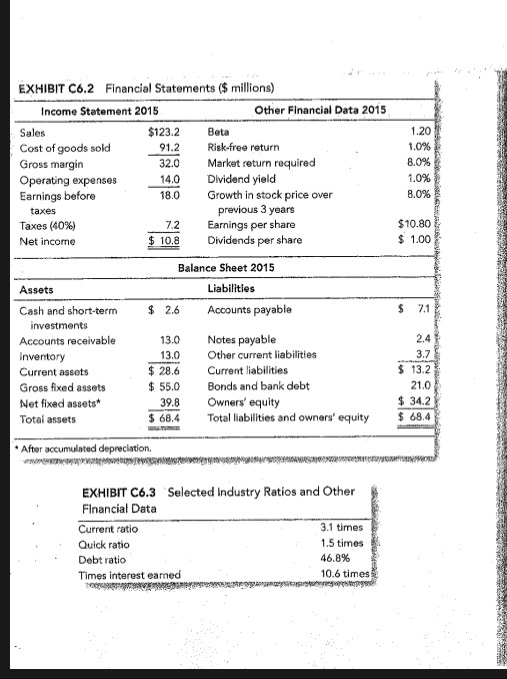

D 1. Using information from the case and also from Exhibits 6.1 and 6.2 develop a pro forma income statement for 2016. Assume that depreciation equals the 2015 amount plus one-sixth of 2016 capital spending. The relevant company tax rate is 40%. Enter answer... D 2. Using information from the pro forma income statement derived in #1, and also Exhibits C 6.2 and 6.3 and other case information, calculate the inventory for 2016. (Hint: First, calculate inventory turnover and then calculate inventory by dividing COGS by the inventory turnover number. Remember, you are calculating the 2016 inventory.). Show all calculations Enter answer... D 3. Using 2016 pro forma sales information, calculate and forecast the amount of payables for 2016. Show all calculations. SU CASS SIX US Young Brands OUNG BRANDS (YB) is a manufacturer of sports clothing and team uniforms. Its industry is quite competitive, so the management team has attempted to operate a modern operation with state-of-the-art production facilities. Careful cost management has been an important factor in attaining profits. YB is considered a leader for its fashion sense, pricing, market- ing, and product quality. Professional and university-team uniforms and affiliated products are sold by company salesmen to teams and to retail stores throughout North America. YB currently uses a network of manufacturers' representatives to reach retailers in Europe, Latin America, and Asia. (A manufacturer's rep resentative (MR) is an independent individual, sales agency, or company that sells a manufacturer's products to wholesale and retail customers in foreign countries.) There is a large demand for licensed (approved) clothing with team logos and colors, and premium prices can be charged to retail customers who buy for themselves as fans, for friends and relatives as gifts, or simply to affiliate with a local (hopefully winning) team. The licensed clothing line includes sweatshirts 245 246 Young Brands caps: Jogging suits: baseball, football, and hockey shirts and various accesso-4 ries (such as tote bags, scarves, and towels) DE CHANGES IN YB'S GLOBAL MARKETING STRATEGY About a year ago, the senior managers concluded that YB products in global markets were "underappreciated and that "sales could-and should-be substantially higher." See Exhibit 06.1 for recent global sales results. They reasoned that trade shows in the major international markets are a relatively Inexpensive way to display the company's products and provide an opportunity to meet major corporate buyers face to face That is precisely what happened. The firm's exhibits were impressive, for- mer athletes were used as spokespersons, and the company made important contacts with Asian and European buyers. The long-term plan is to eliminate the use of MRs and to sell directly to major retail chains. This will improve market saturation in metropolitan areas and end the commissions paid to the MR network (currently about 6 percent of revenue on average). As a result of this, YB's sales growth is expected to increase sharply in the next three years, and revenues are estimated to more than double by the end of 2018. The marketing vice president forecasts worldwide sales of $160 million in 2016. $200 million in 2017 and $250 million in 2018. Management is pleased with the forecast because it is evidence of what they have long believed that the company manufactures quality products with global appeal at a reason- able price. The downside is that such growth will undoubtedly require external financing and could cause administrative and operational difficulties. Although YB will explore a number of financing alternatives, it is recog- nized that the first step is to estimate the external funds needed for the period ahead. After all, before a financing option is explored, a reasonable projection EXHIBIT C6.1 Recent Financial Results Sales Price-Earnings Smillions Ratio (times) 2015 $1232 11.4 2014 $111.3 13.5 2013 $1046 2012 $1010 142 2011 $ 96.4 14.0 Working Capital Issues : 247 must be made of what needs to be raised. And it is even possible that a portion of the expected growth can be internally financed FORECASTING CONSIDERATIONS In order to develop the forecast, the president, Henry Gilmore, called a group meeting of his senior managers. All agree that the sales projections are quite reasonable" in view of the activity resulting from the trade shows and the global obsession with sports teams and competitions, and may even be a bit low. They also decide to concentrate on the 2016 forecast at their initial meeting. A few months ago. YB began Implementing a number of cost-cutting mea- sures that are expected to generate a 32 percent gross margin each year of the forecast. Due to economies of scale, operating expenses are expected to increase less than proportionately with sales, and the manager group agrees to a 20 percent increase in 2016. The relevant tax rate is 40 percent. The purchasing vice president noted that the financial forecast needs to consider the tighter credit terms offered by many of the firm's suppliers. Com- pany records show that two years ago, about 70 percent of YB's purchases were on terms of 2/10, net 30. That is, most suppliers offered a 2 percent discount to customers who paid within 10 days, with full payment expected by day 30. "We always took the discount when it was offered." Company records show that during the past year, about half of the suppli- ers offered the 2/10, net 30, discount. Fewer vendors are likely to offer cash dis- counts in the future, which will impact the firm's gross margin due to slightly higher prices paid for materials. Therefore, he recommends that the gross mar- gin estimate be reduced to 31 percent, which the group accepts. 693 WORKING CAPITAL ISSUES The discussion then turned to working capital management. Inventory control has been a problem for YB at times. Some in the group believe that inventory turnover can be increased to eight times mainly by using suppliers with shorter delivery times. Others are skeptical, believing that it is unrealistic to think that inventory management can be improved unless there is specific evidence to support this conclusion. The group finally concurs that an estimate based on historical inventory patterns is appropriate. Given the new global customer base, it is clear that the firm's historical experience with its accounts receivable will be of little help in predicting future Z Young oras receivables. For the purpose of this forecast, the group decides to assume that they will offer credit terms of net 30 and that 50 percent of customers will pay on time and all other receivables will be received in 50 days. YB expects that this experience will improve in future years. The marketing vice president is tasked with the responsibility of making payment terms clear to the new foreign buyers, and to working with YB's banks to establish letter of credit facilities. (A letter of credit is a document issued by a bank ensuring payment to a seller of goods, provided certain documents have been presented to the bank. These are documents that prove that the seller bas performed the duties under an underlying sales contract and the goods have been supplied as agreed.) The group expects that nearly all sales will be collected, and it estimates that bad debt expense will be "insignificant" and can be ignored. The group also thinks that cash should be 4 percent of sales. The firm's predicted 2016 spending on fixed assets is $35 million. These expenditures partly reflect the replacement of existing equipment but mainly result from the new facilities necessary to accommodate the growth in sales. The note payable will require a 20 percent payoff in 2016. Other current liabilities will increase at the same rate as sales. Bxisting bond debt and bank loans will require an average payoff of 15 percent of the principal amount. FINANCIAL ISSUES YB will pay $1 million in dividends during 2016, the same amount as in 2015. Although this might appear stingy, the group believes that most profits should be reinvested in the aggressive plans for global growth. Ignore any interest expense for the purpose of calculating the 2016 financial statements. The group realizes that it is likely that most of any new required funds will be borrowed. The finance vice president says he has enough information to develop an estimate for 2016, 91.2 EXHIBIT C6.2 Financial Statements ($ millions) Income Statement 2015 Other Financial Data 2015 Sales $123.2 Beta Cost of goods sold Risk-free return Gross margin Market return required Operating expenses Dividend yield Earnings before Growth in stock price over previous 3 years Taxes (40%) Earnings per share Net income $ 10.8 Dividends per share 180 taxes $10.80 Balance Sheet 2015 Liabilities $ 2.6 Accounts payable IN Assets Cash and short-term investments Accounts receivable Inventory Current assets Gross fixed assets Net fixed assets Total assets 13.0 13.0 $ 28.6 $ 55.0 39.8 $ 68.4 Notes payable Other current liabilities Current liabilities Bonds and bank debt Owners' equity Total liabilities and owners' equity DINO * After accumulated depreciation EXHIBIT C6.3 Selected Industry Ratios and Other Financial Data Current ratio 3.1 times Quick ratio 1.5 times Debt ratio 46.8% Times interest earned 10.6 times D 1. Using information from the case and also from Exhibits 6.1 and 6.2 develop a pro forma income statement for 2016. Assume that depreciation equals the 2015 amount plus one-sixth of 2016 capital spending. The relevant company tax rate is 40%. Enter answer... D 2. Using information from the pro forma income statement derived in #1, and also Exhibits C 6.2 and 6.3 and other case information, calculate the inventory for 2016. (Hint: First, calculate inventory turnover and then calculate inventory by dividing COGS by the inventory turnover number. Remember, you are calculating the 2016 inventory.). Show all calculations Enter answer... D 3. Using 2016 pro forma sales information, calculate and forecast the amount of payables for 2016. Show all calculations. SU CASS SIX US Young Brands OUNG BRANDS (YB) is a manufacturer of sports clothing and team uniforms. Its industry is quite competitive, so the management team has attempted to operate a modern operation with state-of-the-art production facilities. Careful cost management has been an important factor in attaining profits. YB is considered a leader for its fashion sense, pricing, market- ing, and product quality. Professional and university-team uniforms and affiliated products are sold by company salesmen to teams and to retail stores throughout North America. YB currently uses a network of manufacturers' representatives to reach retailers in Europe, Latin America, and Asia. (A manufacturer's rep resentative (MR) is an independent individual, sales agency, or company that sells a manufacturer's products to wholesale and retail customers in foreign countries.) There is a large demand for licensed (approved) clothing with team logos and colors, and premium prices can be charged to retail customers who buy for themselves as fans, for friends and relatives as gifts, or simply to affiliate with a local (hopefully winning) team. The licensed clothing line includes sweatshirts 245 246 Young Brands caps: Jogging suits: baseball, football, and hockey shirts and various accesso-4 ries (such as tote bags, scarves, and towels) DE CHANGES IN YB'S GLOBAL MARKETING STRATEGY About a year ago, the senior managers concluded that YB products in global markets were "underappreciated and that "sales could-and should-be substantially higher." See Exhibit 06.1 for recent global sales results. They reasoned that trade shows in the major international markets are a relatively Inexpensive way to display the company's products and provide an opportunity to meet major corporate buyers face to face That is precisely what happened. The firm's exhibits were impressive, for- mer athletes were used as spokespersons, and the company made important contacts with Asian and European buyers. The long-term plan is to eliminate the use of MRs and to sell directly to major retail chains. This will improve market saturation in metropolitan areas and end the commissions paid to the MR network (currently about 6 percent of revenue on average). As a result of this, YB's sales growth is expected to increase sharply in the next three years, and revenues are estimated to more than double by the end of 2018. The marketing vice president forecasts worldwide sales of $160 million in 2016. $200 million in 2017 and $250 million in 2018. Management is pleased with the forecast because it is evidence of what they have long believed that the company manufactures quality products with global appeal at a reason- able price. The downside is that such growth will undoubtedly require external financing and could cause administrative and operational difficulties. Although YB will explore a number of financing alternatives, it is recog- nized that the first step is to estimate the external funds needed for the period ahead. After all, before a financing option is explored, a reasonable projection EXHIBIT C6.1 Recent Financial Results Sales Price-Earnings Smillions Ratio (times) 2015 $1232 11.4 2014 $111.3 13.5 2013 $1046 2012 $1010 142 2011 $ 96.4 14.0 Working Capital Issues : 247 must be made of what needs to be raised. And it is even possible that a portion of the expected growth can be internally financed FORECASTING CONSIDERATIONS In order to develop the forecast, the president, Henry Gilmore, called a group meeting of his senior managers. All agree that the sales projections are quite reasonable" in view of the activity resulting from the trade shows and the global obsession with sports teams and competitions, and may even be a bit low. They also decide to concentrate on the 2016 forecast at their initial meeting. A few months ago. YB began Implementing a number of cost-cutting mea- sures