Did Abby compute the cost of the Breeland Ltd. special order correctly before the weekend get-together? If not, how was her cost estimate and/or price determination flawed?

Whose assessment of the costing of this special order do you believe is correctGeorge Smilee's or Abby Conroy's? That is, should George's conversations with Josh impact Abby's cost estimate of the Breeland Ltd. special order? Explain your answer.

Are there any ethical issues related to the cost determination on the Breeland Ltd. special order? If so, what issues are present? How should Abby resolve these conflicts? Should Abby go directly to Tom Brennen about this new development? How can Abby use the IMA Statement of Ethical Professional Practice as a guide for her actions?

If Abby were to modify her original cost estimate of the Breeland Ltd. special order to include Josh's purchase of the remaining 10 gallons of XO-1600, what price determination would she have arrived at? What impact would that have had on Ace Fertilizer's bottom line?

If Abby were to modify her original cost estimate of the Breeland Ltd. special order to include Josh's purchase of the remaining 10 gallons of XO-1600, what price determination would she have arrived at? What impact would that have had on Ace Fertilizer's bottom line?

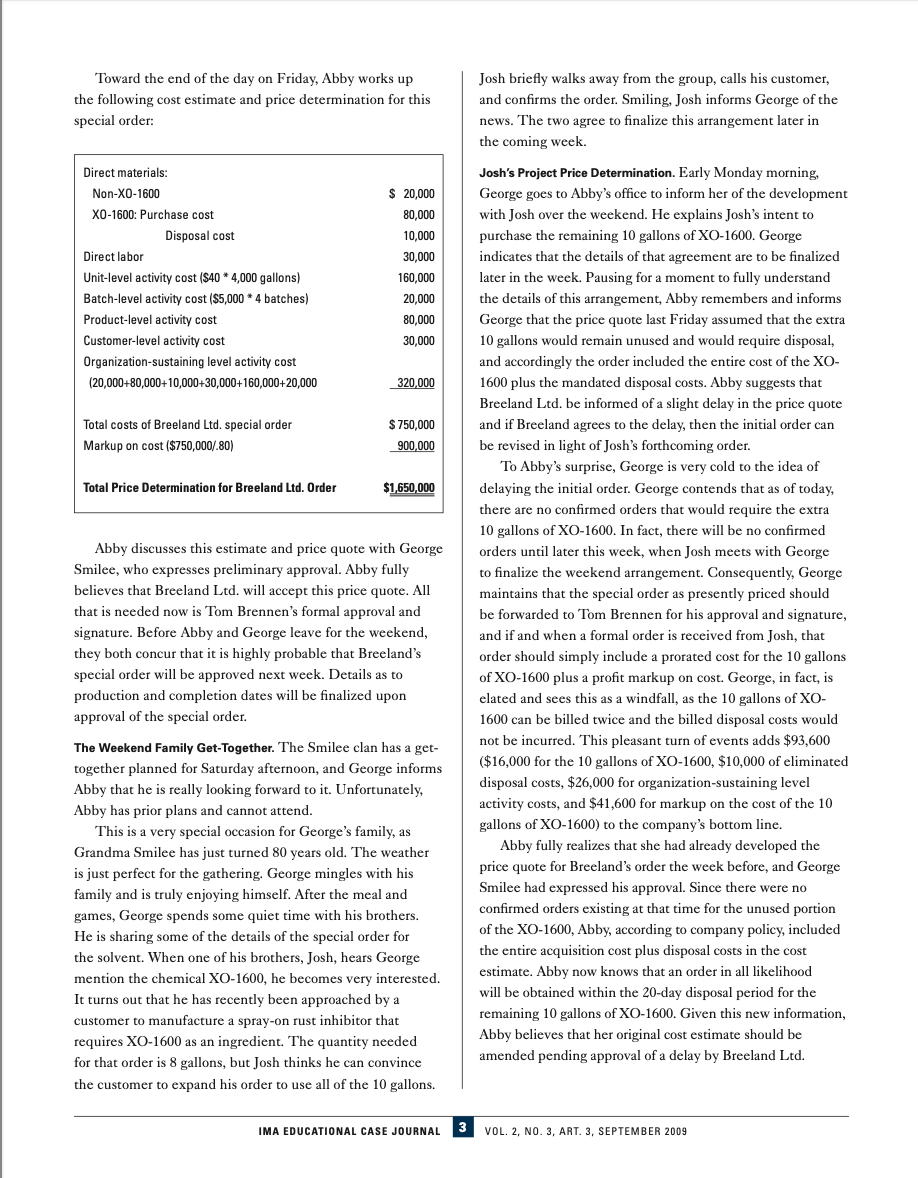

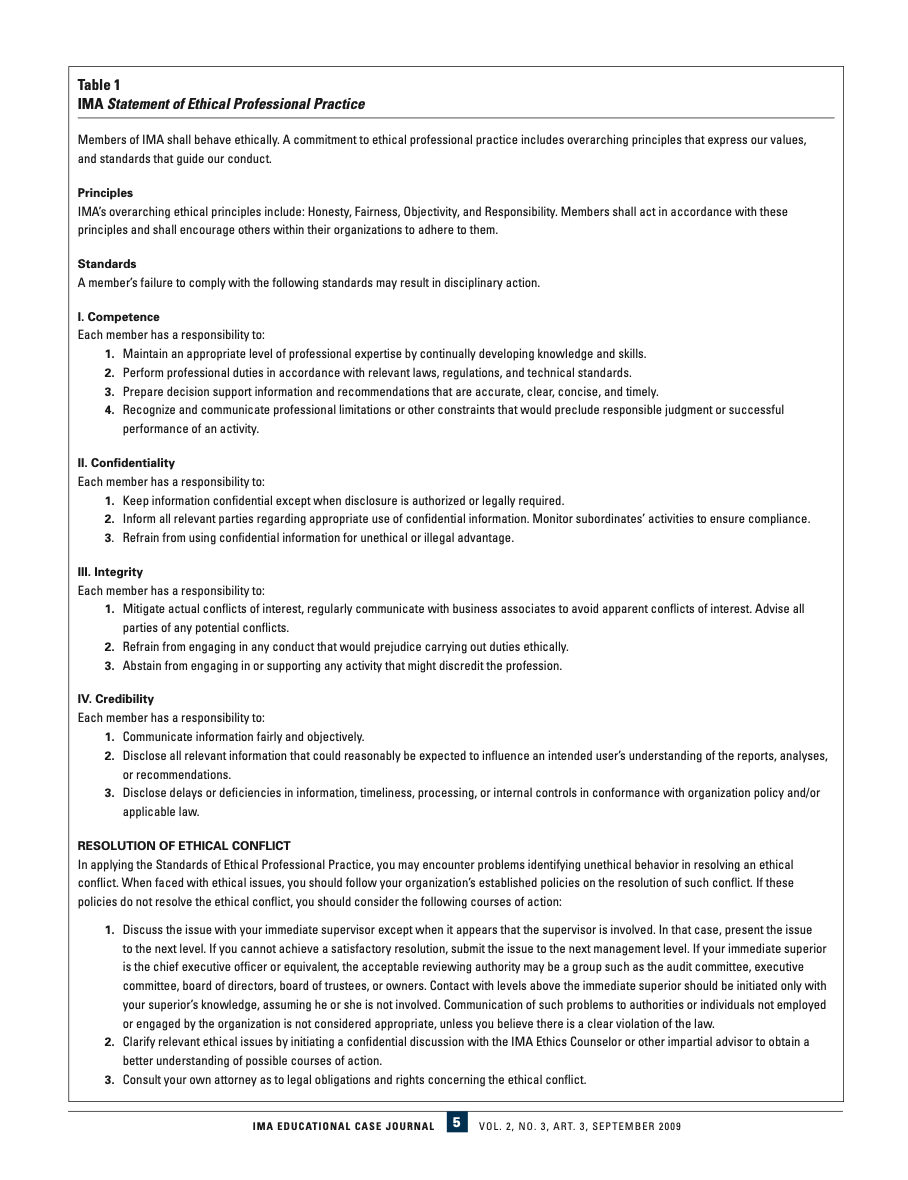

Ace Fertilizer Company: Ethical Cost Allocations and Price Determination Jerry Kreuze Sheldon Langsam Western Michigan University Western Michigan University INTRODUCTION contracts. Completed, initialed customer contracts then proceed to Tom Brennen for his ultimate approval and signature. \begin{tabular}{l|l} Toward the end of the day on Friday, Abby works up & Josh briefly walks away from the group, calls his customer, \end{tabular} the following cost estimate and price determination for this and confirms the order. Smiling, Josh informs George of the special order: news. The two agree to finalize this arrangement later in the coming week. Josh's Project Price Determination. Early Monday morning, George goes to Abby's office to inform her of the development with Josh over the weekend. He explains Josh's intent to purchase the remaining 10 gallons of XO1600. George indicates that the details of that agreement are to be finalized later in the week. Pausing for a moment to fully understand the details of this arrangement, Abby remembers and informs George that the price quote last Friday assumed that the extra 10 gallons would remain unused and would require disposal, and accordingly the order included the entire cost of the XO1600 plus the mandated disposal costs. Abby suggests that Breeland Ltd. be informed of a slight delay in the price quote and if Breeland agrees to the delay, then the initial order can be revised in light of Josh's forthcoming order. To Abby's surprise, George is very cold to the idea of delaying the initial order. George contends that as of today, there are no confirmed orders that would require the extra 10 gallons of XO-1600. In fact, there will be no confirmed Abby discusses this estimate and price quote with George orders until later this week, when Josh meets with George Smilee, who expresses preliminary approval. Abby fully to finalize the weekend arrangement. Consequently, George believes that Breeland Ltd. will accept this price quote. All maintains that the special order as presently priced should that is needed now is Tom Brennen's formal approval and be forwarded to Tom Brennen for his approval and signature, signature. Before Abby and George leave for the weekend, and if and when a formal order is received from Josh, that they both concur that it is highly probable that Breeland's order should simply include a prorated cost for the 10 gallons \begin{tabular}{l|l} special order will be approved next week. Details as to & of XO-1600 plus a profit markup on cost. George, in fact, is \end{tabular} production and completion dates will be finalized upon elated and sees this as a windfall, as the 10 gallons of XOapproval of the special order. 