Question: Dave asked Means to present her finding to the larger community of employees at the firm. Several reprintatives the manufacturing departments were present, as well

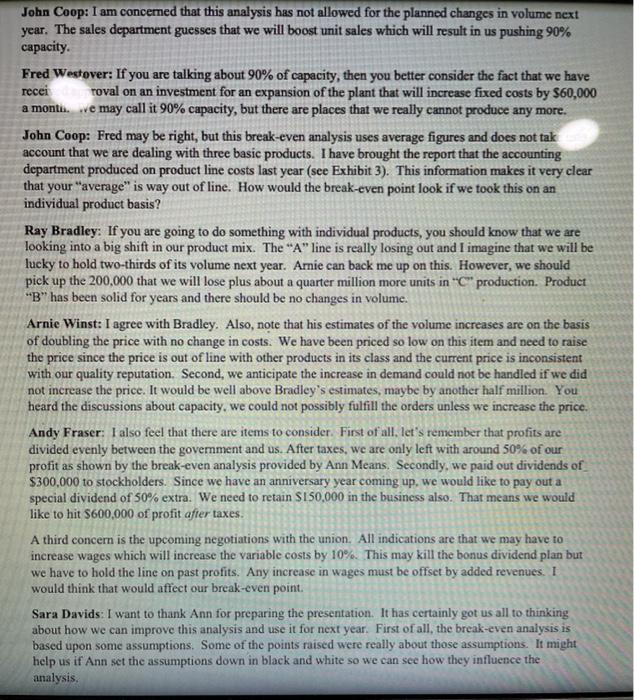

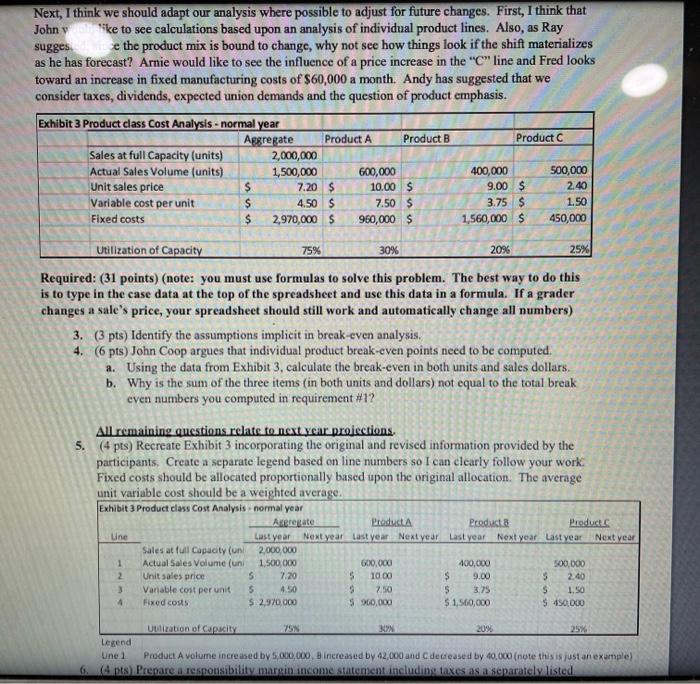

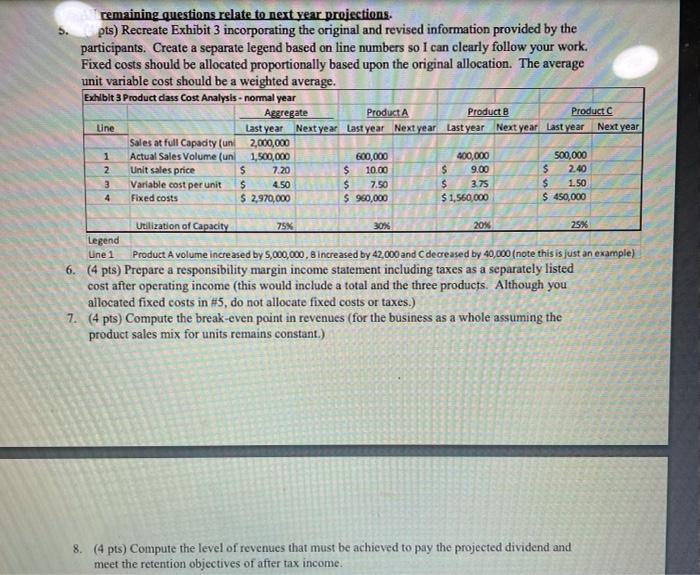

Dave asked Means to present her finding to the larger community of employees at the firm. Several reprintatives the manufacturing departments were present, as well as the metal sales manage to tant sales managers, the purchasing office and we people from production in Follow is chart of these senting tahlar Matripants) Staff Accountant Controller Product Control Manfacturing Assistant Sales Manager General Sales Manager Administrative Assistant to the President The follow the Alam concerned that this analysis has not allowed for the planned changes in volume next Star The sales departments that we will boost titles which will result in phi 90% you are talking about 90% of capacity, then you better comider the fact that we have received approval ansvestment for an expansion of the plant that will increase fixed costs try $40,000 We may call i capacity, but there are places that we really cannot produce any more. y be right. But this becak-even analysis uses average figures and does not take into cott we are dealing with the basic products. Thave brought the report that the accounting department produced en product line costs last year see Exhibit 3 This information makes a very clear that you werage" is way out of line. How would the beak-even prick if we took this can Latinal product basis? you are paring to do something with individuel products, you should know that we are Woking into a hug shift in our product mix. The line is really losing out and I imagine that we will be fucky to hold two-think of its volume next you hack me up on this. However, we should pick up the 200.000 that we will lose plus about a quarter milties more units in production Product "Esolid for years and there should be so changes in volume Ale note that his estimates of the volume increases are on the basis of oubling the price with no change in costs. We have been priced so low on this item and need to make the price since the price is out of line with other products in its class and the current prices inconsistent with our quality reputation. Second, we anticipate the increase in demand could not be lundied if we did not increase the price. It would be well above estimates, maybe by another half million. You Sdraic about capacity, we could not posibly fulfill the orders unless we increase the price I also feel that there are este consider First of all, let's member that profits are divided evenly between the povernment and us. After taxes we cely left with around 50% off peolitas shown by the beak-even analysis provided by cody, we paid ou dividends of $300,000 cholen. Since we have an anniversary year coming up, we would like to pay out pecial dividend 50lestra We need to retain S150,000 in the business. That means we would like to hit 600.000 or profit after taxe Athind concem is the upcoming reportations with the union. All indications are that we may have to increase wages which will increase the variable costs by 10%. This may kill the bonus dividend plan bu we have to hold the line on post profits. Any increase in wapes must be offset by added revenues ile old affect our brouk-even point ant to thank for preparing the presentation. It has certainly got us all to thinking about how we can improve the analysis and use it for next year First of all, the break-eventysis is based upon some assumption Some of the points and were really about those assumption it might help withe assumptions down in black md where so we can see how they influence the Next, I think we should adapt our analysis where possible to adjust for future changes. First, I think that would like to see calculations based upon an analysis of individual product lines. Also, as suggested, since the product mix is bound to change, why not see how things look if the shift materializes as he has forecast?kould like to see the influence of a price increase in the "C" line and looks toward an increase in fixed manufacturing costs of $60,000 a month as suggested that we consider taxes, dividends, expected union demands and the question of product emphasis Exhibit 3 Product class Cost Analysis - normal year Arererate Product A Product Product Sales at full Capacity (units) 2.000.000 Actual Sales Volume (units) 1.500.000 600,000 400,000 500.000 Unit sales price $ 7205 10.00 $ 9.00 $ 2.40 Variable cost per unit $ 4.50 7.505 3.75$ 1.50 Fixed costs $ 2.970,000 $ 960,000 $ 1.560,000 $ 450,000 Utilization of Capacity 30% 20% Required: (31 points) (note: you must use formulas to solve this problem. The best way to do this is to type in the case data at the top of the spreadsheet and use this data in a formula. If a grader changes a sale's price, your spreadsheet should still work and automatically change all numbers) 3. (3 pts) Identify the assumptions implicit in break-even analysis 4. (6 pts gorgues that individual product break-even points need to be computed a. Using the data from Exhibit 3. calculate the break-even in both units and sales dollars 1. Why is the sum of the three items (in both units and dollars) not equal to the total becak even numbers you computed in requirement #l? All remaining questions relate to next year projections. 