Answered step by step

Verified Expert Solution

Question

1 Approved Answer

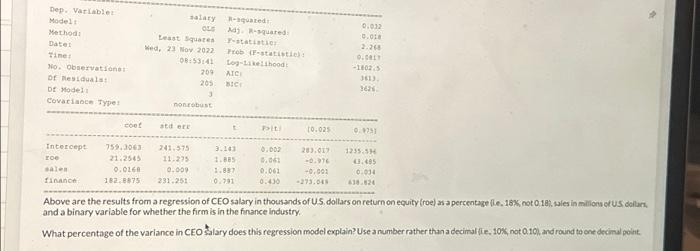

Dep. Variable: Model: Method: Date: Time: No. Observations: Df Residuals: Df Model: Covariance Type: Intercept roe sales finance. coef 759.3063 21.2545 0.0168 182.8875 salary OLS

Dep. Variable: Model: Method: Date: Time: No. Observations: Df Residuals: Df Model: Covariance Type: Intercept roe sales finance. coef 759.3063 21.2545 0.0168 182.8875 salary OLS Least Squares Wed, 23 Nov 2022 08:53:41 nonrobust std err 209 205 3 241.575 11.275 0.009 231.251 R-squared: Adj. R-squared: F-statistic: Prob (F-statistic): Log-Likelihood: AIC: BIC: t 3.143 1.885 1.887 0.791 P>|t| 0.002 0.061 0.061 0.430 =========== [0.025 283.017 -0.976 -0.001 -273.049 0.032 0.018 2.268 0.0817 -1802.5 3613. 3626. ===== 0.975] 1235.596 43.485 0.034 638.824 ===== -p Above are the results from a regression of CEO salary in thousands of U.S. dollars on return on equity (roe) as a percentage (i.e., 18%, not 0.18), sales in millions of U.S. dollars, and a binary variable for whether the firm is in the finance industry. What percentage of the variance in CEO salary does this regression model explain? Use a number rather than a decimal (i.e., 10%, not 0.10), and round to one decimal point.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing and Accounting Cases Investigating Issues of Fraud and Professional Ethics

Authors: Jay Thibodeau, Deborah Freier

4th edition

78025567, 978-0078025563