Answered step by step

Verified Expert Solution

Question

1 Approved Answer

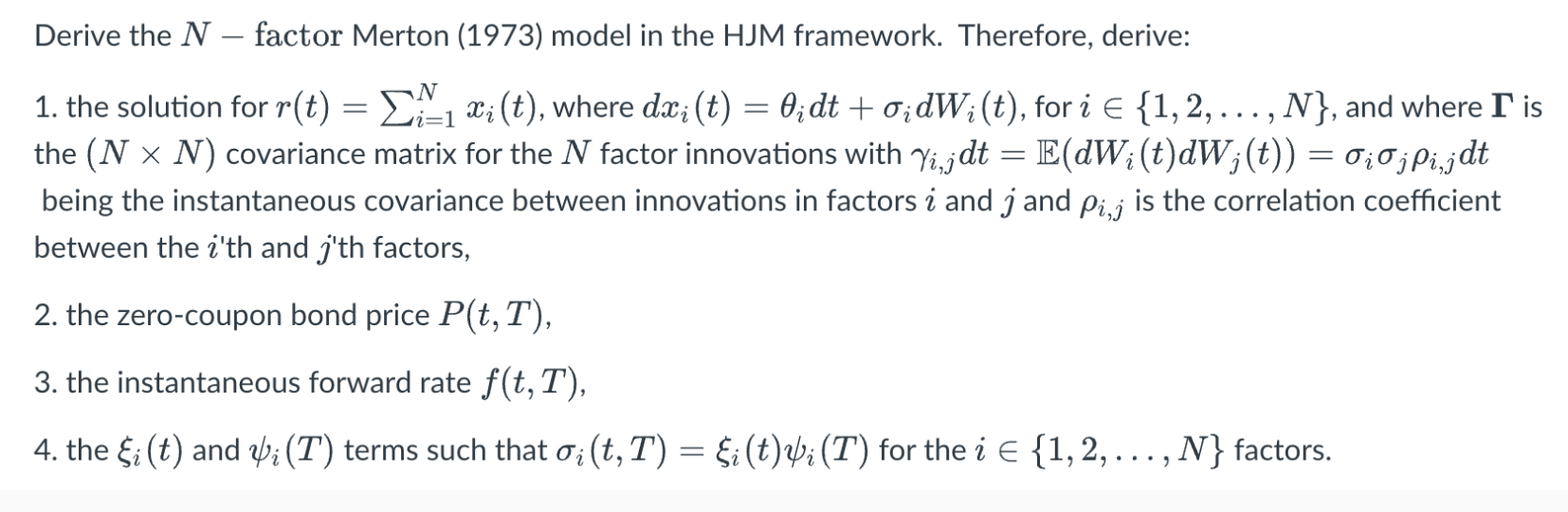

Derive the N - factor Merton ( 1 9 7 3 ) model in the HJM framework. Therefore, derive: the solution for r ( t

Derive the factor Merton model in the HJM framework. Therefore, derive:

the solution for where for iindots, and where is

the covariance matrix for the factor innovations with

being the instantaneous covariance between innovations in factors i and and is the correlation coefficient

between the th and th factors,

the zerocoupon bond price

the instantaneous forward rate

the and terms such that for the iindots, factors. please derive it with full derivation solution. not just with explaination on how to do it thanks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Finance Theory And Policy

Authors: Steven Michael Suranovic

1st Edition

193612646X, 9781936126460