Answered step by step

Verified Expert Solution

Question

1 Approved Answer

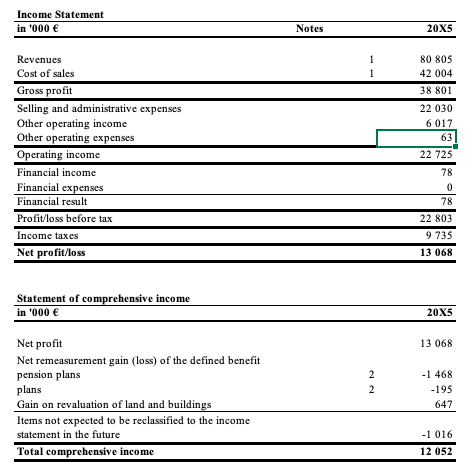

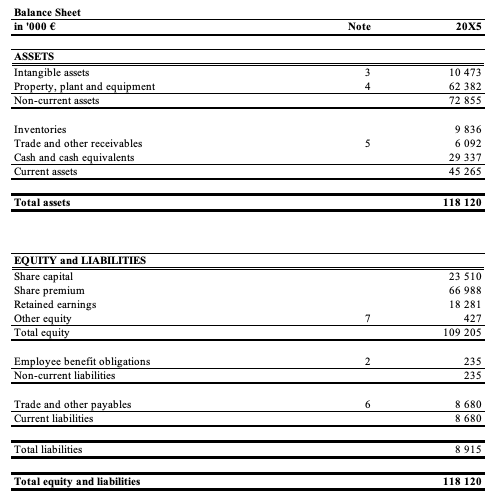

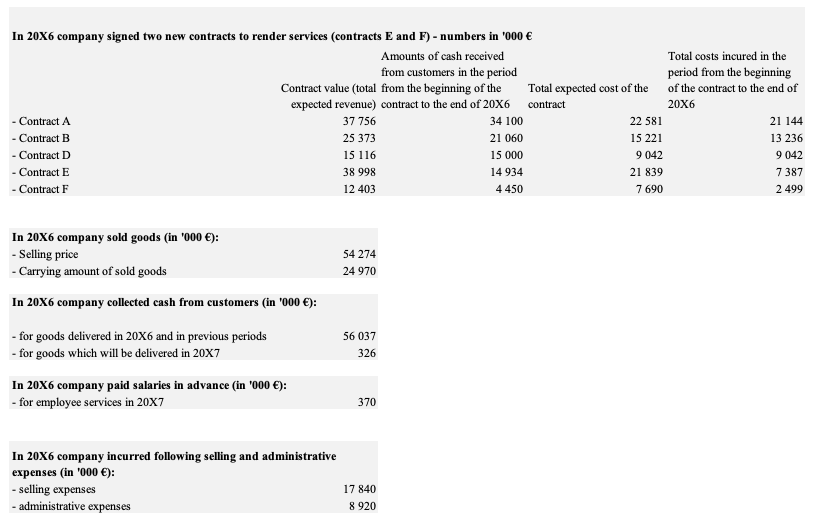

Create income statement and balance sheet for 2016 Income Statement in '000 Notes 20X5 1 1 80 805 42 004 38 801 Revenues Cost of