5. (4 pts) Recreate Exhibit 3 incorporating the original and revised information provided by the participants. Create a separate legend based on line numbers so I can clearly follow your work Fixed costs should be allocated proportionally based upon the original allocation. The average unit variable cost should be a weighted average Exhibit Product cats Cost Analysis formal year Aggregate Product Protect Last year Next year last year Next year antytar Next year. Last year Next year Sales atful Capacity on 2.000.000 Actual Sales Volume fun 1.500.000 500.000 100.000 500.000 2 Unitsale price 720 5 3000 5 200 5 2.40 3 Variable cost per 4.50 7.50 375 4 Fixed costs $ 2.970,000 $ 60,000 $ 0.00 550.000 Union of Cagay 79 Legend Line 1 Product A volume increased by 5.000.000, increased by 12.000 and decreased by 40 000 note this is just an example 6. (4 pts) Prepare a responsibility margin income statement including taxes as a separately listed cost after operating income (this would include a total and the three products. Although you allocated fixed costs in 5. do not allocate fixed costs or taxes.) 7. (4 pts) Compute the becak-even point in revenues (for the business as a whole assuming the product sales mix for units remains constant.) $ $ $ 150 8.4pts Compute the level of revenues that must be achieved to pay the projected dividend and meet the retention objectives of after tax income Dave asked Means to present her finding to the larger community of employees at the firm. Several reprintatives the manufacturing departments were present, as well as the metal sales manage to tant sales managers, the purchasing office and we people from production in Follow is chart of these senting tahlar Matripants) Staff Accountant Controller Product Control Manfacturing Assistant Sales Manager General Sales Manager Administrative Assistant to the President The follow the Alam concerned that this analysis has not allowed for the planned changes in volume next Star The sales departments that we will boost titles which will result in phi 90% you are talking about 90% of capacity, then you better comider the fact that we have received approval ansvestment for an expansion of the plant that will increase fixed costs try $40,000 We may call i capacity, but there are places that we really cannot produce any more. y be right. But this becak-even analysis uses average figures and does not take into cott we are dealing with the basic products. Thave brought the report that the accounting department produced en product line costs last year see Exhibit 3 This information makes a very clear that you werage" is way out of line. How would the beak-even prick if we took this can Latinal product basis? you are paring to do something with individuel products, you should know that we are Woking into a hug shift in our product mix. The line is really losing out and I imagine that we will be fucky to hold two-think of its volume next you hack me up on this. However, we should pick up the 200.000 that we will lose plus about a quarter milties more units in production Product "Esolid for years and there should be so changes in volume Ale note that his estimates of the volume increases are on the basis of oubling the price with no change in costs. We have been priced so low on this item and need to make the price since the price is out of line with other products in its class and the current prices inconsistent with our quality reputation. Second, we anticipate the increase in demand could not be lundied if we did not increase the price. It would be well above estimates, maybe by another half million. You Sdraic about capacity, we could not posibly fulfill the orders unless we increase the price I also feel that there are este consider First of all, let's member that profits are divided evenly between the povernment and us. After taxes we cely left with around 50% off peolitas shown by the beak-even analysis provided by cody, we paid ou dividends of $300,000 cholen. Since we have an anniversary year coming up, we would like to pay out pecial dividend 50lestra We need to retain S150,000 in the business. That means we would like to hit 600.000 or profit after taxe Athind concem is the upcoming reportations with the union. All indications are that we may have to increase wages which will increase the variable costs by 10%. This may kill the bonus dividend plan bu we have to hold the line on post profits. Any increase in wapes must be offset by added revenues ile old affect our brouk-even point ant to thank for preparing the presentation. It has certainly got us all to thinking about how we can improve the analysis and use it for next year First of all, the break-eventysis is based upon some assumption Some of the points and were really about those assumption it might help withe assumptions down in black md where so we can see how they influence the Next, I think we should adapt our analysis where possible to adjust for future changes. First, I think that would like to see