Answered step by step

Verified Expert Solution

Question

1 Approved Answer

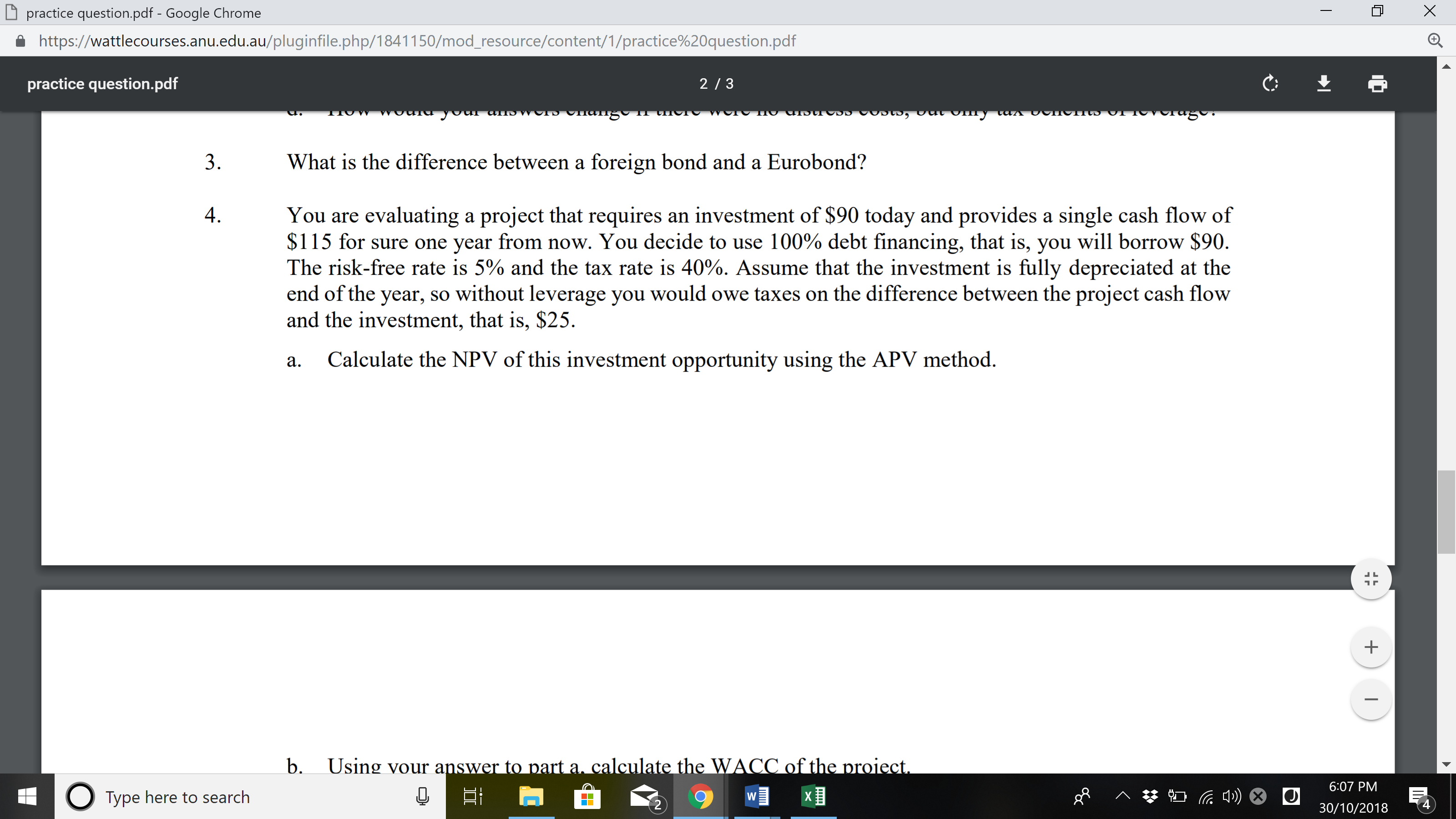