Create income statement and balance sheet for 2016

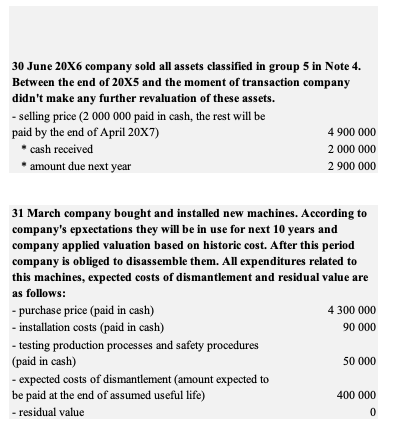

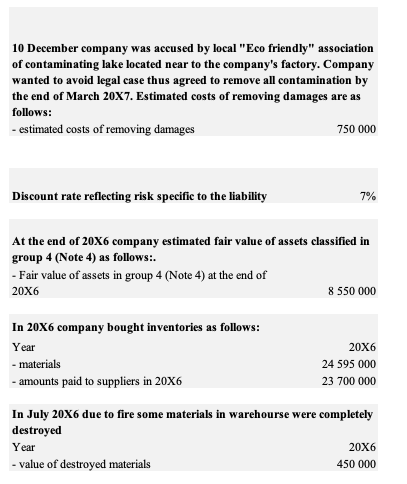

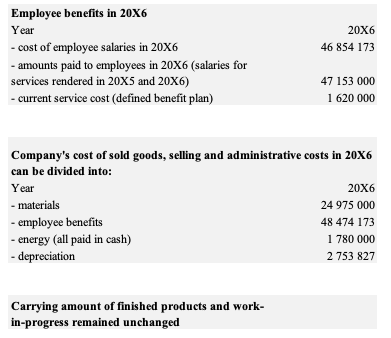

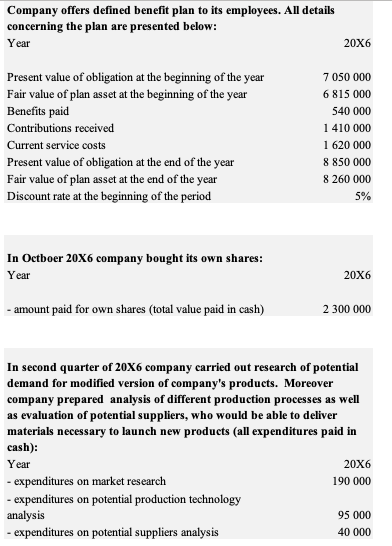

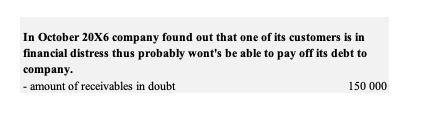

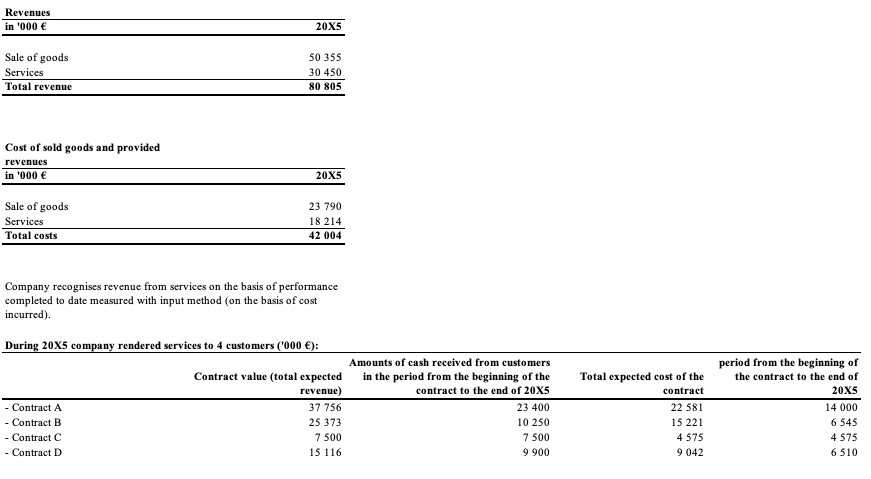

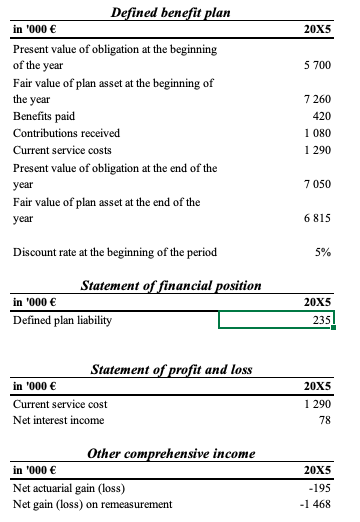

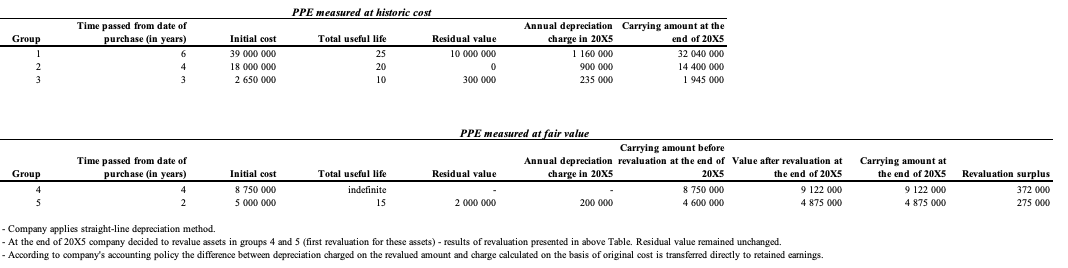

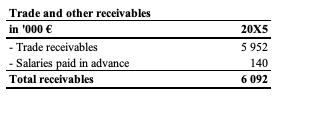

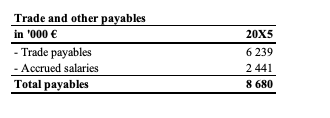

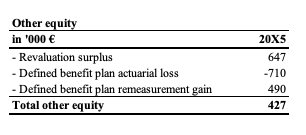

Income Statement in '000 Notes 20X5 1 1 80 805 42 004 38 801 Revenues Cost of sales Gross profit Selling and administrative expenses Other operating income Other operating expenses Operating income Financial income Financial expenses Financial result Profit/loss before tax Income taxes Net profit/loss 22 030 6 017 63 22 725 78 0 0 78 22 803 9 735 13 068 Statement of comprehensive income in '000 20X5 13 068 2 2 Net profit Net remeasurement gain (loss) of the defined benefit pension plans plans Gain on revaluation of land and buildings Items not expected to be reclassified to the income statement in the future Total comprehensive income -1 468 -195 647 -1 016 12 052 Balance Sheet in '000 Note 20X5 ASSETS Intangible assets Property, plant and equipment Non-current assets 3 4 10 473 62 382 72 855 5 Inventories Trade and other receivables Cash and cash equivalents Current assets 9 836 6092 29 337 45 265 Total assets 118 120 EQUITY and LIABILITIES Share capital Share premium Retained earnings Other equity Total equity 23 510 66 988 18 281 427 109 205 7 2 Employee benefit obligations Non-current liabilities 235 235 6 Trade and other payables Current liabilities 8 680 8 680 Total liabilities 8 915 Total equity and liabilities 118 120 In 20x6 company signed two new contracts to render services (contracts E and F) - numbers in '000 Amounts of cash received Total costs incured in the from customers in the period period from the beginning Contract value (total from the beginning of the Total expected cost of the of the contract to the end of expected revenue) contract to the end of 20x6 contract 20X6 - Contract A 37 756 34 100 22 581 21 144 - Contract B 25 373 21 060 15 221 13 236 - Contract D 15 116 15 000 9 042 9 042 - Contract E 38 998 14 934 21 839 7387 - Contract F 12 403 4450 7690 2 499 In 20x6 company sold goods (in '000 ): - Selling price - Carrying amount of sold goods 54 274 24 970 In 20x6 company collected cash from customers in '000 ): - for goods delivered in 20X6 and in previous periods - for goods which will be delivered in 20x7 56 037 326 In 20x6 company paid salaries in advance (in '000 ): - for employee services in 20x7 370 In 20x6 company incurred following selling and administrative expenses in '000 ): - selling expenses - administrative expenses 17 840 8 920 30 June 20x6 company sold all assets classified in group 5 in Note 4. Between the end of 20X5 and the moment of transaction company didn't make any further revaluation of these assets. - selling price (2 000 000 paid in cash, the rest will be paid by the end of April 20x7) 4 900 000 cash received 2 000 000 * amount due next year 2 900 000 31 March company bought and installed new machines. According to company's