Answered step by step

Verified Expert Solution

Question

1 Approved Answer

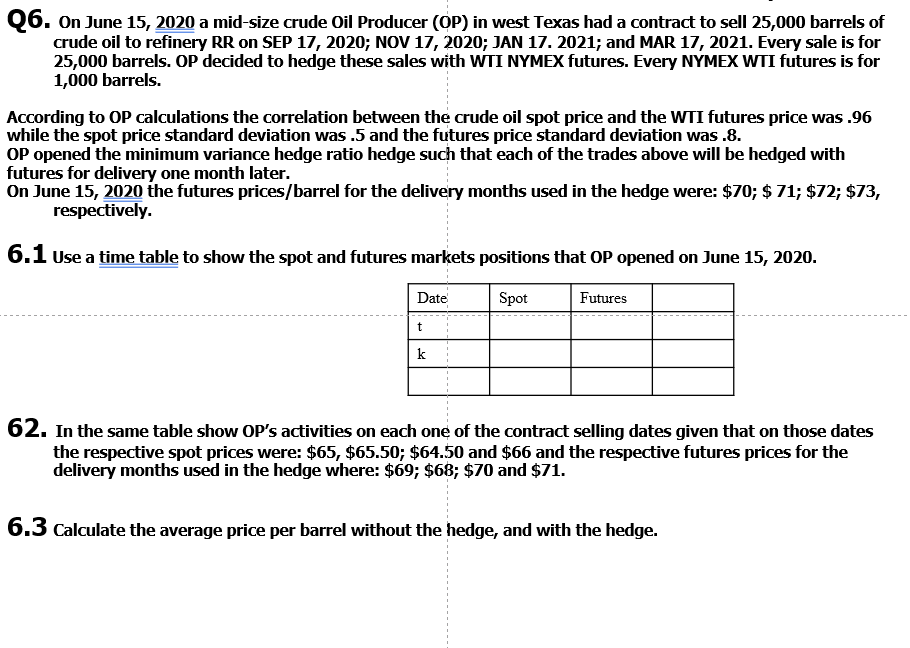

crude oil to refinery RR on SEP 17, 2020; NOV 17, 2020; JAN 17. 2021; and MAR 17, 2021 . Every sale is for 25,000

crude oil to refinery RR on SEP 17, 2020; NOV 17, 2020; JAN 17. 2021; and MAR 17, 2021 . Every sale is for 25,000 barrels. OP decided to hedge these sales with WTI NYMEX futures. Every NYMEX WTI futures is for 1,000 barrels. According to OP calculations the correlation between the crude oil spot price and the WTI futures price was .96 while the spot price standard deviation was .5 and the futures price standard deviation was .8. OP opened the minimum variance hedge ratio hedge such that each of the trades above will be hedged with futures for delivery one month later. On June 15, 2020 the futures prices/barrel for the delivery months used in the hedge were: $70;$71;$72;$73, respectively. 6.1 Use a time table to show the spot and futures markets positions that OP opened on June 15, 2020. 62. In the same table show OP 's activities on each one of the contract selling dates given that on those dates the respective spot prices were: $65,$65.50;$64.50 and $66 and the respective futures prices for the delivery months used in the hedge where: $69;$68;$70 and $71. 6.3 Calculate the average price per barrel without the hedge, and with the hedge

crude oil to refinery RR on SEP 17, 2020; NOV 17, 2020; JAN 17. 2021; and MAR 17, 2021 . Every sale is for 25,000 barrels. OP decided to hedge these sales with WTI NYMEX futures. Every NYMEX WTI futures is for 1,000 barrels. According to OP calculations the correlation between the crude oil spot price and the WTI futures price was .96 while the spot price standard deviation was .5 and the futures price standard deviation was .8. OP opened the minimum variance hedge ratio hedge such that each of the trades above will be hedged with futures for delivery one month later. On June 15, 2020 the futures prices/barrel for the delivery months used in the hedge were: $70;$71;$72;$73, respectively. 6.1 Use a time table to show the spot and futures markets positions that OP opened on June 15, 2020. 62. In the same table show OP 's activities on each one of the contract selling dates given that on those dates the respective spot prices were: $65,$65.50;$64.50 and $66 and the respective futures prices for the delivery months used in the hedge where: $69;$68;$70 and $71. 6.3 Calculate the average price per barrel without the hedge, and with the hedge Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Total Inventors Manual

Authors: Sean Michael Ragan

1st Edition

1681881586, 978-1681881584