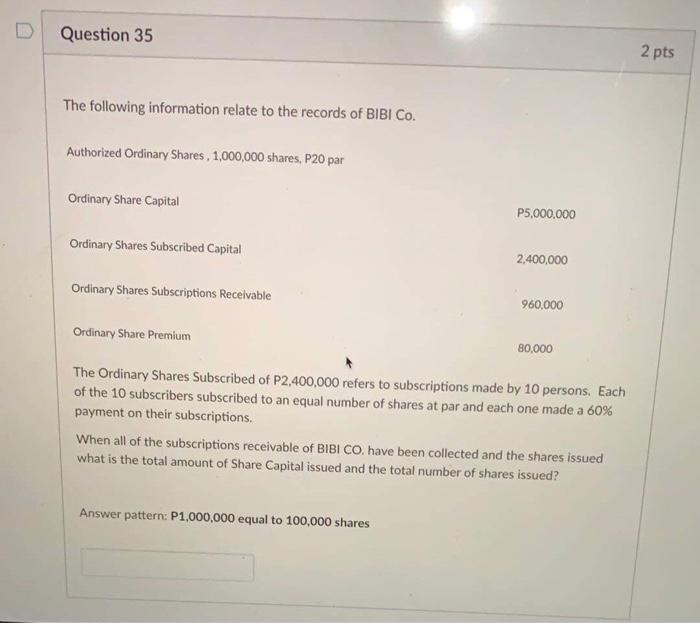

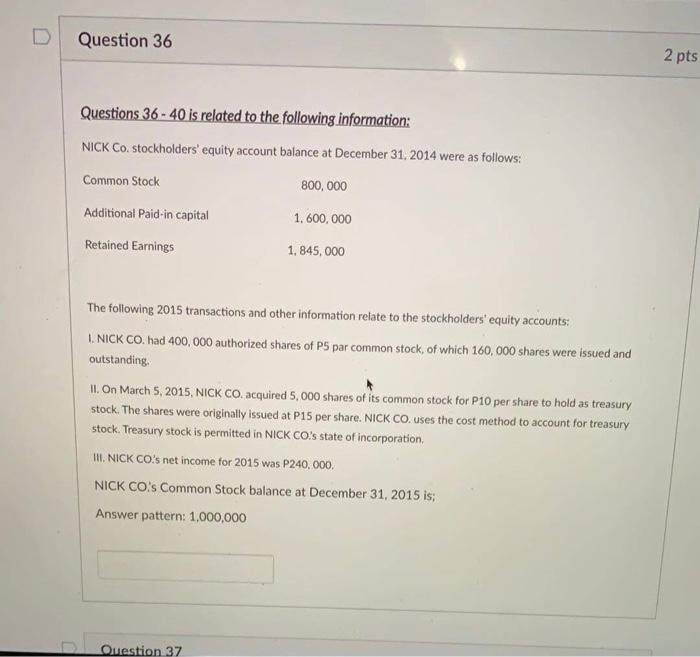

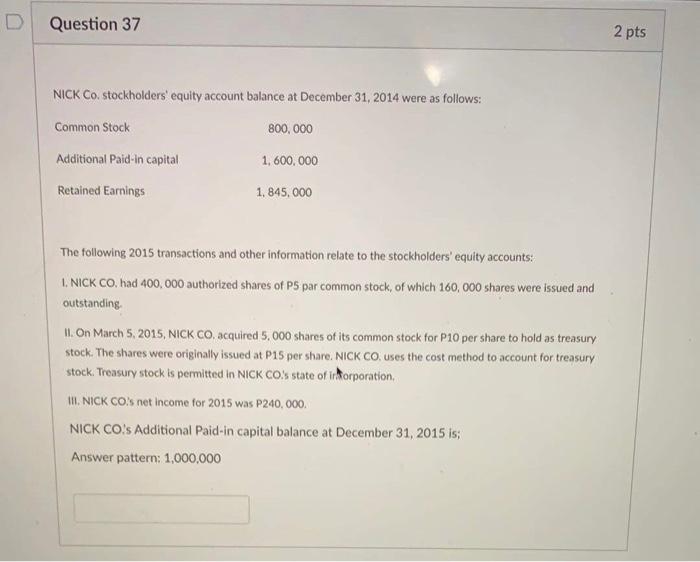

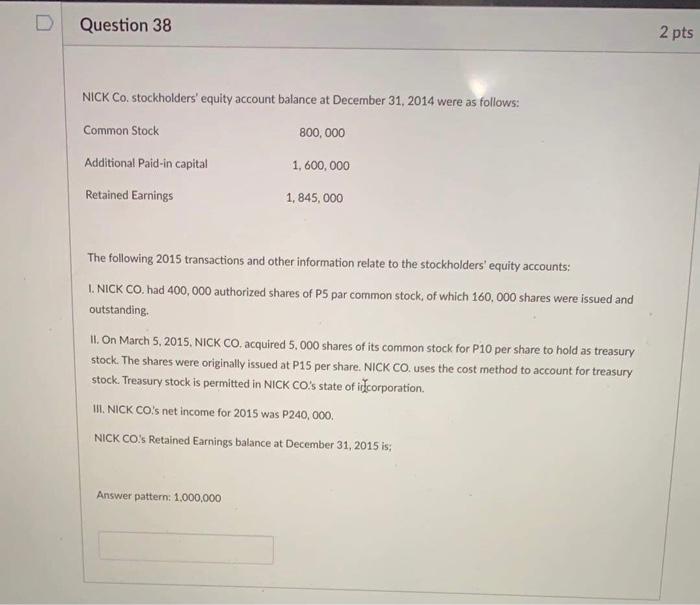

D Question 30 1 pts Preference shareholders can vote only upon 2/3 votes of BOD's. True False Question 31 2 pts On March 1, 2021, SEC authorized SHEIN Corp to issue 100,000 shares with par value of P20 per share. On March 3, 2021, SHEIN received subscriptions for 15,000 shares at par. SHEIN collected 25% on such subscriptions on March 4, 2021. On March 14, 2021, SHEIN received full payment on 5,000 shares originally subscribed and thereafter issued share certificates for 5,000 shares 1. Under the journal entry method of accounting for share capital transactions, how would SHEIN journalize the transaction on March 3, 2021? ODR-Subscription Receivable P300,000 CR -Subscribed Share Capital 300.000 DR Cash P300,000 CR-Share Capital P3000.000 DR Subscription Receivable P300,000 CR- Share Capital P300.000 DR - Unissued Shares P2,000,000 CR Authorized share capital P2.000.000 D Question 32 2 pts On March 1, 2021. SEC authorized SHEIN Corp to issue 100,000 shares with par value of P20 per share. On March 3, 2021, SHEIN received subscriptions for 15,000 shares at par. SHEIN collected 25% on such subscriptions on March 4, 2021. On March 14, 2021, SHEIN received full payment on 5,000 shares originally subscribed and thereafter issued share certificates for 5,000 shares. Under the memorandum entry method of accounting for share capital transactions, how would SHEIN journalize the issuance of shares on March 14, 2021? Dr-Subscribed Share Capital P100,000 CR- Share Capital P100,000 ODR-Subscribed Share Capital P65,000 CR- Share Capital P65,000 DR-Subscribed Share Capital P65,000 CR - Unissued Share Capital P65,000 o DR Subscribed Share Capital P100,000 CR-Unissued Share Capital P100,000 Question 33 2 pts The following information relate to the records of BIBI Co. Authorized Ordinary Shares, 1,000,000 shares, P20 par Ordinary Share Capital P5,000,000 Ordinary Shares Subscribed Capital 2,400,000 Ordinary Shares Subscriptions Receivable, 960,000 Ordinary Share Premium 80,000 The Ordinary Shares Subscribed of P2,400,000 refers to subscriptions made by 10 persons. Each of the 10 subscribers subscribed to an equal number of shares at par and each one made a 60% payment on their subscriptions. Assuming six of the ten subscribers of BIBI CO. who still have a balance payable on their subscriptions made full payment, how many shares of ordinary share capital will be issued? Answer Pattern: 10,000 shares Question 34 2 pts The following information relate to the records of BIBI CO. Authorized Ordinary Shares. 1.000,000 shares, P20 pat Ordinary Share Capital P5,000,000 Ordinary Shares Subscribed Capital 2,400,000 Ordinary Shares Subscriptions Receivable 960,000 Ordinary Share Premium 80,000 The Ordinary Shares Subscribed of P2,400,000 refers to subscriptions made by 10 persons. Each of the 10 subscribers subscribed to an equal number of shares at par and each one made a 60% payment on their subscriptions Assuming six of the ten subscribers of BIBI CO.who still have a balance payable on their subscriptions made full payment, How much is the balance of subscription Receivable after collecting full payment from six shareholders? Answer pattern: 100,000 Question 35 2 pts The following information relate to the records of BIBI Co. Authorized Ordinary Shares, 1,000,000 shares, P20 par Ordinary Share Capital P5,000,000 Ordinary Shares Subscribed Capital 2,400,000 Ordinary Shares Subscriptions Receivable 960,000 Ordinary Share Premium 80,000 The Ordinary Shares Subscribed of P2,400,000 refers to subscriptions made by 10 persons. Each of the 10 subscribers subscribed to an equal number of shares at par and each one made a 60% payment on their subscriptions. When all of the subscriptions receivable of BIBI CO, have been collected and the shares issued what is the total amount of Share Capital issued and the total number of shares issued? Answer pattern: P1,000,000 equal to 100,000 shares D Question 36 2 pts Questions 36-40 is related to the following information: NICK Co. stockholders' equity account balance at December 31, 2014 were as follows: Common Stock 800,000 1.600.000 Additional Paid-in capital Retained Earnings 1,845,000 The following 2015 transactions and other information relate to the stockholders' equity accounts: 1. NICK CO. had 400,000 authorized shares of P5 par common stock, of which 160,000 shares were issued and outstanding. II. on March 5, 2015, NICK CO. acquired 5,000 shares of its common stock for P10 per share to hold as treasury stock. The shares were originally issued at P15 per share. NICK CO. uses the cost method to account for treasury stock. Treasury stock is permitted in NICK CO's state of incorporation, III. NICK CO's net income for 2015 was P240,000. NICK CO.s Common Stock balance at December 31, 2015 is: Answer pattern: 1,000,000 Question 37 D Question 37 2 pts NICK Co stockholders' equity account balance at December 31, 2014 were as follows: Common Stock 800,000 Additional Paid-in capital 1,600,000 Retained Earnings 1,845,000 The following 2015 transactions and other information relate to the stockholders' equity accounts: 1. NICK CO. had 400,000 authorized shares of P5 par common stock, of which 160,000 shares were issued and outstanding II. on March 5, 2015, NICK CO acquired 5,000 shares of its common stock for P10 per share to hold as treasury stock. The shares were originally issued at P15 per share. NICK CO, uses the cost method to account for treasury stock. Treasury stock is permitted in NICK CO.S state of orporation, III. NICK CO.S net income for 2015 was P240,000. NICK CO's Additional Paid-in capital balance at December 31, 2015 is; Answer pattern: 1,000,000 D Question 38 2 pts NICK Co. stockholders' equity account balance at December 31, 2014 were as follows: Common Stock 800,000 1,600,000 Additional Paid-in capital Retained Earnings 1,845,000 The following 2015 transactions and other information relate to the stockholders' equity accounts: 1. NICK CO. had 400,000 authorized shares of P5 par common stock, of which 160,000 shares were issued and outstanding. 11. On March 5, 2015, NICK CO. acquired 5,000 shares of its common stock for P10 per share to hold as treasury stock. The shares were originally issued at P15 per share. NICK CO. uses the cost method to account for treasury stock. Treasury stock is permitted in NICK CO:s state of is corporation. III. NICK CO's net income for 2015 was P240,000. NICK COs Retained Earnings balance at December 31, 2015 is: Answer pattern: 1.000.000 Question 39 2 NICK Co. stockholders' equity account balance at December 31, 2014 were as follows: Common Stock 800,000 Additional Paid-in capital 1,600,000 Retained Earnings 1,845,000 The following 2015 transactions and other information relate to the stockholders' equity accounts: 1. NICK CO. had 400,000 authorized shares of P5 par common stock, of which 160,000 shares were issued and outstanding. II. On March 5, 2015, NICK CO. acquired 5,000 shares of its common stock for P10 per share to hold as treasury stock. The shares were originally issued at P15 per share. NICK CO. uses the cost method to account for treasury stock. Treasury stock is permitted in NICK CO's state of inforporation. III. NICK CO's net income for 2015 was P240,000. NICK CO's Treasury Stock balance at December 31, 2015 is; Answer pattern: 1,000,000 Question 40 2 pts NICK Co. stockholders' equity account balance at December 31, 2014 were as follows: Common Stock 800,000 Additional Paid-in capital 1,600,000 Retained Earnings 1,845,000 The following 2015 transactions and other information relate to the stockholders' equity accounts: 1. NICK CO. had 400,000 authorized shares of P5 par common stock, of which 160,000 shares were issued and outstanding. 11. On March 5, 2015, NICK CO. acquired 5.000 shares of its common stock for P10 per share to hold as treasury stock. The shares were originally issued at P15 per share. JNICK CO. uses the cost method to account for treasury stock. Treasury stock is permitted in NICK CO's state of incorporation II. NICK CO's net income for 2015 was P240,000 NICK CO.s Stockholders' Equity balance at December 31, 2015 is; Answer pattern: 1,000,000