epxectations they will be in use for next 10 years and company applied valuation based on historic cost. After this period company is obliged to disassemble them. All expenditures related to this machines, expected costs of dismantlement and residual value are as follows: - purchase price (paid in cash) 4 300 000 - installation costs (paid in cash) 90 000 - testing production processes and safety procedures (paid in cash) 50 000 - expected costs of dismantlement (amount expected to be paid at the end of assumed useful life) 400 000 - residual value 0 10 December company was accused by local "Eco friendly" association of contaminating lake located near to the company's factory. Company wanted to avoid legal case thus agreed to remove all contamination by the end of March 20x7. Estimated costs of removing damages are as follows: - estimated costs of removing damages 750 000 Discount rate reflecting risk specific to the liability 7% At the end of 20x6 company estimated fair value of assets classified in group 4 (Note 4) as follows:. - Fair value of assets in group 4 (Note 4) at the end of 20X6 8 550 000 In 20x6 company bought inventories as follows: Year - materials - amounts paid to suppliers in 20X6 20X6 24 595 000 23 700 000 In July 20x6 due to fire some materials in warehourse were completely destroyed Year 20X6 - value of destroyed materials 450 000 20x6 46 854 173 Employee benefits in 20X6 Year - cost of employee salaries in 20X6 - amounts paid to employees in 20X6 (salaries for services rendered in 20x5 and 20X6) - current service cost (defined benefit plan) 47 153 000 1 620 000 Company's cost of sold goods, selling and administrative costs in 20X6 can be divided into: Year 20X6 - materials 24 975 000 - employee benefits 48 474 173 - energy (all paid in cash) 1 780 000 - depreciation 2 753 827 Carrying amount of finished products and work- in-progress remained unchanged Company offers defined benefit plan to its employees. All details concerning the plan are presented below: Year 20X6 Present value of obligation at the beginning of the year 7 050 000 Fair value of plan asset at the beginning of the year 6 815 000 Benefits paid 540 000 Contributions received 1 410 000 Current service costs 1 620 000 Present value of obligation at the end of the year 8 850 000 Fair value of plan asset at the end of the year 8 260 000 Discount rate at the beginning of the period 5% In Octboer 20x6 company bought its own shares: Year 20X6 - amount paid for own shares (total value paid in cash) 2 300 000 In second quarter of 20x6 company carried out research of potential demand for modified version of company's products. Moreover company prepared analysis of different production processes as well as evaluation of potential suppliers, who would be able to deliver materials necessary to launch new products (all expenditures paid in cash): 20X6 - expenditures on market research 190 000 - expenditures on potential production technology analysis 95 000 - expenditures on potential suppliers analysis 40 000 Year In October 20X6 company found out that one of its customers is in financial distress thus probably wont's be able to pay off its debt to company. - amount of receivables in doubt 150 000 Revenues in '000 20XS Sale of goods Services Total revenue 50 355 30 450 80 805 Cost of sold goods and provided revenues in '000 20XS Sale of goods Services Total costs 23 790 18 214 42 004 Company recognises revenue from services on the basis of performance completed to date measured with input method (on the basis of cost incurred). During 20x5 company rendered services to 4 customers ('000 ): - Contract A - Contract B - Contract C - Contract D Contract value (total expected revenue) 37 756 25 373 7 500 15 116 Amounts of cash received from customers in the period from the beginning of the contract to the end of 20x5 23 400 10 250 7 500 9 900 Total expected cost of the contract 22 581 15 221 4 575 9 042 period from the beginning of the contract to the end of 20X5 14 000 6 545 4 575 6 510 20X5 5 700 Defined benefit plan in '000 Present value of obligation at the beginning of the year Fair value of plan asset at the beginning of the year Benefits paid Contributions received Current service costs Present value of obligation at the end of the year Fair value of plan asset at the end of the year 7 260 420 1 080 1 290 7050 6 815 Discount rate at the beginning of the period 5% Statement of financial position in '000 Defined plan liability 20X5 235 Statement of profit and loss in '000 Current service cost Net interest income 20X5 1 290 78 Other comprehensive income in '000 Net actuarial gain (loss) Net gain (loss) on remeasurement 20X5 -195 -1 468 Intangible assets measured at historic cost Initial cost Group 6 Residual value Time passed from date of purchase (in years) 2 1 Annual depreciation Carrying amount at the charge in 20X5 end of 20X5 0 3 450 000 0 7 023 000 Total useful life indefinite indefinite 3 450 000 7 023 000 7 PPE measured at historic cost Total useful life Group 1 2 3 Time passed from date of purchase (in years) 6 6 4 3 Initial cost 39 000 000 18 000 000 2 650 000 25 20 10 Residual value 10 000 000 0 0 300 000 Annual depreciation Carrying amount at the charge in 20X5 end of 20X5 1 160 000 32 040 000 900 000 14 400 000 235 000 1 945 000 PPE measured at fair value Carrying amount before Time passed from date of Annual depreciation revaluation at the end of Value after revaluation at Group purchase (in years) Initial cost Total useful life Residual value charge in 20x5 20X5 the end of 20XS 4 4 8 750 000 indefinite 8 750 000 9 122 000 5 2 5 000 000 15 2 000 000 200 000 4 600 000 4 875 000 - Company applies straight-line depreciation method. - At the end of 20x5 company decided to revalue assets in groups 4 and 5 (first revaluation for these assets) - results of revaluation presented in above Table. Residual value remained unchanged. - According to company's accounting policy the difference between depreciation charged on the revalued amount and charge calculated on the basis of original cost is transferred directly to retained earnings. Carrying amount at the end of 20XS 9 122 000 4 875 000 Revaluation surplus 372 000 275 000 Trade and other receivables in '000 ' - Trade receivables - Salaries paid in advance Total receivables 20X5 5 952 140 6 092 Trade and other payables in '000 - Trade payables - Accrued salaries Total payables 20X5 6 239 2 441 8 680 8 Other equity in '000 - Revaluation surplus - Defined benefit plan actuarial loss - Defined benefit plan remeasurement gain Total other equity 20X5 647 -710 490 427 Income Statement in '000 Notes 20X5 1 1 80 805 42 004 38 801 Revenues Cost of sales Gross profit Selling and administrative expenses Other operating income Other operating expenses Operating income Financial income Financial expenses Financial result Profit/loss before tax Income taxes Net profit/loss 22 030 6 017 63 22 725 78 0 0 78 22 803 9 735 13 068 Statement of comprehensive income in '000 20X5 13 068 2 2 Net profit Net remeasurement gain (loss) of the defined benefit pension plans plans Gain on revaluation of land and buildings Items not expected to be reclassified to the income statement in the future Total comprehensive income -1 468 -195 647 -1 016 12 052 Balance Sheet in '000 Note 20X5 ASSETS Intangible assets Property, plant and equipment Non-current assets 3 4 10 473 62 382 72 855 5 Inventories Trade and other receivables Cash and cash equivalents Current assets 9 836 6092 29 337 45 265 Total assets 118 120 EQUITY and LIABILITIES Share capital Share premium Retained earnings Other equity Total equity 23 510 66 988 18 281 427 109 205 7 2 Employee benefit obligations Non-current liabilities 235 235 6 Trade and other payables Current liabilities 8 680 8 680 Total liabilities 8 915 Total equity and liabilities 118 120 In 20x6 company signed two new contracts to render services (contracts E and F) - numbers in '000 Amounts of cash received Total costs incured in the from customers in the period period from the beginning Contract value (total from the beginning of the Total expected cost of the of the contract to the end of expected revenue) contract to the end of 20x6 contract 20X6 - Contract A 37 756 34 100 22 581 21 144 - Contract B 25 373 21 060 15 221 13 236 - Contract D 15 116 15 000 9 042 9 042 - Contract E 38 998 14 934 21 839 7387 - Contract F 12 403 4450 7690 2 499 In 20x6 company sold goods (in '000 ): - Selling price - Carrying amount of sold goods 54 274 24 970 In 20x6 company collected cash from customers in '000 ): - for goods delivered in 20X6 and in previous periods - for goods which will be delivered in 20x7 56 037 326 In 20x6 company paid salaries in advance (in '000 ): - for employee services in 20x7 370 In 20x6 company incurred following selling and administrative expenses in '000 ): - selling expenses - administrative expenses 17 840 8 920 30 June 20x6 company sold all assets classified in group 5 in Note 4. Between the end of 20X5 and the moment of transaction company didn't make any further revaluation of these assets. - selling price (2 000 000 paid in cash, the rest will be paid by the end of April 20x7) 4 900 000 cash received 2 000 000 * amount due next year 2 900 000 31 March company bought and installed new machines. According to company's epxectations they will be in use for next 10 years and company applied valuation based on historic cost. After this period company is obliged to disassemble them. All expenditures related to this machines, expected costs of dismantlement and residual value are as follows: - purchase price (paid in cash) 4 300 000 - installation costs (paid in cash) 90 000 - testing