Question

DATA FROM: https://drive.google.com/file/d/1jGFcz6wA93o1XjxBwpyUswNJS52872mR/view?usp=sharing USE GMAIL TO ACCESS LINK Question 3 Assessing control risk in the purchase and cash disbursement cycle a. Identify five control weaknesses

DATA FROM: https://drive.google.com/file/d/1jGFcz6wA93o1XjxBwpyUswNJS52872mR/view?usp=sharing

USE GMAIL TO ACCESS LINK

Question 3 Assessing control risk in the purchase and cash disbursement cycle

a. Identify five control weaknesses in the purchase system.

b. Explain how each control weakness may affect the financial statements (i.e. which accounts and assertions are at risk)

c. Identify the audit procedures to test the account(s) and assertion(s) that are at risk.

a. Identify six control strengths in the inventory system

b. Explain why each control is a strength (i.e. which accounts and assertions does it strengthen).

c. For each control strength, identify audit procedures to test the effectiveness of control.

Question 4: Substantive Procedures and Audit Documentation

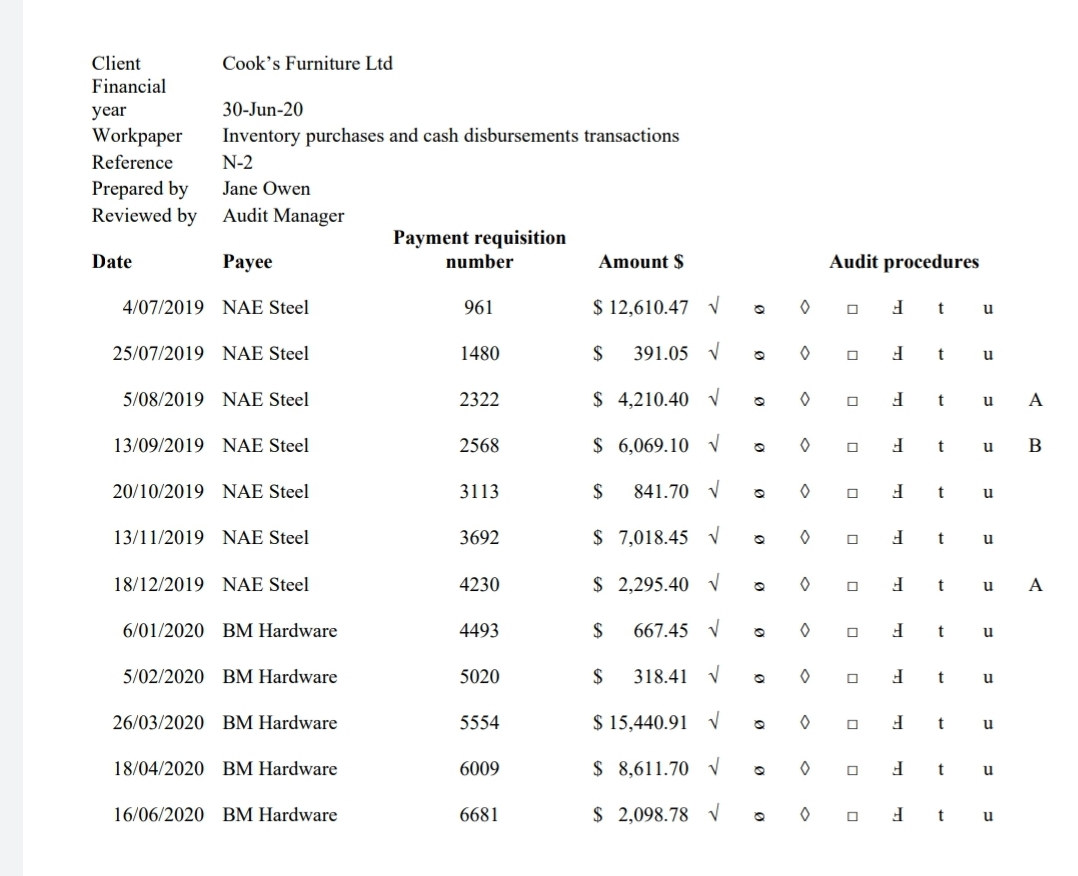

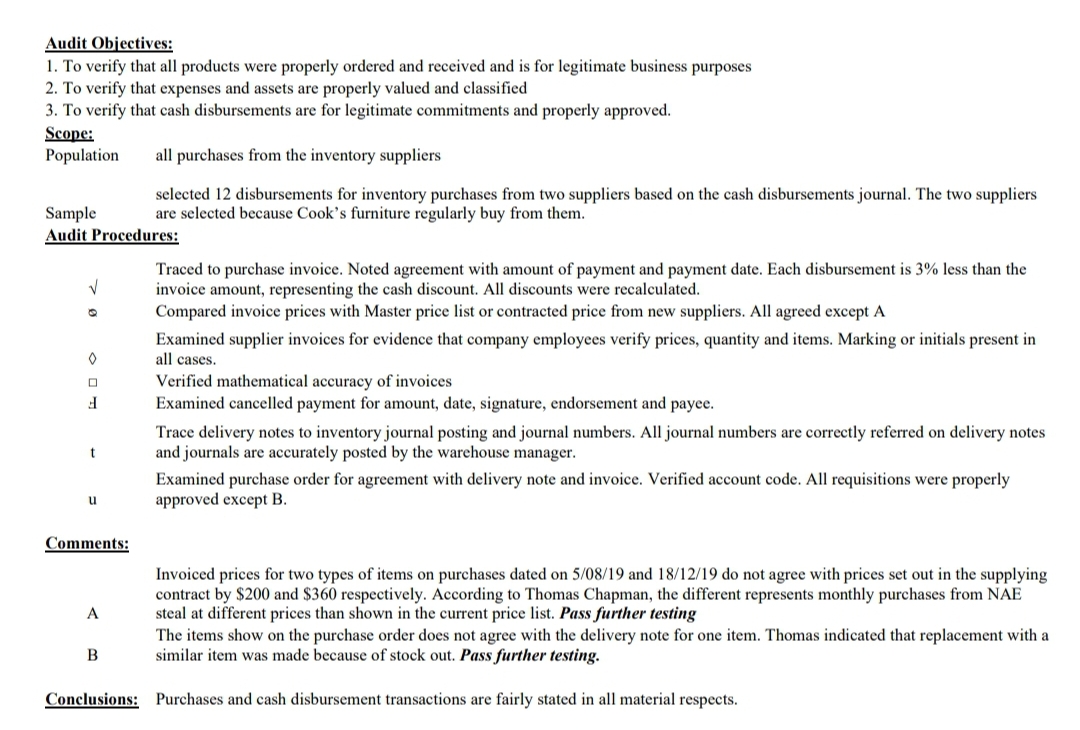

After the end of the financial year, Jane Owen performed transaction tests of the inventory purchases and cash disbursement. She summarised the audit procedures she performed in the following workpaper (reference N-2). To ensure audit quality, BDC has a review policy which helps to ensure that each audit document provides a clear and complete indication of the procedures that were performed and that adequate evidence has been collected. For this audit, you must review and approve all audit workpapers. If you find any unclarity or issues in a workpaper, the workpaper is returned to the appropriate staff auditor for necessary and appropriate revision.

REQUIRED:

Review the audit work papers below. Prepare Jane a list of the concerns that are present in her work papers. For each point raised, give explanations why the documentation is not appropriate.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Management Accounting A User Perspective

Authors: Michael L Werner, Kumen H Jones

2nd Edition

0130327506, 9780130327505