Answered step by step

Verified Expert Solution

Question

1 Approved Answer

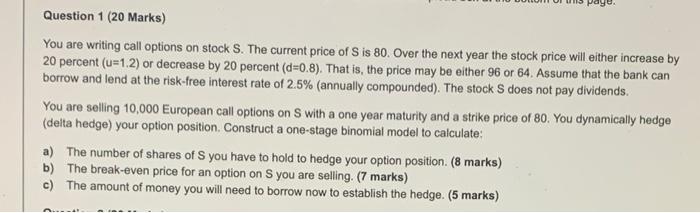

Delta hedging Question 1 (20 Marks) You are writing call options on stock S. The current price of Sis 80. Over the next year the

Delta hedging

Question 1 (20 Marks) You are writing call options on stock S. The current price of Sis 80. Over the next year the stock price will either increase by 20 percent (u=1.2) or decrease by 20 percent (d=0.8). That is, the price may be either 96 or 64. Assume that the bank can borrow and lend at the risk-free interest rate of 2.5% (annually compounded). The stock S does not pay dividends. You are selling 10.000 European call options on with a one year maturity and a strike price of 80. You dynamically hedge (delta hedge) your option position, Construct a one-stage binomial model to calculate: a) The number of shares of S you have to hold to hedge your option position. (8 marks) b) The break-even price for an option on S you are selling. (7 marks) c) The amount of money you will need to borrow now to establish the hedge Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Asset Allocation Strategies For Mutual Funds Evaluating Performance Risk And Return

Authors: Giuseppe Galloppo

1st Edition

3030761274,3030761282