Answered step by step

Verified Expert Solution

Question

1 Approved Answer

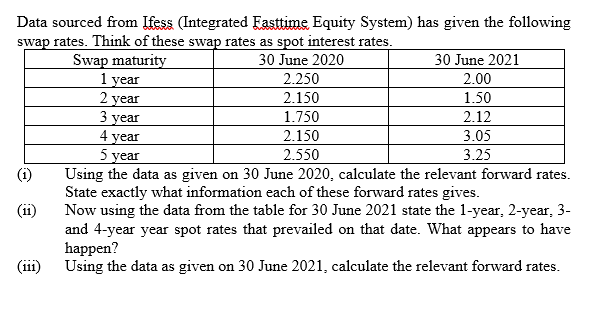

Data sourced from Ifess (Integrated Fasttime Equity System) has given the following swap rates. Think of these swap rates as spot interest rates. Swap

Data sourced from Ifess (Integrated Fasttime Equity System) has given the following swap rates. Think of these swap rates as spot interest rates. Swap maturity 1 year 2 year 3 year 4 year 5 year 30 June 2020 2.250 2.150 1.750 2.150 2.550 30 June 2021 2.00 1.50 2.12 3.05 3.25 (11) (111) Using the data as given on 30 June 2020, calculate the relevant forward rates. State exactly what information each of these forward rates gives. Now using the data from the table for 30 June 2021 state the 1-year, 2-year, 3- and 4-year year spot rates that prevailed on that date. What appears to have happen? Using the data as given on 30 June 2021, calculate the relevant forward rates.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Practicing Statistics Guided Investigations For The Second Course

Authors: Shonda Kuiper, Jeff Sklar

1st Edition

321586018, 978-0321586018