Answered step by step

Verified Expert Solution

Question

1 Approved Answer

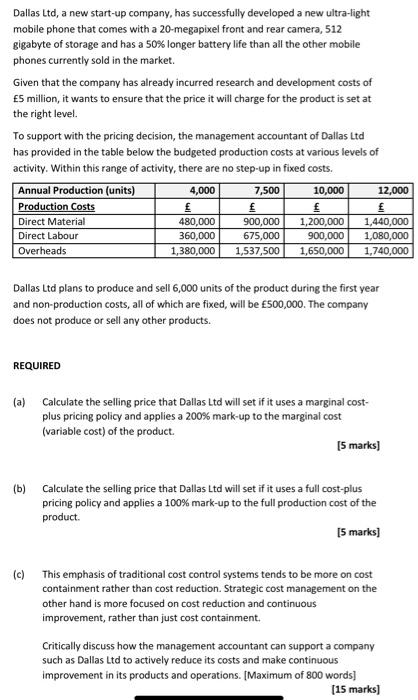

Dallas Ltd, a new start-up company, has successfully developed a new ultra-light mobile phone that comes with a 20-megapixel front and rear camera, 512 gigabyte

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

IATF 16949 2016 Plus ISO 9001 2015 Audit Guide And Checklist With ISO 9001 Customer Specific Core Tools And CQI Requirments

Authors: Patrick Ambrose, Systemsthinking .works

2nd Edition

154703355X, 978-1547033553