calculations based upon an analysis of individual product lines. Also, as suggested, since the product mix is bound to change, why not see how things look if the shift materializes as he has forecast?kould like to see the influence of a price increase in the "C" line and looks toward an increase in fixed manufacturing costs of $60,000 a month as suggested that we consider taxes, dividends, expected union demands and the question of product emphasis Exhibit 3 Product class Cost Analysis - normal year Arererate Product A Product Product Sales at full Capacity (units) 2.000.000 Actual Sales Volume (units) 1.500.000 600,000 400,000 500.000 Unit sales price $ 7205 10.00 $ 9.00 $ 2.40 Variable cost per unit $ 4.50 7.505 3.75$ 1.50 Fixed costs $ 2.970,000 $ 960,000 $ 1.560,000 $ 450,000 Utilization of Capacity 30% 20% Required: (31 points) (note: you must use formulas to solve this problem. The best way to do this is to type in the case data at the top of the spreadsheet and use this data in a formula. If a grader changes a sale's price, your spreadsheet should still work and automatically change all numbers) 3. (3 pts) Identify the assumptions implicit in break-even analysis 4. (6 pts gorgues that individual product break-even points need to be computed a. Using the data from Exhibit 3. calculate the break-even in both units and sales dollars 1. Why is the sum of the three items (in both units and dollars) not equal to the total becak even numbers you computed in requirement #l? All remaining questions relate to next year projections. 5. (4 pts) Recreate Exhibit 3 incorporating the original and revised information provided by the participants. Create a separate legend based on line numbers so I can clearly follow your work Fixed costs should be allocated proportionally based upon the original allocation. The average unit variable cost should be a weighted average Exhibit Product cats Cost Analysis formal year Aggregate Product Protect Last year Next year last year Next year antytar Next year. Last year Next year Sales atful Capacity on 2.000.000 Actual Sales Volume fun 1.500.000 500.000 100.000 500.000 2 Unitsale price 720 5 3000 5 200 5 2.40 3 Variable cost per 4.50 7.50 375 4 Fixed costs $ 2.970,000 $ 60,000 $ 0.00 550.000 Union of Cagay 79 Legend Line 1 Product A volume increased by 5.000.000, increased by 12.000 and decreased by 40 000 note this is just an example 6. (4 pts) Prepare a responsibility margin income statement including taxes as a separately listed cost after operating income (this would include a total and the three products. Although you allocated fixed costs in 5. do not allocate fixed costs or taxes.) 7. (4 pts) Compute the becak-even point in revenues (for the business as a whole assuming the product sales mix for units remains constant.) $ $ $ 150 8.4pts Compute the level of revenues that must be achieved to pay the projected dividend and meet the retention objectives of after tax income John Coop: I am concerned that this analysis has not allowed for the planned changes in volume next year. The sales department guesses that we will boost unit sales which will result in us pushing 90% capacity. Fred Westover: If you are talking about 90% of capacity, then you better consider the fact that we have recei roval on an investment for an expansion of the plant that will increase fixed costs by $60,000 a monta ve may call it 90% capacity, but there are places that we really cannot produce any more. John Coop: Fred may be right, but this break-even analysis uses average figures and does not tak account that we are dealing with three basic products. I have brought the report that the accounting department produced on product line costs last year (see Exhibit 3). This information makes it very clear that your "average" is way out of line. How would the break-even point look if we took this on an individual product basis? Ray Bradley: If you are going to do something with individual products, you should know that we are looking into a big shift in our product mix. The "A" line is really losing out and I imagine that we will be lucky to hold two-thirds of its volume next year. Arnie can back me up on this. However, we should pick up the 200,000 that we will lose plus about a quarter million more units in "C"production. Product "B" has been solid for years and there should be no changes in volume. Arnie Winst: I agree with Bradley. Also, note that his estimates of the volume increases are on the basis of doubling the price with no change in costs. We have been priced so low on this item and need to raise the price since the price is out of line with other products in its class and the current price is inconsistent with our quality reputation. Second, we anticipate the increase in demand could not be handled if we did not increase the price. It would be well above Bradley's estimates, maybe by another half million. You heard the discussions about capacity, we could not possibly fulfill the orders unless we increase the price. Andy Fraser: I also feel that there are items to consider. First of all, let's remember that profits are divided evenly between the goverment and us. After taxes, we are only left with around 50% of our profit as shown by the break-even analysis provided by Ann Means. Secondly, we paid out dividends of $300,000 to stockholders. Since we have an anniversary year coming up, we would like to pay out a special dividend of 50% extra. We need to retain S150,000 in the business also. That means we would like to hit $600,000 of profit after taxes. A third concern is the upcoming negotiations with the union. All indications are that we may have to increase wages which will increase the variable costs by 10%. This may kill the bonus dividend plan but we have to hold the line on past profits. Any increase in wages must be offset by added revenues. 1 would think that would affect our break-even point Sara Davids: I want to thank Ann for preparing the presentation. It has certainly got us all to thinking about how we can improve this analysis and use it for next year. First of all, the break-even analysis is based upon some assumptions. Some of the points raised were really about those assumptions. It might help us if Ann set the assumptions down in black and white so we can see how they influence the analysis Next, I think we should adapt our analysis where possible to adjust for future changes. First, I think that Johny like to see calculations based upon an analysis of individual product lines. Also, as Ray sugges e the product mix is bound to change, why not see how things look if the shift materializes as he has forecast? Arnie would like to see the influence of a price increase in the "C" line and Fred looks toward an increase in fixed manufacturing costs of $60,000 a month. Andy has suggested that we consider taxes, dividends, expected union demands and the question of product emphasis. Exhibit 3 Product class Cost Analysis - normal year Aggregate Product A Product B Product C Sales at full Capacity (units) 2,000,000 Actual Sales Volume (units) 1,500,000 600,000 400,000 500,000 Unit sales price $ 7.20 $ 10.00 $ 9.00 $ 2.40 Variable cost per unit $ 4.50 $ 7.50 $ 3.75 $ 1.50 Fixed costs $ 2,970,000 $ 960,000 $ 1,560,000 $ 450,000 75% 30% 209 25% Utilization of Capacity Required: (31 points) (note: you must use formulas to solve this problem. The best way to do this is to type in the case data at the top of the spreadsheet and use this data in a formula. If a grader changes a sale's price, your spreadsheet should still work and automatically change all numbers) 3. (3 pts) Identify the assumptions implicit in break-even analysis. 4. (6 pts) John Coop argues that individual product break-even points need to be computed. a. Using the data from Exhibit 3, calculate the break-even in both units and sales dollars. b. Why is the sum of the three items (in both units and dollars) not equal to the total break even numbers you computed in requirement #12 All remaining questions relate to next year projections 5. (4 pts) Recreate Exhibit 3 incorporating the original and revised information provided by the participants. Create a separate legend based on line numbers so I can clearly follow your work Fixed costs should be allocated proportionally based upon the original allocation. The average unit variable cost should be a weighted average. Exhibit 3 Product class Cost Analysis - normal year Agregate Product Product & Products Une Last year Next year last year Next year Last year Next year Last year Sales at full Capacity (unl 2,000,000 Actual Sales Volume (un 1,500,000 600,000 400,000 500,000 Unit sales price 5 7.20 S 10.00 $ 9.00 5 2.40 Vanable cost per unit Fixed costs 5.2.970,000 S960,000 $ 1,560,000 $ 450,000 Next year 1 2 5 4.50 7.50 $ S 1.50 Uutization of Capacity 20%. Legend Une 1 Product A volume increased by 5,000,000. Bincreased by 42,000 and decreased by 40,000 (note this is just an example) 6. Ints) Prepare a responsibility margin income statement including taxes as a separately listed remaining questions relate to next year projections. 5. pts) Recreate Exhibit 3 incorporating the original and revised information provided by the participants. Create a separate legend based on line numbers so I can clearly follow your work. Fixed costs should be allocated proportionally based upon the original allocation. The average unit variable cost should be a weighted average. Exhibit 3 Product class Cost Analysis - normal year Aggregate Product A Product B Product C Une Last year Next year Last year Next year Last year Next year Last year Sales at full Capacity (uni 2,000,000 Actual Sales Volume (un 1,500,000 600,000 400,000 500,000 Unit sales price $ $ 2.40 Variable cost per unit $ 7.50 $ $ 2,970,000 $ 960,000 $ 450,000 Next year 1 10.00 Nm $ $ 7.20 4.50 $ 9.00 3.75 $ 1,560,000 $ 1.50 4 Fixed costs Utilization of Capacity 75% 30% 20% 25% Legend Line 1 Product A volume increased by 5,000,000, 8 increased by 42,000 and C decreased by 40,000 (note this is just an example) 6. (4 pts) Prepare a responsibility margin income statement including taxes as a separately listed cost after operating income (this would include a total and the three products. Although you allocated fixed costs in #5, do not allocate fixed costs or taxes.) 7. (4 pts) Compute the break-even point in revenues (for the business as a whole assuming the product sales mix for units remains constant.) 