Answered step by step

Verified Expert Solution

Question

1 Approved Answer

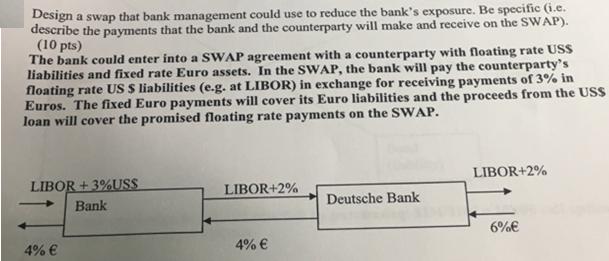

Design a swap that bank management could use to reduce the bank's exposure. Be specific (i.e. describe the payments that the bank and the

Design a swap that bank management could use to reduce the bank's exposure. Be specific (i.e. describe the payments that the bank and the counterparty will make and receive on the SWAP). (10 pts) The bank could enter into a SWAP agreement with a counterparty with floating rate USS liabilities and fixed rate Euro assets. In the SWAP, the bank will pay the counterparty's floating rate US $ liabilities (e.g. at LIBOR) in exchange for receiving payments of 3% in Euros. The fixed Euro payments will cover its Euro liabilities and the proceeds from the USS loan will cover the promised floating rate payments on the SWAP. LIBOR +3%USS Bank 4% LIBOR+2% 4% Deutsche Bank LIBOR+2% 6%

Step by Step Solution

★★★★★

3.43 Rating (169 Votes )

There are 3 Steps involved in it

Step: 1

In this diagram the bank side represents the cash flows that the bank will make and receive while the counterparty side represents the cash flows that the counterparty will make and receive On the ban...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Information System

Authors: James A. Hall

7th Edition

978-1439078570, 1439078572