1600 can be billed twice and the billed disposal costs would The Weekend Family Get-Together. The Smilee clan has a get- not be incurred. This pleasant turn of events adds $93,600 together planned for Saturday afternoon, and George informs ($16,000 for the 10 gallons of XO-1600, $10,000 of eliminated Abby that he is really looking forward to it. Unfortunately, disposal costs, $26,000 for organization-sustaining level Abby has prior plans and cannot attend. activity costs, and $41,600 for markup on the cost of the 10 gallons of XO-1600) to the company's bottom line. Alternatively, Abby would like to submit a revised quote to Breeland Ltd. if Josh's order is finalized within 20 days. Specifically, she would like to only bill Breeland Ltd. for 40 gallons of XO-1600, delete the disposal costs, and modify the organization-sustaining and profit on cost amounts. Josh would then be shipped the product and be billed for the cost of the 10 gallons of XO-1600. Contrary to George's suggestion, Abby believes that Josh should also be billed an appropriate organization-sustaining cost amount in addition to a profit on cost. Even these amounts, however, would result in a smaller profit margin for the special order and would not allow the company to meet its monthly profit goal. George Smilee seems adamant in his determination and has instructed Abby to develop a quote for Josh independent of the cost determination for the Breeland special order. George is meeting with Tom Brennen the first thing on Wednesday morning to get his approval and signature on the special order. Abby is contemplating what course of action she should take. She plans to rely, in part, on the guidance provided by the Institute of Management Accounting (IMA) in its Statement of Ethical Professional Practice, found in Table 1. Abby is wondering why George Smilee is not using this same guidance. She wonders if George would be taking a similar position if he also were a Certified Management Accountant (CMA). REQUIRED QUESTIONS 1. Did Abby compute the cost of the Breeland Ltd. special order correctly before the weekend get-together? If not, how was her cost estimate and/or price determination flawed? 2. Whose assessment of the costing of this special order do you believe is correct-George Smilee's or Abby Conroy's? That is, should George's conversations with Josh impact Abby's cost estimate of the Breeland Ltd. special order? Explain your answer. 3. Are there any ethical issues related to the cost determination on the Breeland Ltd. special order? If so, what issues are present? How should Abby resolve these conflicts? Should Abby go directly to Tom Brennen about this new development? How can Abby use the IMA Statement of Ethical Professional Practice as a guide for her actions? 4. If Abby were to modify her original cost estimate of the Breeland Ltd. special order to include Josh's purchase of the remaining 10 gallons of XO1600, what price determination would she have arrived at? What impact would that have had on Ace Fertilizer's bottom line? I. Competence Each member has a responsibility to: 1. Maintain an appropriate level of professional expertise by continually developing knowledge and skills. 2. Perform professional duties in accordance with relevant laws, regulations, and technical standards. 3. Prepare decision support information and recommendations that are accurate, clear, concise, and timely. 4. Recognize and communicate professional limitations or other constraints that would preclude responsible judgment or successful performance of an activity. II. Confidentiality Each member has a responsibility to: 1. Keep information confidential except when disclosure is authorized or legally required. 