8. (4 pts) Compute the level of revenues that must be achieved to pay the projected dividend and meet the retention objectives of after tax income. Dave asked Means to present her finding to the larger community of employees at the firm. Several reprintatives the manufacturing departments were present, as well as the metal sales manage to tant sales managers, the purchasing office and we people from production in Follow is chart of these senting tahlar Matripants) Staff Accountant Controller Product Control Manfacturing Assistant Sales Manager General Sales Manager Administrative Assistant to the President The follow the Alam concerned that this analysis has not allowed for the planned changes in volume next Star The sales departments that we will boost titles which will result in phi 90% you are talking about 90% of capacity, then you better comider the fact that we have received approval ansvestment for an expansion of the plant that will increase fixed costs try $40,000 We may call i capacity, but there are places that we really cannot produce any more. y be right. But this becak-even analysis uses average figures and does not take into cott we are dealing with the basic products. Thave brought the report that the accounting department produced en product line costs last year see Exhibit 3 This information makes a very clear that you werage" is way out of line. How would the beak-even prick if we took this can Latinal product basis? you are paring to do something with individuel products, you should know that we are Woking into a hug shift in our product mix. The line is really losing out and I imagine that we will be fucky to hold two-think of its volume next you hack me up on this. However, we should pick up the 200.000 that we will lose plus about a quarter milties more units in production Product "Esolid for years and there should be so changes in volume Ale note that his estimates of the volume increases are on the basis of oubling the price with no change in costs. We have been priced so low on this item and need to make the price since the price is out of line with other products in its class and the current prices inconsistent with our quality reputation. Second, we anticipate the increase in demand could not be lundied if we did not increase the price. It would be well above estimates, maybe by another half million. You Sdraic about capacity, we could not posibly fulfill the orders unless we increase the price I also feel that there are este consider First of all, let's member that profits are divided evenly between the povernment and us. After taxes we cely left with around 50% off peolitas shown by the beak-even analysis provided by cody, we paid ou dividends of $300,000 cholen. Since we have an anniversary year coming up, we would like to pay out pecial dividend 50lestra We need to retain S150,000 in the business. That means we would like to hit 600.000 or profit after taxe Athind concem is the upcoming reportations with the union. All indications are that we may have to increase wages which will increase the variable costs by 10%. This may kill the bonus dividend plan bu we have to hold the line on post profits. Any increase in wapes must be offset by added revenues ile old affect our brouk-even point ant to thank for preparing the presentation. It has certainly got us all to thinking about how we can improve the analysis and use it for next year First of all, the break-eventysis is based upon some assumption Some of the points and were really about those assumption it might help withe assumptions down in black md where so we can see how they influence the Next, I think we should adapt our analysis where possible to adjust for future changes. First, I think that would like to see calculations based upon an analysis of individual product lines. Also, as suggested, since the product mix is bound to change, why not see how things look if the shift materializes as he has forecast?kould like to see the influence of a price increase in the "C" line and looks toward an increase in fixed manufacturing costs of $60,000 a month as suggested that we consider taxes, dividends, expected union demands and the question of product emphasis Exhibit 3 Product class Cost Analysis - normal year Arererate Product A Product Product Sales at full Capacity (units) 2.000.000 Actual Sales Volume (units) 1.500.000 600,000 400,000 500.000 Unit sales price $ 7205 10.00 $ 9.00 $ 2.40 Variable cost per unit $ 4.50 7.505 3.75$ 1.50 Fixed costs $ 2.970,000 $ 960,000 $ 1.560,000 $ 450,000 Utilization of Capacity 30% 20% Required: (31 points) (note: you must use formulas to solve this problem. The best way to do this is to type in the case data at the top of the spreadsheet and use this data in a formula. If a grader changes a sale's price, your spreadsheet should still work and automatically change all numbers) 3. (3 pts) Identify the assumptions implicit in break-even analysis 4. (6 pts gorgues that individual product break-even points need to be computed a. Using the data from Exhibit 3. calculate the break-even in both units and sales dollars 1. Why is the sum of the three items (in both units and dollars) not equal to the total becak even numbers you computed in requirement #l? All remaining questions relate to next year projections. 