Answered step by step

Verified Expert Solution

Question

1 Approved Answer

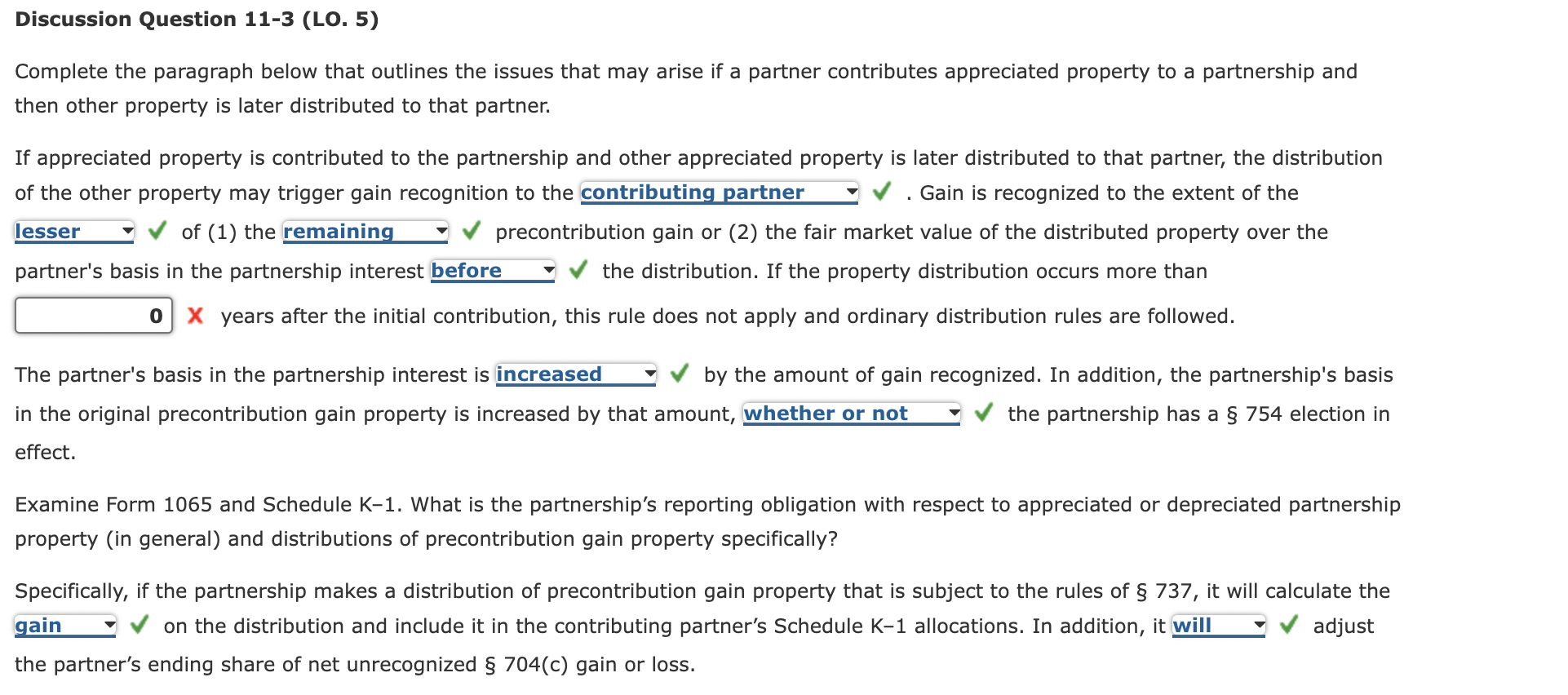

Discussion Question 11-3 (LO. 5) Complete the paragraph below that outlines the issues that may arise if a partner contributes appreciated property to a partnership