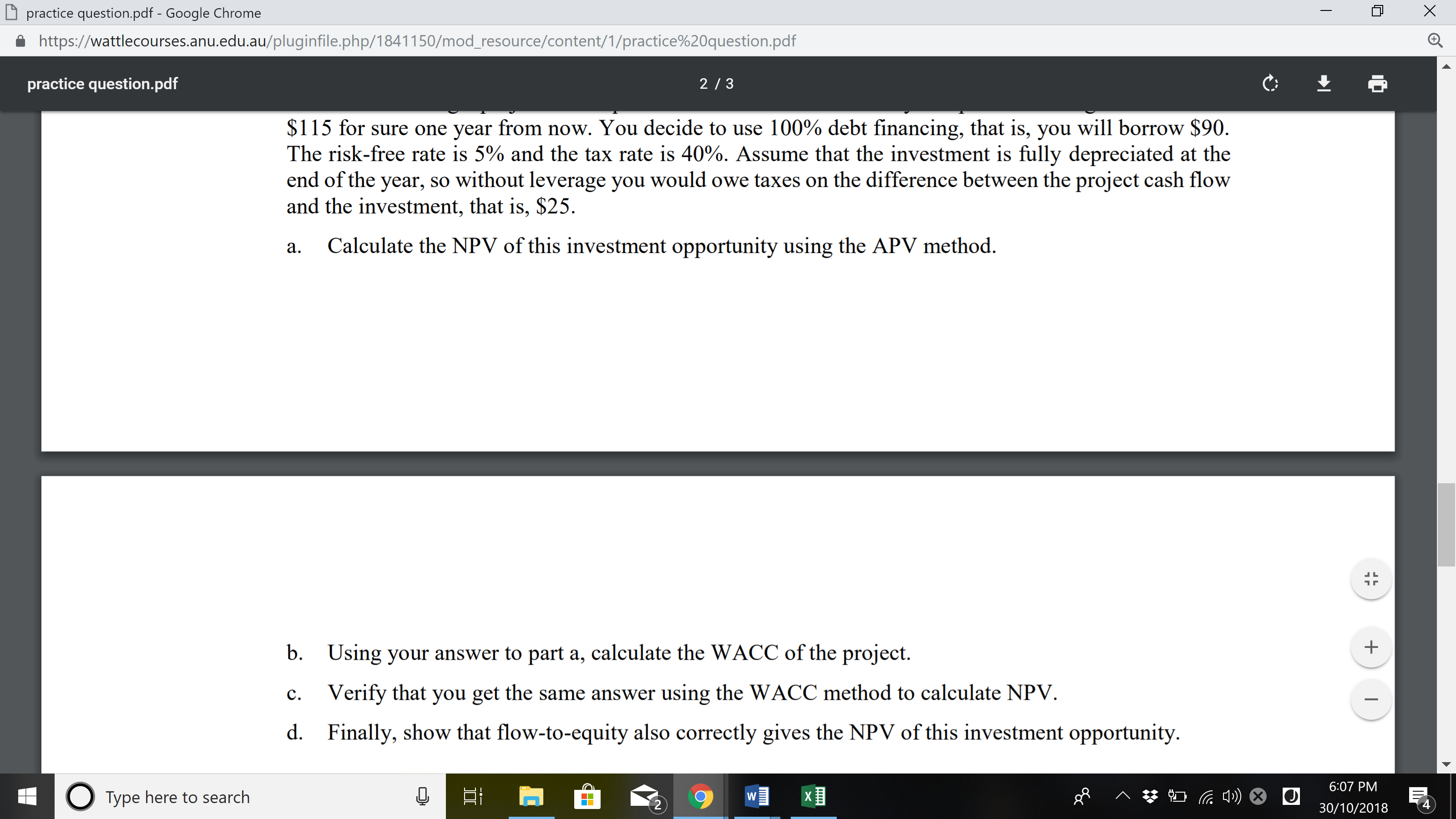

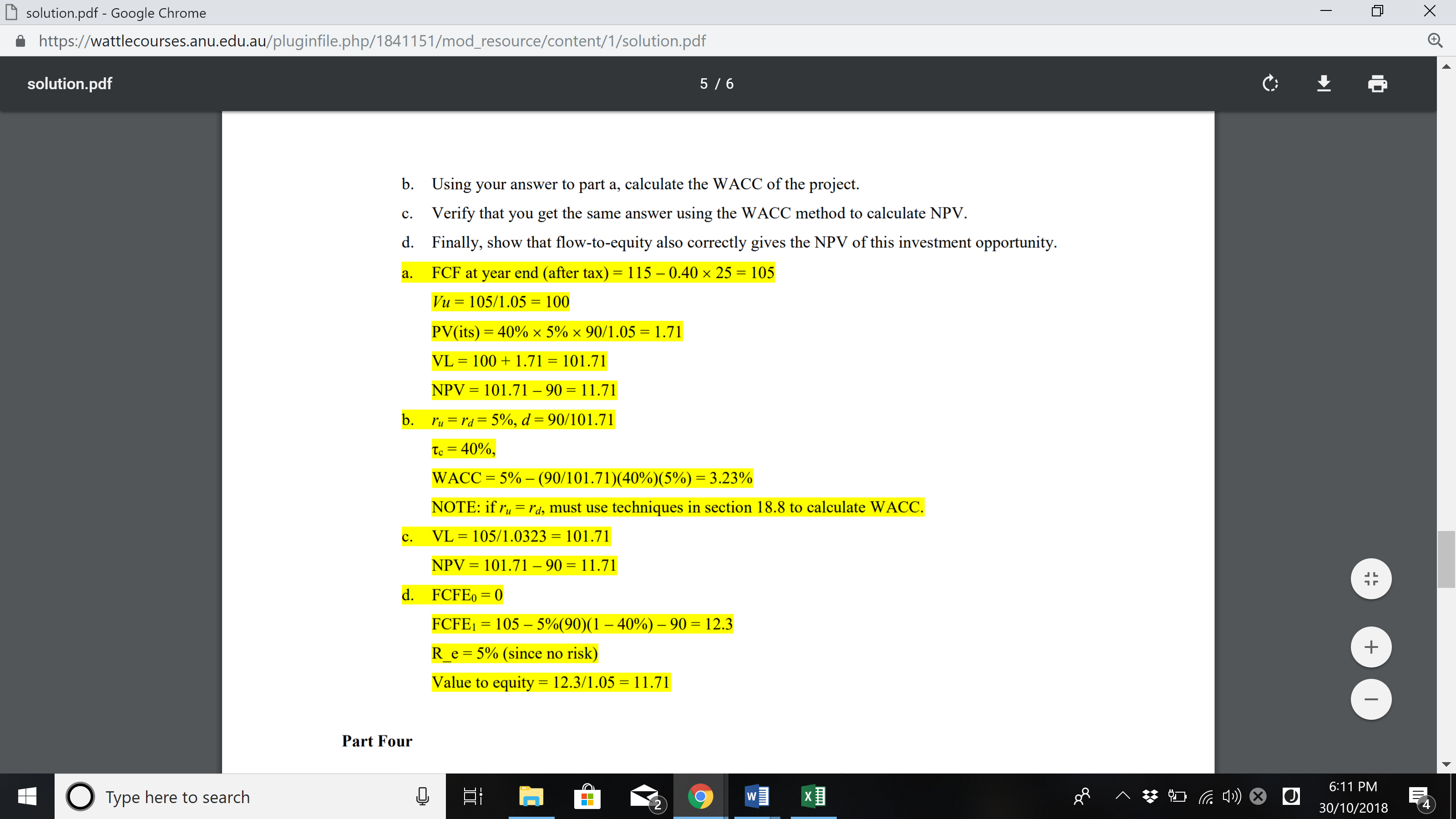

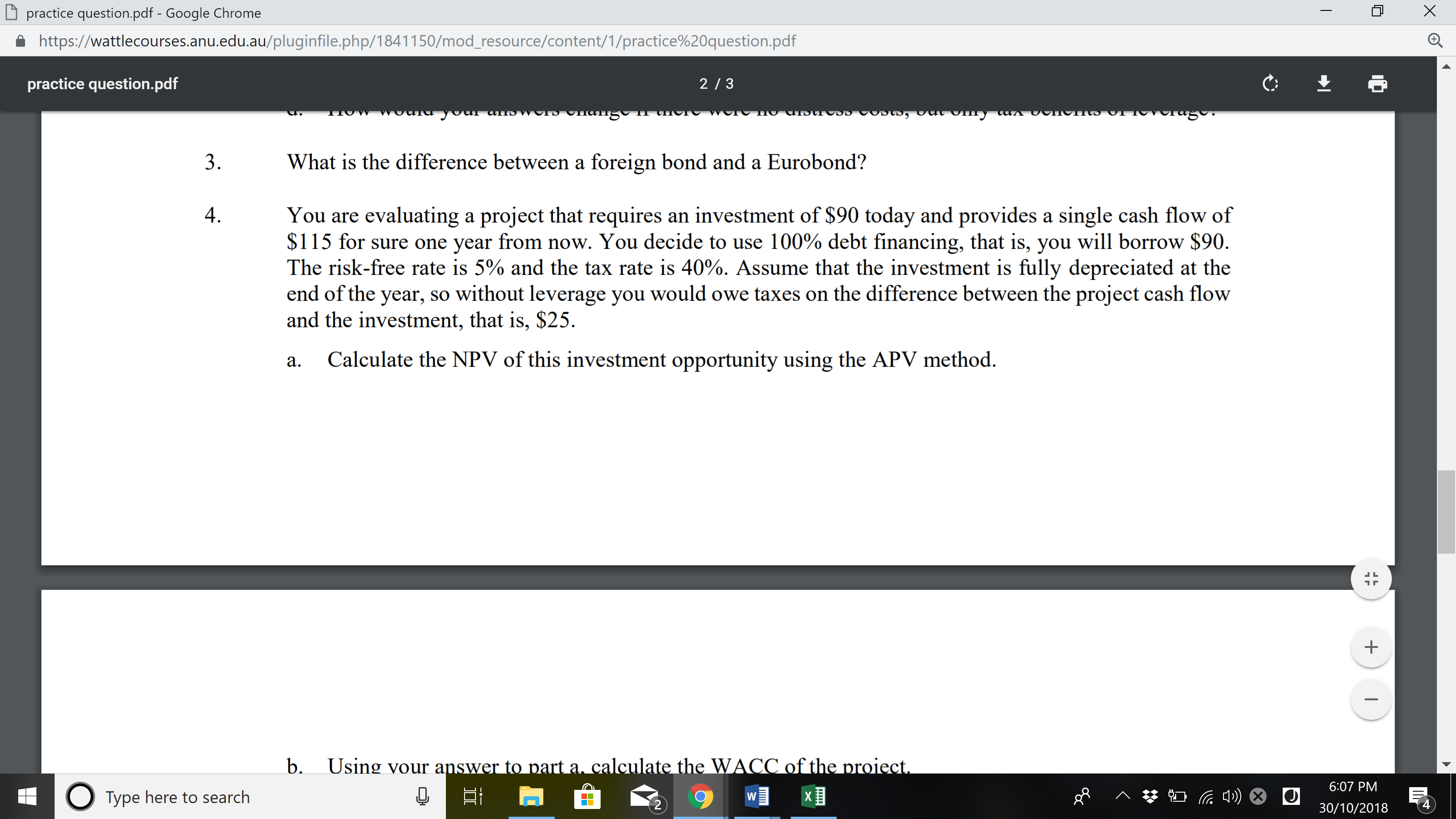