5. (4 pts) Recreate Exhibit 3 incorporating the original and revised information provided by the participants. Create a separate legend based on line numbers so I can clearly follow your work Fixed costs should be allocated proportionally based upon the original allocation. The average unit variable cost should be a weighted average Exhibit Product cats Cost Analysis formal year Aggregate Product Protect Last year Next year last year Next year antytar Next year. Last year Next year Sales atful Capacity on 2.000.000 Actual Sales Volume fun 1.500.000 500.000 100.000 500.000 2 Unitsale price 720 5 3000 5 200 5 2.40 3 Variable cost per 4.50 7.50 375 4 Fixed costs $ 2.970,000 $ 60,000 $ 0.00 550.000 Union of Cagay 79 Legend Line 1 Product A volume increased by 5.000.000, increased by 12.000 and decreased by 40 000 note this is just an example 6. (4 pts) Prepare a responsibility margin income statement including taxes as a separately listed cost after operating income (this would include a total and the three products. Although you allocated fixed costs in 5. do not allocate fixed costs or taxes.) 7. (4 pts) Compute the becak-even point in revenues (for the business as a whole assuming the product sales mix for units remains constant.) $ $ $ 150 8.4pts Compute the level of revenues that must be achieved to pay the projected dividend and meet the retention objectives of after tax income Dave asked Means to present her finding to the larger community of employees at the firm. Several reprintatives the manufacturing departments were present, as well as the metal sales manage to tant sales managers, the purchasing office and we people from production in Follow is chart of these senting tahlar Matripants) Staff Accountant Controller Product Control Manfacturing Assistant Sales Manager General Sales Manager Administrative Assistant to the President The follow the Alam concerned that this analysis has not allowed for the planned changes in volume next Star The sales departments that we will boost titles which will result in phi 90% you are talking about 90% of capacity, then you better comider the fact that we have received approval ansvestment for an expansion of the plant that will increase fixed costs try $40,000 We may call i capacity, but there are places that we really cannot produce any more. y be right. But this becak-even analysis uses average figures and does not take into cott we are dealing with the basic products. Thave brought the report that the accounting department produced en product line costs last year see Exhibit 3 This information makes a very clear that you werage" is way out of line. How would the beak-even prick if we took this can Latinal product basis? you are paring to do something with individuel products, you should know that we are Woking into a hug shift in our product mix. The line is really losing out and I imagine that we will be fucky to hold two-think of its volume next you hack me up on this. However, we should pick up the 200.000 that we will lose plus about a quarter milties more units in production Product "Esolid for years and there should be so changes in volume Ale note that his estimates of the volume increases are on the basis of oubling the price with no change in costs. We have been priced so low on this item and need to make the price since the price is out of line with other products in its class and the current prices inconsistent with our quality reputation. Second, we anticipate the increase in demand could not be lundied if we did not increase the price. It would be well above estimates, maybe by another half million. You Sdraic about capacity, we could not posibly fulfill the orders unless we increase the price I also feel that there are este consider First of all, let's member that profits are divided evenly between the povernment and us. After taxes we cely left with around 50% off peolitas shown by the beak-even analysis provided by cody, we paid ou dividends of $300,000 cholen. Since we have an anniversary year coming up, we would like to pay out pecial dividend 50lestra We need to retain S150,000 in the business. That means we would like to hit 600.000 or profit after taxe Athind concem is the upcoming reportations with the union. All indications are that we may have to increase wages which will increase the variable costs by 10%. This may kill the bonus dividend plan bu we have to hold the line on post profits. Any increase in wapes must be offset by added revenues ile old affect our brouk-even point ant to thank for preparing the presentation. It has certainly got us all to thinking about how we can improve the analysis and use it for next year First of all, the break-eventysis is based upon some assumption Some of the points and were really about those assumption it might help withe assumptions down in black md where so we can see how they influence the Next, I think we should adapt our analysis where possible to adjust for future changes. First, I think that would like to see calculations based upon an analysis of individual product lines. Also, as suggested, since the product mix is bound to change, why not see how things look if the shift materializes