2. Inform all relevant parties regarding appropriate use of confidential information. Monitor subordinates' activities to ensure compliance. 3. Refrain from using confidential information for unethical or illegal advantage. III. Integrity Each member has a responsibility to: 1. Mitigate actual conflicts of interest, regularly communicate with business associates to avoid apparent conflicts of interest. Advise all parties of any potential conflicts. 2. Refrain from engaging in any conduct that would prejudice carrying out duties ethically. 3. Abstain from engaging in or supporting any activity that might discredit the profession. IV. Credibility Each member has a responsibility to: 1. Communicate information fairly and objectively. 2. Disclose all relevant information that could reasonably be expected to influence an intended user's understanding of the reports, analyses, or recommendations. 3. Disclose delays or deficiencies in information, timeliness, processing, or internal controls in conformance with organization policy and/or applicable law. RESOLUTION OF ETHICAL CONFLICT In applying the Standards of Ethical Professional Practice, you may encounter problems identifying unethical behavior in resolving an ethical conflict. When faced with ethical issues, you should follow your organization's established policies on the resolution of such conflict. If these policies do not resolve the ethical conflict, you should consider the following courses of action: 1. Discuss the issue with your immediate supervisor except when it appears that the supervisor is involved. In that case, present the issue to the next level. If you cannot achieve a satisfactory resolution, submit the issue to the next management level. If your immediate superior is the chief executive officer or equivalent, the acceptable reviewing authority may be a group such as the audit committee, executive committee, board of directors, board of trustees, or owners. Contact with levels above the immediate superior should be initiated only with your superior's knowledge, assuming he or she is not involved. Communication of such problems to authorities or individuals not employed or engaged by the organization is not considered appropriate, unless you believe there is a clear violation of the law. 2. Clarify relevant ethical issues by initiating a confidential discussion with the IMA Ethics Counselor or other impartial advisor to obtain a better understanding of possible courses of action. 3. Consult your own attorney as to legal obligations and rights concerning the ethical conflict. Ace Fertilizer Company: Ethical Cost Allocations and Price Determination Jerry Kreuze Sheldon Langsam Western Michigan University Western Michigan University INTRODUCTION contracts. Completed, initialed customer contracts then proceed to Tom Brennen for his ultimate approval and signature. \begin{tabular}{l|l} Toward the end of the day on Friday, Abby works up & Josh briefly walks away from the group, calls his customer, \end{tabular} the following cost estimate and price determination for this and confirms the order. Smiling, Josh informs George of the special order: news. The two agree to finalize this arrangement later in the coming week. Josh's Project Price Determination. Early Monday morning, George goes to Abby's office to inform her of the development with Josh over the weekend. He explains Josh's intent to purchase the remaining 10 gallons of XO1600. George indicates that the details of that agreement are to be finalized later in the week. Pausing for a moment to fully understand the details of this arrangement, Abby remembers and informs George that the price quote last Friday assumed that the extra 10 gallons would remain unused and would require disposal, and accordingly the order included the entire cost of the XO1600 plus the mandated disposal costs. Abby suggests that Breeland Ltd. be informed of a slight delay in the price quote and if Breeland agrees to the delay, then the initial order can be revised in light of Josh's forthcoming order. To Abby's surprise, George is very cold to the idea of delaying the initial order. George contends that as of today, there are no confirmed orders that would require the extra 10 gallons of XO-1600. In fact, there will be no confirmed Abby discusses this estimate and price quote with George orders until later this week, when Josh meets with George Smilee, who expresses preliminary approval. Abby fully to finalize the weekend arrangement. Consequently, George believes that Breeland Ltd. will accept this price quote. All maintains that the special order as presently priced should that is needed now is Tom Brennen's formal approval and be forwarded to Tom Brennen for his approval and signature, signature. Before Abby and George leave for the weekend, and if and when a formal order is received from Josh, that they both concur that it is highly probable that Breeland's order should simply include a prorated cost for the 10 gallons \begin{tabular}{l|l} special order will be approved next week. Details as to & of XO-1600 plus a profit markup on cost. George, in fact, is \end{tabular} production and completion dates will be finalized upon elated and sees this as a windfall, as the 10 gallons of XOapproval of the special order. 1600 can be billed twice and the billed disposal costs would The Weekend Family Get-Together. The Smilee clan has a get- not be incurred. This pleasant turn of events adds $93,600 together planned for Saturday afternoon, and George informs ($16,000 for the 10 gallons of XO-1600, $10,000 of eliminated Abby that he is really looking forward to it. Unfortunately, disposal costs, $26,000 for organization-sustaining level Abby has prior plans and cannot attend. activity costs, and $41,600 for markup on the cost of the 10 gallons of XO-1600) to the company's bottom line. Alternatively, Abby would like to submit a revised quote to Breeland Ltd. if Josh's order is finalized within 20 days. Specifically, she would like to only bill Breeland Ltd. for 40 gallons of XO-1600, delete the disposal costs, and modify the organization-sustaining and profit on cost amounts. Josh would then be shipped the product and be billed for the cost of the 10 gallons of XO-1600. Contrary to George's suggestion, Abby believes that Josh should also be billed an appropriate organization-sustaining cost amount in addition to a profit on cost. Even these amounts, however, would result in a smaller profit margin for the special order and would not allow the company to meet its monthly profit goal. George Smilee seems adamant in his determination and has instructed Abby to develop a quote for Josh independent of the cost determination for the Breeland special order. George is meeting with Tom Brennen the first thing on Wednesday morning to get his approval and signature on the special order. Abby is contemplating what course of action she should take. She plans to rely, in part, on the guidance provided by the Institute of Management Accounting (IMA) in its Statement of Ethical Professional Practice, found in Table 1. Abby is wondering why George Smilee is not using this same guidance. She wonders if George would be taking a similar position if he also were a Certified Management Accountant (CMA). REQUIRED QUESTIONS 1. Did Abby compute the cost of the Breeland Ltd. special order correctly before the weekend get-together? If not, how was her cost estimate and/or price determination flawed? 2. Whose assessment of the costing of this special order do you believe is correct-George Smilee's or Abby Conroy's? That is, should George's conversations with Josh impact Abby's cost estimate of the Breeland Ltd. special order? Explain your answer. 