that are expected to generate a 32 percent gross margin each year of the forecast. Due to economies of scale, operating expenses are expected to increase less than proportionately with sales, and the manager group agrees to a 20 percent increase in 2016. The relevant tax rate is 40 percent. The purchasing vice president noted that the financial forecast needs to consider the tighter credit terms offered by many of the firm's suppliers. Com- pany records show that two years ago, about 70 percent of YB's purchases were on terms of 2/10, net 30. That is, most suppliers offered a 2 percent discount to customers who paid within 10 days, with full payment expected by day 30. "We always took the discount when it was offered." Company records show that during the past year, about half of the suppli- ers offered the 2/10, net 30, discount. Fewer vendors are likely to offer cash dis- counts in the future, which will impact the firm's gross margin due to slightly higher prices paid for materials. Therefore, he recommends that the gross mar- gin estimate be reduced to 31 percent, which the group accepts. 693 WORKING CAPITAL ISSUES The discussion then turned to working capital management. Inventory control has been a problem for YB at times. Some in the group believe that inventory turnover can be increased to eight times mainly by using suppliers with shorter delivery times. Others are skeptical, believing that it is unrealistic to think that inventory management can be improved unless there is specific evidence to support this conclusion. The group finally concurs that an estimate based on historical inventory patterns is appropriate. Given the new global customer base, it is clear that the firm's historical experience with its accounts receivable will be of little help in predicting future Z Young oras receivables. For the purpose of this forecast, the group decides to assume that they will offer credit terms of net 30 and that 50 percent of customers will pay on time and all other receivables will be received in 50 days. YB expects that this experience will improve in future years. The marketing vice president is tasked with the responsibility of making payment terms clear to the new foreign buyers, and to working with YB's banks to establish letter of credit facilities. (A letter of credit is a document issued by a bank ensuring payment to a seller of goods, provided certain documents have been presented to the bank. These are documents that prove that the seller bas performed the duties under an underlying sales contract and the goods have been supplied as agreed.) The group expects that nearly all sales will be collected, and it estimates that bad debt expense will be "insignificant" and can be ignored. The group also thinks that cash should be 4 percent of sales. The firm's predicted 2016 spending on fixed assets is $35 million. These expenditures partly reflect the replacement of existing equipment but mainly result from the new facilities necessary to accommodate the growth in sales. The note payable will require a 20 percent payoff in 2016. Other current liabilities will increase at the same rate as sales. Bxisting bond debt and bank loans will require an average payoff of 15 percent of the principal amount. FINANCIAL ISSUES YB will pay $1 million in dividends during 2016, the same amount as in 2015. Although this might appear stingy, the group believes that most profits should be reinvested in the aggressive plans for global growth. Ignore any interest expense for the purpose of calculating the 2016 financial statements. The group realizes that it is likely that most of any new required funds will be borrowed. The finance vice president says he has enough information to develop an estimate for 2016, 91.2 EXHIBIT C6.2 Financial Statements ($ millions) Income Statement 2015 Other Financial Data 2015 Sales $123.2 Beta Cost of goods sold Risk-free return Gross margin Market return required Operating expenses Dividend yield Earnings before Growth in stock price over previous 3 years Taxes (40%) Earnings per share Net income $ 10.8 Dividends per share 180 taxes $10.80 Balance Sheet 2015 Liabilities $ 2.6 Accounts payable IN Assets Cash and short-term investments Accounts receivable Inventory Current assets Gross fixed assets Net fixed assets Total assets 13.0 13.0 $ 28.6 $ 55.0 39.8 $ 68.4 Notes payable Other current liabilities Current liabilities Bonds and bank debt Owners' equity Total liabilities and owners' equity DINO * After accumulated depreciation EXHIBIT C6.3 Selected Industry Ratios and Other Financial Data Current ratio 3.1 times Quick ratio 1.5 times Debt ratio 46.8% Times interest earned 10.6 times