as he has forecast?kould like to see the influence of a price increase in the "C" line and looks toward an increase in fixed manufacturing costs of $60,000 a month as suggested that we consider taxes, dividends, expected union demands and the question of product emphasis Exhibit 3 Product class Cost Analysis - normal year Arererate Product A Product Product Sales at full Capacity (units) 2.000.000 Actual Sales Volume (units) 1.500.000 600,000 400,000 500.000 Unit sales price $ 7205 10.00 $ 9.00 $ 2.40 Variable cost per unit $ 4.50 7.505 3.75$ 1.50 Fixed costs $ 2.970,000 $ 960,000 $ 1.560,000 $ 450,000 Utilization of Capacity 30% 20% Required: (31 points) (note: you must use formulas to solve this problem. The best way to do this is to type in the case data at the top of the spreadsheet and use this data in a formula. If a grader changes a sale's price, your spreadsheet should still work and automatically change all numbers) 3. (3 pts) Identify the assumptions implicit in break-even analysis 4. (6 pts gorgues that individual product break-even points need to be computed a. Using the data from Exhibit 3. calculate the break-even in both units and sales dollars 1. Why is the sum of the three items (in both units and dollars) not equal to the total becak even numbers you computed in requirement #l? All remaining questions relate to next year projections. 5. (4 pts) Recreate Exhibit 3 incorporating the original and revised information provided by the participants. Create a separate legend based on line numbers so I can clearly follow your work Fixed costs should be allocated proportionally based upon the original allocation. The average unit variable cost should be a weighted average Exhibit Product cats Cost Analysis formal year Aggregate Product Protect Last year Next year last year Next year antytar Next year. Last year Next year Sales atful Capacity on 2.000.000 Actual Sales Volume fun 1.500.000 500.000 100.000 500.000 2 Unitsale price 720 5 3000 5 200 5 2.40 3 Variable cost per 4.50 7.50 375 4 Fixed costs $ 2.970,000 $ 60,000 $ 0.00 550.000 Union of Cagay 79 Legend Line 1 Product A volume increased by 5.000.000, increased by 12.000 and decreased by 40 000 note this is just an example 6. (4 pts) Prepare a responsibility margin income statement including taxes as a separately listed cost after operating income (this would include a total and the three products. Although you allocated fixed costs in 5. do not allocate fixed costs or taxes.) 7. (4 pts) Compute the becak-even point in revenues (for the business as a whole assuming the product sales mix for units remains constant.) $ $ $ 150 8.4pts Compute the level of revenues that must be achieved to pay the projected dividend and meet the retention objectives of after tax income John Coop: I am concerned that this analysis has not allowed for the planned changes in volume next year. The sales department guesses that we will boost unit sales which will result in us pushing 90% capacity. Fred Westover: If you are talking about 90% of capacity, then you better consider the fact that we have recei roval on an investment for an expansion of the plant that will increase fixed costs by $60,000 a monta ve may call it 90% capacity, but there are places that we really cannot produce any more. John Coop: Fred may be right, but this break-even analysis uses average figures and does not tak account that we are dealing with three basic products. I have brought the report that the accounting department produced on product line costs last year (see Exhibit 3). This information makes it very clear that your "average" is way out of line. How would the break-even point look if we took this on an individual product basis? Ray Bradley: If you are going to do something with individual products, you should know that we are looking into a big shift in our product mix. The "A" line is really losing out and I imagine that we will be lucky to hold two-thirds of its volume next year. Arnie can back me up on this. However, we should pick up the 200,000 that we will lose plus about a quarter million more units in "C"production. Product "B" has been solid for years and there should be no changes in volume. Arnie Winst: I agree with Bradley. Also, note that his estimates of the volume increases are on the basis of doubling the price with no change in costs. We have been priced so low on this item and need to raise the price since the price is out of line with other products in its class and the current price is inconsistent with our quality reputation. Second, we anticipate the increase in demand could not be handled if we did not increase the price. It would be well above Bradley's estimates, maybe by another half million. You heard the discussions about capacity, we could not possibly fulfill the orders unless we increase the price. Andy Fraser: I also feel that there are items to consider. First of all, let's remember that profits are divided evenly between the goverment and us. After taxes, we are only left with around 50% of our profit as shown by the break-even analysis provided by Ann Means. Secondly, we paid out dividends of $300,000 to stockholders. Since we have an anniversary year coming up, we would like to pay out a special dividend of 50% extra. We need to retain S150,000 in the business also. That means we would like to hit $600,000 of profit after taxes. A third concern is the upcoming negotiations with the union. All indications are that we may have to increase wages which will increase the variable costs by 10%. This may kill the bonus dividend plan but we have to hold the line on past profits. Any increase in wages must be offset by added revenues. 1 would think that would affect our break-even point Sara Davids: I want to thank Ann for preparing the presentation. It has certainly got us all to thinking about how we can improve this analysis and use it for next year. First of all, the break-even analysis is based upon some assumptions. Some of the points raised were really about those assumptions. It might help us if Ann set the assumptions down in black and white so we can see how they influence the analysis Next, I think we should adapt our analysis where possible to adjust for future changes. First, I think that Johny like to see calculations based upon an analysis of individual product lines. Also, as Ray sugges e the product mix is bound to change, why not see how things look if the shift materializes as he has forecast? Arnie would like to see the influence of a price increase in the "C" line and Fred looks toward an increase in fixed manufacturing costs of $60,000 a month. Andy has suggested that we consider taxes, dividends, expected union demands and the question of product emphasis. Exhibit 3 Product class Cost Analysis - normal year Aggregate Product A Product B Product C Sales at full Capacity (units) 2,000,000 Actual Sales Volume (units) 1,500,000 600,000 400,000 500,000 Unit sales price $ 7.20 $ 10.00 $ 9.00 $ 2.40 Variable cost per unit $ 4.50 $ 7.50 $ 3.75 $ 1.50 Fixed costs $ 2,970,000 $ 960,000 $ 1,560,000 $ 450,000 75% 30% 209 25% Utilization of Capacity Required: (31 points) (note: you must use formulas to solve this problem. The best way to do this is to type in the case data at the top of the spreadsheet and use this data in a formula. If a grader changes a sale's price, your spreadsheet should still work and automatically change all numbers) 3. (3 pts) Identify the assumptions implicit in break-even analysis. 4. (6 pts) John Coop argues that individual product break-even points need to be computed. a. Using the data from Exhibit 3, calculate the break-even in both units and sales dollars. b. Why is the sum of the three items (in both units and dollars) not equal to the total break even numbers you computed in requirement #12 All remaining questions relate to next year projections 5. (4 pts) Recreate Exhibit 3 incorporating the original and revised information provided by the participants. Create a separate legend based on line numbers so I can clearly follow your work Fixed costs should be allocated proportionally based upon the original allocation. The average unit variable cost should be a weighted average. Exhibit 3 Product class Cost Analysis - normal year Agregate Product Product & Products Une Last year Next year last year Next year Last year Next year Last year Sales at full Capacity (unl 2,000,000 Actual Sales Volume (un 1,500,000 600,000 400,000 500,000 Unit sales price 5 7.20 S 10.00 $ 9.00 5 2.40 Vanable cost per unit Fixed costs 5.2.970,000 S960,000 $ 1,560,000 $ 450,000 Next year 1 2 5 4.50 7.50 $ S 1.50 Uutization of Capacity 20%. Legend Une 1 Product A volume increased by 5,000,000. Bincreased by 42,000 and decreased by 40,000 (note this is just an example) 6. Ints) Prepare a responsibility margin income statement including taxes as a separately listed remaining questions relate to next year projections. 5. pts) Recreate Exhibit 3 incorporating the original and revised information provided by the participants. Create a separate legend based on line numbers so I can clearly follow your work. Fixed costs should be allocated proportionally based upon the original allocation. The average unit variable cost should be a weighted average. Exhibit 3 Product class Cost Analysis - normal year Aggregate Product A Product B Product C Une Last year Next year Last year Next year Last year Next year Last year Sales at full Capacity (uni 2,000,000 Actual Sales Volume (un 1,500,000 600,000 400,000 500,000 Unit sales price $ $ 2.40 Variable cost per unit $ 7.50 $ $ 2,970,000 $ 960,000 $ 450,000 Next year 1 10.00 Nm $ $ 7.20 4.50 $ 9.00 3.75 $ 1,560,000 $ 1.50 4 Fixed costs Utilization of Capacity 75% 30% 20% 25% Legend Line 1 Product A volume increased by 5,000,000, 8 increased by 42,000 and C decreased by 40,000 (note this is just an example) 6. (4 pts) Prepare a responsibility margin income statement including taxes as a separately listed cost after operating income (this would include a total and the three products. Although you allocated fixed costs in #5, do not allocate fixed costs or taxes.) 7. (4 pts) Compute the break-even point in revenues (for the business as a whole assuming the product sales mix for units remains constant.) 8. (4 pts) Compute the level of revenues that must be achieved to pay the projected dividend and meet the retention objectives of after tax income

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts