Question

Credit risk measures using the reduced form model: assume a company has the following values for its debt issue. Face value of the firms debt:

Credit risk measures using the reduced form model: assume a company has the following values for its debt issue.

Face value of the firms debt: K = $1,000

Time to maturity of the debt (tenor): T t = 1 year (T = maturity)

Default intensity (approx prob of default per year): = 0.03

Loss given default: = 0.3 (30%)

P(t,T) = 0.95

(a) Calculate the probability that the debt will default over the time to maturity.

(b) Calculate the expected loss.

(c) Calculate the present value of the expected loss.

Show all calculations All prices and interest rates must be expressed to three decimal places

I have added an example question below the way the professor wants his answers to be.

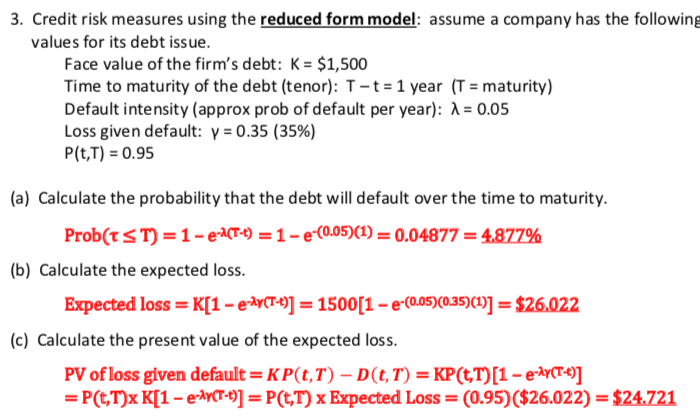

3. Credit risk measures using the reduced form model: assume a company has the following values for its debt issue. Face value of the firm's debt: K = $1,500 Time to maturity of the debt (tenor): T - t = 1 year (T = maturity) Default intensity (approx prob of default per year): 1 = 0.05 Loss given default: p = 0.35 (35%) P(t,T) = 0.95 (a) Calculate the probability that the debt will default over the time to maturity. Prob(TST) = 1 - E-UCT-1) = 1 - e-(0.05)(1) = 0.04877 = 4.877% (b) Calculate the expected loss. Expected loss = K[1 e-AY(T-1)] = 1500[1 e-(0.05)(0.35)(1)] = $26.022 (c) Calculate the present value of the expected loss. PV of loss given default = K P(t,T) - D(t, T) = KP(t,T)[1 e-A%CT-6)] = P(t,T)x K[1 - e-AYCT-t)] = P(t,T) x Expected Loss = (0.95) ($26.022) = $24.721

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance A Quantitative Introduction

Authors: Nico Van Der Wijst

1st Edition

1107029228, 978-1107029224