75 8,25 8,3 operating profit -2,178 -2,013 -2,000 Indicates costs of materials and packaging used in local production * Indicates costs of employees employed in local production and warehouse Market leader and follower all use economics of scale advantages since they share their sourcing manufacturing, warehousing and distribution systems with other businesses. The level of coordination among SBUs in Unilever, P&G and Loreal is good to perfect. P&G and Unilever have their own distribution system, composed of regional warehouses and distribution vehicles that are fully controlled by ERP systems. Loreal has a similar distribution system to yours, yet they prefer not to distribute to more rural areas and work with better-more reputable, financially sound, large sized- distributors. Unilever group has enough production capacity which exceeds 15 million liters. Canan cosmetics has the largest local production site in Turkey which amounts to more than 20 million liters. The second largest production capacity is Tan Alizes, which has 15 million liters. But the infrastructure of the facility and its machinery and equipment are obsolete. Hayat group has a facility in Kocaeli, its hair care production capacity is 8 million liters. There are also many small companies in the consumer care business such as the one you are currently working with Yet, many of these companies have quality problems and small production capacity has a negative impact on unit production costs. Furthermore, due to recent competitive pressures in the industry, you heard that Loreal tends to make an offer to Canan in order to utilize it as a regional production center - although not publicly available there are rumors that they offered 35 million for 51% of the company- As of this year, Germany asks you about both your annual business plan and a medium ranged strategic plan (up to three years). You are aware that Schwarzkopf-Henkel has another brand in Hair Care (Poly Kur) which is positioned between Schauma and Gliss. Also, it is the market leader in Germany in kids market with the brand Schauina-for-kids. You are a legal holder of copyrights for these brands since you are a fully owned subsidiary. Furthermore, Schwartzkopf-Henkel always approaches new brand launches as a potential cash generator and thus, endorses such moves. In addition, you know that Germany has enough resources to finance more important strategic operations, such as acquisition of a local company-in case that ROIC (return on invested capital) rates are higher than 10%( annual terms)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts