Answered step by step

Verified Expert Solution

Question

1 Approved Answer

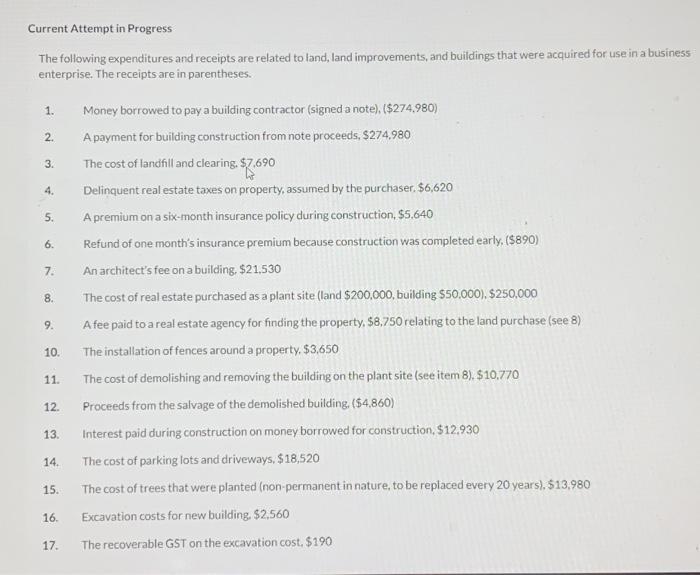

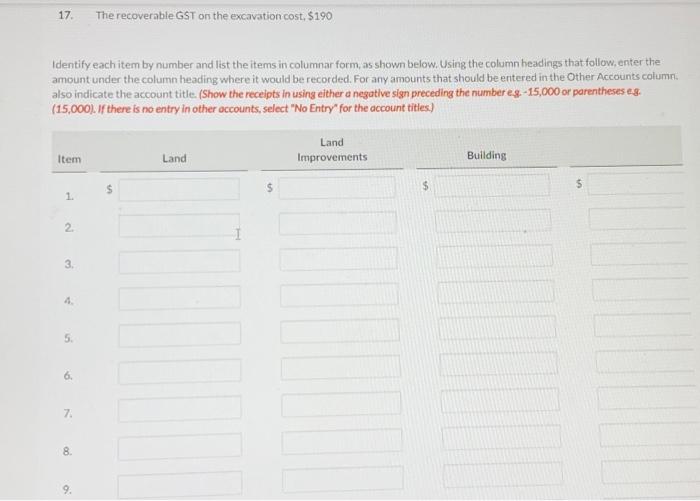

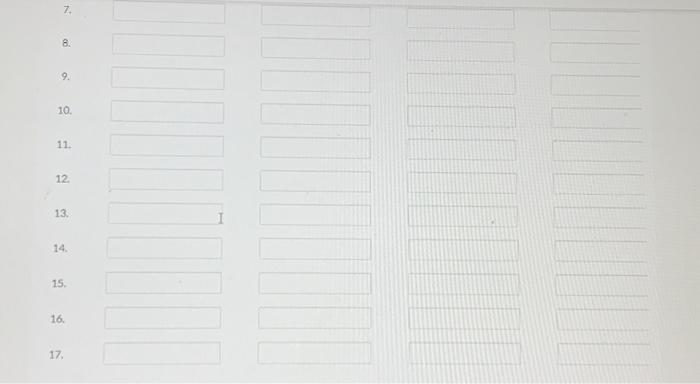

Current Attempt in Progress The following expenditures and receipts are related to land, land improvements, and buildings that were acquired for use in a business

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting For MBAs

Authors: Peter Easton, Robert Halsey, Mary Lea McAnally, John Wild

8th Edition

1618533584, 9781618533586