Question

Darryl is the sole proprietor of a motorcycle shop. During the present year, Darryl had $32,000 of adjusted gross income before considering the tax effect

Darryl is the sole proprietor of a motorcycle shop. During the present year, Darryl had $32,000 of adjusted gross income before considering the tax effect of the following transactions. Darryl has no remaining nonrecaptured 1231 losses from the prior five tax years.

a. Land adjacent to the store was purchased 3-years ago for an anticipated store expansion. It cost $14,000 and was sold this year for $35,000.

b. Obsolete 5-year-old motorcycle repair equipment was sold for $12,000 during the year. It was fully depreciated. The equipment cost $65,000.

c. Darryl developed and patented a new synthetic oil called Super Z. Darryl had not reduced the patent to practice. He sold all his rights in the patent for $75,000 to Harley Davidson. Darryl had not amortized the $12,000 cost of obtaining the patent. He held the patent for more than a year, but less than five years.

d. A 3-year-old delivery truck with an adjusted basis of $6,000 was sold for $17,000. It had cost $10,000.

e. One of the motorcycle repair machines caught on fire and was completely destroyed. It had an adjusted basis of $17,000. The insurance recovery was $24,000. The machine was obsolete, had been purchased several years ago, and was not replaced.

f. Darryl bought an electronic cash register for $3,000 early in the year. It was not suitable for his business. Darryl sold it for $2,500 four months after it was purchased.

g. Darryls 2-year-old personal car was rear-ended by a truck. The auto was completely demolished. The adjusted basis of the car was $15,000. Darryl did not have any insurance for collision damage. The car was worth $12,000 before the crash.

h. Darryl sold for $300,000 an apartment building he had owned for 15 years. Total depreciation on the building was $363,189. The adjusted basis was $125,000.

i. Darryl sold Memorial Grady stock (purchased in January of last year for $16,000) for $39,000 in December of this year.

j. Darryl sold Del Amo Foods stock (purchased in September of this year for $27,000) for $21,000 in December of this year.

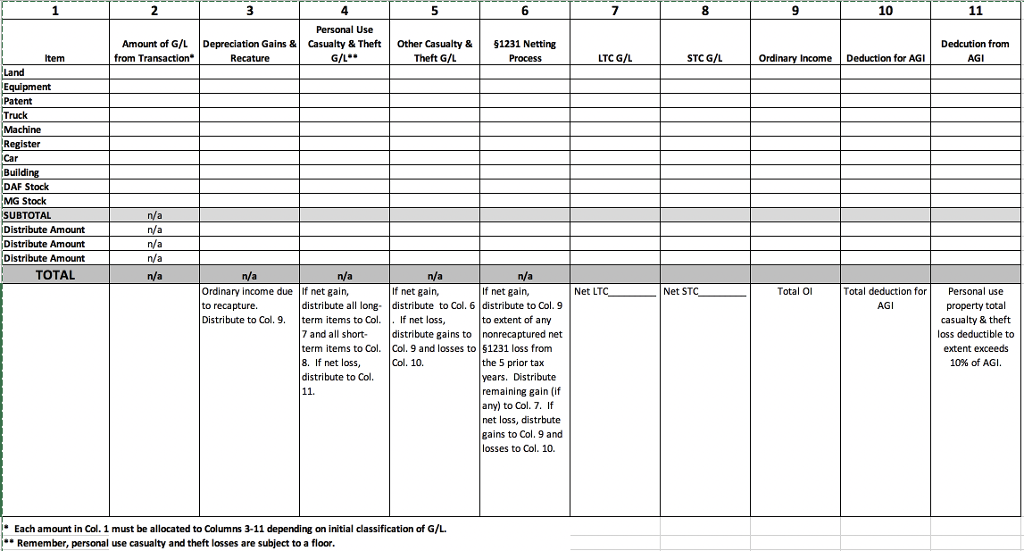

Using the Worksheet provided:

1. Analyze each transaction above to determine the amount of gain or loss from that transaction. Identify such amount in Column 1.

2. Determine the initial classification(s) of each gain and loss (Exhibits 6 and 7 can assist) and place the gains/losses in the correct columns (Columns 3-11) on the Worksheet.

3, After completing the Worksheet, determine Darryls AGI and deductions from AGI.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Operations Management

Authors: David Loader

2nd Edition

0470026545, 978-0470026540