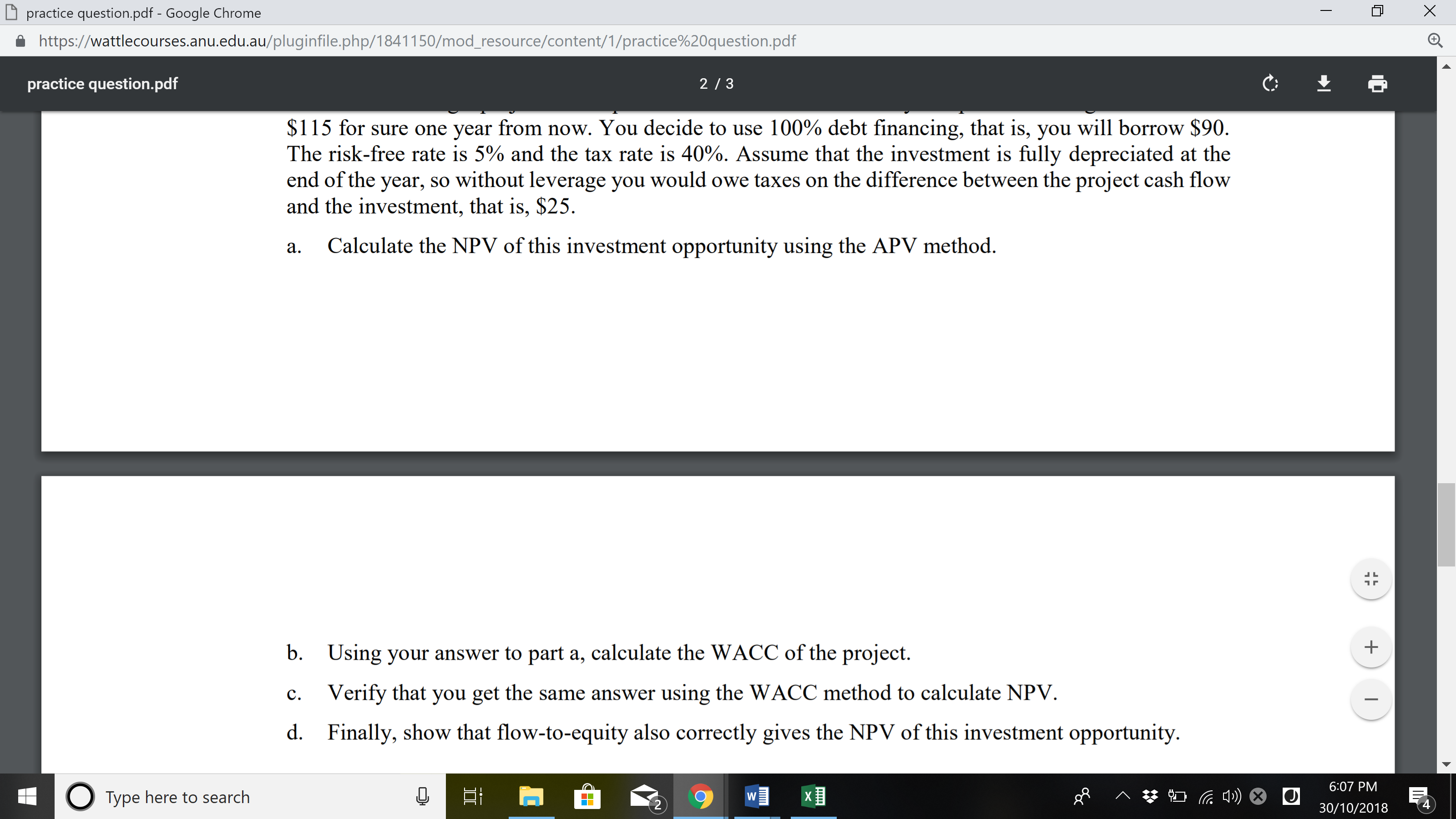

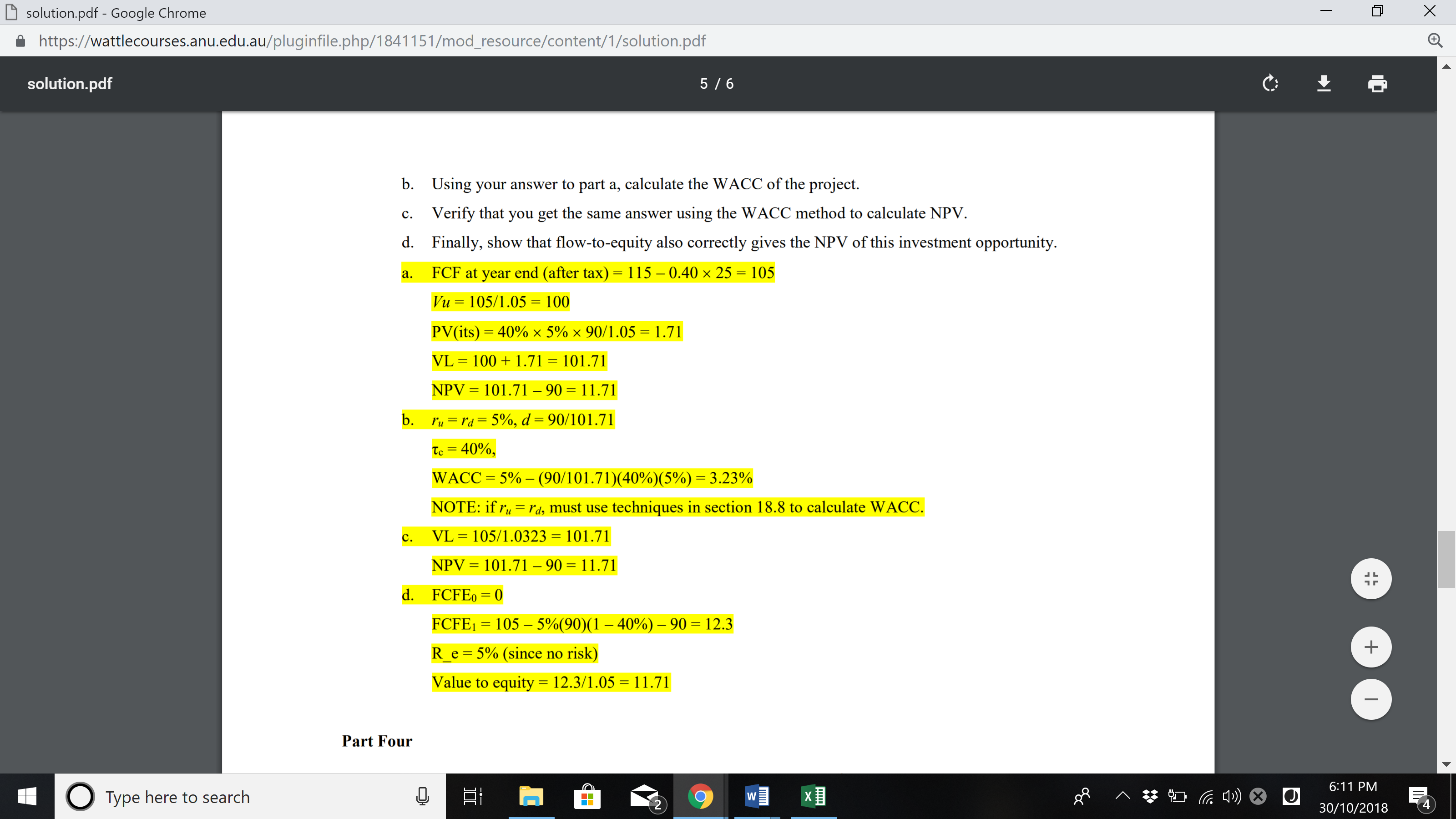

D practice questionpdf - Google Chrome 5 https://wattlecourses.anu.edu.au/p|uginfile.php/18411SO/modiresource/content/l/practice%20question,pdf practice questionlpdf E: 0 Type here to search 2/3 _. __ ' .........,... . ... .. .._.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Concepts and Applications

Authors: Stephen Foerster

1st edition

013293664X, 978-0132936644