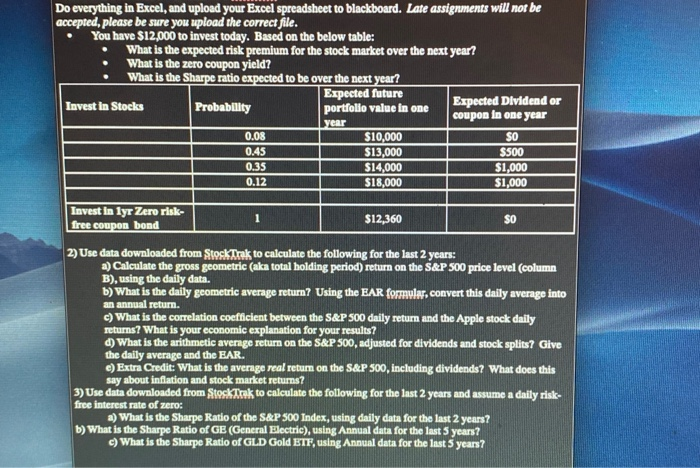

Do everything in Excel, and upload your Excel spreadsheet to blackboard. Late assignments will not be accepted, please be sure you upload the correct file. You have $12,000 to invest today. Based on the below table: What is the expected risk premium for the stock market over the next year? What is the zero coupon yield? What is the Sharpe ratio expected to be over the next year? Expected future Invest in Stocks Probability portfolio value in one Expected Dividend or coupon in one year year 0.08 $10,000 SO 0.45 $13,000 $500 0.35 $14,000 $1,000 0.12 $18,000 $1,000 Invest in lyr Zero risk- free coupon bond 1 $12,360 SO 2) Use data downloaded from StockTrak to calculate the following for the last 2 years: a) Calculate the gross geometric (aka total holding period) return on the S&P 500 price level (column B), using the daily data. b) What is the daily geometric average return? Using the EAR formular, convert this daily average into an annual retum. c) What is the correlation coefficient between the S&P 500 daily return and the Apple stock daily returns? What is your economic explanation for your results? d) What is the arithmetic average return on the S&P 500, adjusted for dividends and stock splits? Give the daily average and the EAR. e) Extra Credit: What is the average real return on the S&P 500, including dividends? What does this say about inflation and stock market returns? 3) Use data downloaded from StockTak to calculate the following for the last 2 years and assume a daily risk- free interest rate of zero: a) What is the Sharpe Ratio of the S&P 500 Index, using daily data for the last 2 years? b) What is the Sharpe Ratio of GE (General Electric), using Annual data for the last 5 years? c) What is the Sharpe Ratio of GLD Gold ETF, using Annual data for the last 5 years? Do everything in Excel, and upload your Excel spreadsheet to blackboard. Late assignments will not be accepted, please be sure you upload the correct file. You have $12,000 to invest today. Based on the below table: What is the expected risk premium for the stock market over the next year? What is the zero coupon yield? What is the Sharpe ratio expected to be over the next year? Expected future Invest in Stocks Probability portfolio value in one Expected Dividend or coupon in one year year 0.08 $10,000 SO 0.45 $13,000 $500 0.35 $14,000 $1,000 0.12 $18,000 $1,000 Invest in lyr Zero risk- free coupon bond 1 $12,360 SO 2) Use data downloaded from StockTrak to calculate the following for the last 2 years: a) Calculate the gross geometric (aka total holding period) return on the S&P 500 price level (column B), using the daily data. b) What is the daily geometric average return? Using the EAR formular, convert this daily average into an annual retum. c) What is the correlation coefficient between the S&P 500 daily return and the Apple stock daily returns? What is your economic explanation for your results? d) What is the arithmetic average return on the S&P 500, adjusted for dividends and stock splits? Give the daily average and the EAR. e) Extra Credit: What is the average real return on the S&P 500, including dividends? What does this say about inflation and stock market returns? 3) Use data downloaded from StockTak to calculate the following for the last 2 years and assume a daily risk- free interest rate of zero: a) What is the Sharpe Ratio of the S&P 500 Index, using daily data for the last 2 years? b) What is the Sharpe Ratio of GE (General Electric), using Annual data for the last 5 years? c) What is the Sharpe Ratio of GLD Gold ETF, using Annual data for the last 5 years