3. Are there any ethical issues related to the cost determination on the Breeland Ltd. special order? If so, what issues are present? How should Abby resolve these conflicts? Should Abby go directly to Tom Brennen about this new development? How can Abby use the IMA Statement of Ethical Professional Practice as a guide for her actions? 4. If Abby were to modify her original cost estimate of the Breeland Ltd. special order to include Josh's purchase of the remaining 10 gallons of XO1600, what price determination would she have arrived at? What impact would that have had on Ace Fertilizer's bottom line? I. Competence Each member has a responsibility to: 1. Maintain an appropriate level of professional expertise by continually developing knowledge and skills. 2. Perform professional duties in accordance with relevant laws, regulations, and technical standards. 3. Prepare decision support information and recommendations that are accurate, clear, concise, and timely. 4. Recognize and communicate professional limitations or other constraints that would preclude responsible judgment or successful performance of an activity. II. Confidentiality Each member has a responsibility to: 1. Keep information confidential except when disclosure is authorized or legally required. 2. Inform all relevant parties regarding appropriate use of confidential information. Monitor subordinates' activities to ensure compliance. 3. Refrain from using confidential information for unethical or illegal advantage. III. Integrity Each member has a responsibility to: 1. Mitigate actual conflicts of interest, regularly communicate with business associates to avoid apparent conflicts of interest. Advise all parties of any potential conflicts. 2. Refrain from engaging in any conduct that would prejudice carrying out duties ethically. 3. Abstain from engaging in or supporting any activity that might discredit the profession. IV. Credibility Each member has a responsibility to: 1. Communicate information fairly and objectively. 2. Disclose all relevant information that could reasonably be expected to influence an intended user's understanding of the reports, analyses, or recommendations. 3. Disclose delays or deficiencies in information, timeliness, processing, or internal controls in conformance with organization policy and/or applicable law. RESOLUTION OF ETHICAL CONFLICT In applying the Standards of Ethical Professional Practice, you may encounter problems identifying unethical behavior in resolving an ethical conflict. When faced with ethical issues, you should follow your organization's established policies on the resolution of such conflict. If these policies do not resolve the ethical conflict, you should consider the following courses of action: 1. Discuss the issue with your immediate supervisor except when it appears that the supervisor is involved. In that case, present the issue to the next level. If you cannot achieve a satisfactory resolution, submit the issue to the next management level. If your immediate superior is the chief executive officer or equivalent, the acceptable reviewing authority may be a group such as the audit committee, executive committee, board of directors, board of trustees, or owners. Contact with levels above the immediate superior should be initiated only with your superior's knowledge, assuming he or she is not involved. Communication of such problems to authorities or individuals not employed or engaged by the organization is not considered appropriate, unless you believe there is a clear violation of the law. 2. Clarify relevant ethical issues by initiating a confidential discussion with the IMA Ethics Counselor or other impartial advisor to obtain a better understanding of possible courses of action. 3. Consult your own attorney as to legal obligations and rights concerning the ethical conflict