production processes and safety procedures (paid in cash) 50 000 - expected costs of dismantlement (amount expected to be paid at the end of assumed useful life) 400 000 - residual value 0 10 December company was accused by local "Eco friendly" association of contaminating lake located near to the company's factory. Company wanted to avoid legal case thus agreed to remove all contamination by the end of March 20x7. Estimated costs of removing damages are as follows: - estimated costs of removing damages 750 000 Discount rate reflecting risk specific to the liability 7% At the end of 20x6 company estimated fair value of assets classified in group 4 (Note 4) as follows:. - Fair value of assets in group 4 (Note 4) at the end of 20X6 8 550 000 In 20x6 company bought inventories as follows: Year - materials - amounts paid to suppliers in 20X6 20X6 24 595 000 23 700 000 In July 20x6 due to fire some materials in warehourse were completely destroyed Year 20X6 - value of destroyed materials 450 000 20x6 46 854 173 Employee benefits in 20X6 Year - cost of employee salaries in 20X6 - amounts paid to employees in 20X6 (salaries for services rendered in 20x5 and 20X6) - current service cost (defined benefit plan) 47 153 000 1 620 000 Company's cost of sold goods, selling and administrative costs in 20X6 can be divided into: Year 20X6 - materials 24 975 000 - employee benefits 48 474 173 - energy (all paid in cash) 1 780 000 - depreciation 2 753 827 Carrying amount of finished products and work- in-progress remained unchanged Company offers defined benefit plan to its employees. All details concerning the plan are presented below: Year 20X6 Present value of obligation at the beginning of the year 7 050 000 Fair value of plan asset at the beginning of the year 6 815 000 Benefits paid 540 000 Contributions received 1 410 000 Current service costs 1 620 000 Present value of obligation at the end of the year 8 850 000 Fair value of plan asset at the end of the year 8 260 000 Discount rate at the beginning of the period 5% In Octboer 20x6 company bought its own shares: Year 20X6 - amount paid for own shares (total value paid in cash) 2 300 000 In second quarter of 20x6 company carried out research of potential demand for modified version of company's products. Moreover company prepared analysis of different production processes as well as evaluation of potential suppliers, who would be able to deliver materials necessary to launch new products (all expenditures paid in cash): 20X6 - expenditures on market research 190 000 - expenditures on potential production technology analysis 95 000 - expenditures on potential suppliers analysis 40 000 Year In October 20X6 company found out that one of its customers is in financial distress thus probably wont's be able to pay off its debt to company. - amount of receivables in doubt 150 000 Revenues in '000 20XS Sale of goods Services Total revenue 50 355 30 450 80 805 Cost of sold goods and provided revenues in '000 20XS Sale of goods Services Total costs 23 790 18 214 42 004 Company recognises revenue from services on the basis of performance completed to date measured with input method (on the basis of cost incurred). During 20x5 company rendered services to 4 customers ('000 ): - Contract A - Contract B - Contract C - Contract D Contract value (total expected revenue) 37 756 25 373 7 500 15 116 Amounts of cash received from customers in the period from the beginning of the contract to the end of 20x5 23 400 10 250 7 500 9 900 Total expected cost of the contract 22 581 15 221 4 575 9 042 period from the beginning of the contract to the end of 20X5 14 000 6 545 4 575 6 510 20X5 5 700 Defined benefit plan in '000 Present value of obligation at the beginning of the year Fair value of plan asset at the beginning of the year Benefits paid Contributions received Current service costs Present value of obligation at the end of the year Fair value of plan asset at the end of the year 7 260 420 1 080 1 290 7050 6 815 Discount rate at the beginning of the period 5% Statement of financial position in '000 Defined plan liability 20X5 235 Statement of profit and loss in '000 Current service cost Net interest income 20X5 1 290 78 Other comprehensive income in '000 Net actuarial gain (loss) Net gain (loss) on remeasurement 20X5 -195 -1 468 Intangible assets measured at historic cost Initial cost Group 6 Residual value Time passed from date of purchase (in years) 2 1 Annual depreciation Carrying amount at the charge in 20X5 end of 20X5 0 3 450 000 0 7 023 000 Total useful life indefinite indefinite 3 450 000 7 023 000 7 PPE measured at historic cost Total useful life Group 1 2 3 Time passed from date of purchase (in years) 6 6 4 3 Initial cost 39 000 000 18 000 000 2 650 000 25 20 10 Residual value 10 000 000 0 0 300 000 Annual depreciation Carrying amount at the charge in 20X5 end of 20X5 1 160 000 32 040 000 900 000 14 400 000 235 000 1 945 000 PPE measured at fair value Carrying amount before Time passed from date of Annual depreciation revaluation at the end of Value after revaluation at Group purchase (in years) Initial cost Total useful life Residual value charge in 20x5 20X5 the end of 20XS 4 4 8 750 000 indefinite 8 750 000 9 122 000 5 2 5 000 000 15 2 000 000 200 000 4 600 000 4 875 000 - Company applies straight-line depreciation method. - At the end of 20x5 company decided to revalue assets in groups 4 and 5 (first revaluation for these assets) - results of revaluation presented in above Table. Residual value remained unchanged. - According to company's accounting policy the difference between depreciation charged on the revalued amount and charge calculated on the basis of original cost is transferred directly to retained earnings. Carrying amount at the end of 20XS 9 122 000 4 875 000 Revaluation surplus 372 000 275 000 Trade and other receivables in '000 ' - Trade receivables - Salaries paid in advance Total receivables 20X5 5 952 140 6 092 Trade and other payables in '000 - Trade payables - Accrued salaries Total payables 20X5 6 239 2 441 8 680 8 Other equity in '000 - Revaluation surplus - Defined benefit plan actuarial loss - Defined benefit plan remeasurement gain Total other equity 20X5 647 -710 490 427

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Forensic Accounting And Fraud Investigation For Non-Experts

Authors: Stephen Pedneault, Frank Rudewicz, Howard Silverstone, Michael Sheetz

3rd Edition

0470879599, 9780470879597