Discussion Question 11-3 (LO. 5) Complete the paragraph below that outlines the issues that may arise if a partner contributes appreciated property to a partnership and then other property is later distributed to that partner. If appreciated property is contributed to the partnership and other appreciated property is later distributed to that partner, the distribution of the other property may trigger gain recognition to the . Gain is recognized to the extent of the of (1) the precontribution gain or (2) the fair market value of the distributed property over the partner's basis in the partnership interest the distribution. If the property distribution occurs more than X years after the initial contribution, this rule does not apply and ordinary distribution rules are followed. The partner's basis in the partnership interest is by the amount of gain recognized. In addition, the partnership's basis in the original precontribution gain property is increased by that amount, the partnership has a 754 election in effect. Examine Form 1065 and Schedule K-1. What is the partnership's reporting obligation with respect to appreciated or depreciated partnership property (in general) and distributions of precontribution gain property specifically? Specifically, if the partnership makes a distribution of precontribution gain property that is subject to the rules of 737, it will calculate the on the distribution and include it in the contributing partner's Schedule K1 allocations. In addition, it adjust the partner's ending share of net unrecognized 704(c) gain or loss. Discussion Question 11-3 (LO. 5) Complete the paragraph below that outlines the issues that may arise if a partner contributes appreciated property to a partnership and then other property is later distributed to that partner. If appreciated property is contributed to the partnership and other appreciated property is later distributed to that partner, the distribution of the other property may trigger gain recognition to the . Gain is recognized to the extent of the of (1) the precontribution gain or (2) the fair market value of the distributed property over the partner's basis in the partnership interest the distribution. If the property distribution occurs more than X years after the initial contribution, this rule does not apply and ordinary distribution rules are followed. The partner's basis in the partnership interest is by the amount of gain recognized. In addition, the partnership's basis in the original precontribution gain property is increased by that amount, the partnership has a 754 election in effect. Examine Form 1065 and Schedule K-1. What is the partnership's reporting obligation with respect to appreciated or depreciated partnership property (in general) and distributions of precontribution gain property specifically? Specifically, if the partnership makes a distribution of precontribution gain property that is subject to the rules of 737, it will calculate the on the distribution and include it in the contributing partner's Schedule K1 allocations. In addition, it adjust the partner's ending share of net unrecognized 704(c) gain or loss

Discussion Question 11-3 (LO. 5) Complete the paragraph below that outlines the issues that may arise if a partner contributes appreciated property to a partnership and then other property is later distributed to that partner. If appreciated property is contributed to the partnership and other appreciated property is later distributed to that partner, the distribution of the other property may trigger gain recognition to the . Gain is recognized to the extent of the of (1) the precontribution gain or (2) the fair market value of the distributed property over the partner's basis in the partnership interest the distribution. If the property distribution occurs more than X years after the initial contribution, this rule does not apply and ordinary distribution rules are followed. The partner's basis in the partnership interest is by the amount of gain recognized. In addition, the partnership's basis in the original precontribution gain property is increased by that amount, the partnership has a 754 election in effect. Examine Form 1065 and Schedule K-1. What is the partnership's reporting obligation with respect to appreciated or depreciated partnership property (in general) and distributions of precontribution gain property specifically? Specifically, if the partnership makes a distribution of precontribution gain property that is subject to the rules of 737, it will calculate the on the distribution and include it in the contributing partner's Schedule K1 allocations. In addition, it adjust the partner's ending share of net unrecognized 704(c) gain or loss. Discussion Question 11-3 (LO. 5) Complete the paragraph below that outlines the issues that may arise if a partner contributes appreciated property to a partnership and then other property is later distributed to that partner. If appreciated property is contributed to the partnership and other appreciated property is later distributed to that partner, the distribution of the other property may trigger gain recognition to the . Gain is recognized to the extent of the of (1) the precontribution gain or (2) the fair market value of the distributed property over the partner's basis in the partnership interest the distribution. If the property distribution occurs more than X years after the initial contribution, this rule does not apply and ordinary distribution rules are followed. The partner's basis in the partnership interest is by the amount of gain recognized. In addition, the partnership's basis in the original precontribution gain property is increased by that amount, the partnership has a 754 election in effect. Examine Form 1065 and Schedule K-1. What is the partnership's reporting obligation with respect to appreciated or depreciated partnership property (in general) and distributions of precontribution gain property specifically? Specifically, if the partnership makes a distribution of precontribution gain property that is subject to the rules of 737, it will calculate the on the distribution and include it in the contributing partner's Schedule K1 allocations. In addition, it adjust the partner's ending share of net unrecognized 704(c) gain or loss Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Benefit Analysis With Reference To Environment And Ecology

Authors: James H. Meisel, K. Puttaswamaiah

1st Edition

1138521329, 978-1138521322