'DROP DOWN:

'DROP DOWN:

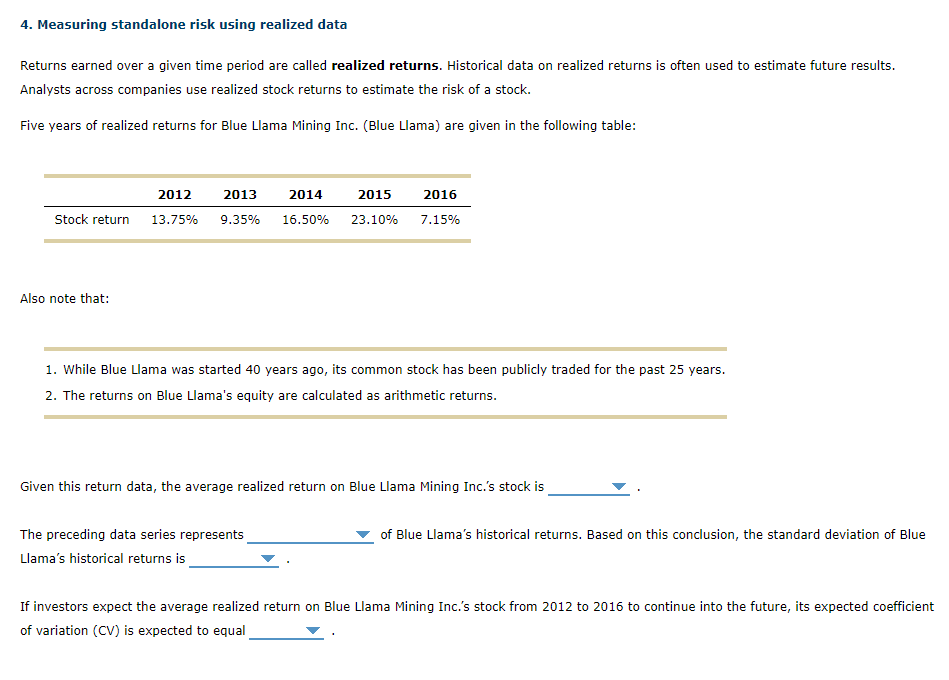

Given this return data, the average realized return on Blue Llama Mining Inc.s stock is (13.97%, 34.93%, 43.31%, 27.94%)

The preceding data series represents (A SAMPLE, THE POPULATION, THE UNIVERSE) _____ of Blue Llamas .historical returns. Based on this conclusion, the standard deviation of Blue Llamas historical returns is _______ (4.8342%, 8.4756%, 5.6154%, 6.2782%)

If investors expect the average realized return on Blue Llama Mining Inc.s stock from 2012 to 2016 to continue into the future, its expected coefficient of variation (CV) is expected to equal ________ (0.4494, 0.8314, 0.3775, 0.5168)

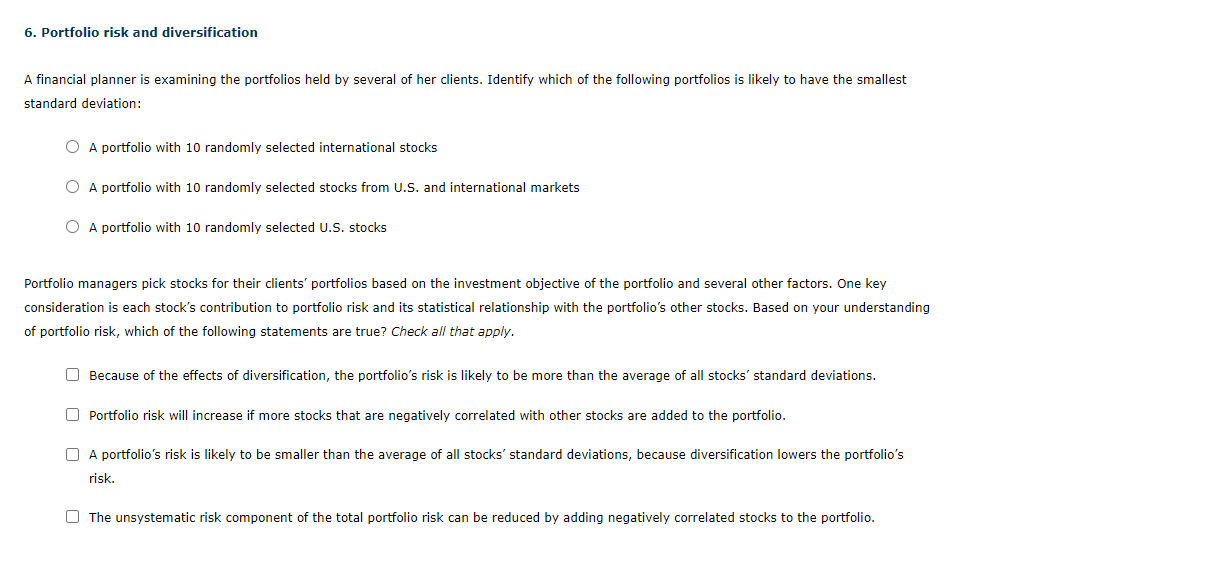

4. Measuring standalone risk using realized data Returns earned over a given time period are called realized returns. Historical data on realized returns is often used to estimate future results. Analysts across companies use realized stock returns to estimate the risk of a stock. Five years of realized returns for Blue Llama Mining Inc. (Blue Llama) are given in the following table: 2012 2013 2014 2015 2016 Stock return 13.75% 9.35% 16.50% 23.10% 7.15% Also note that: 1. While Blue Llama was started 40 years ago, its common stock has been publicly traded for the past 25 years. 2. The returns on Blue Llama's equity are calculated as arithmetic returns. Given this return data, the average realized return on Blue Llama Mining Inc.'s stock is of Blue Llama's historical returns. Based on this conclusion, the standard deviation of Blue The preceding data series represents Llama's historical returns is If investors expect the average realized return on Blue Llama Mining Inc.'s stock from 2012 to 2016 to continue into the future, its expected coefficient of variation (CV) is expected to equal 6. Portfolio risk and diversification A financial planner is examining the portfolios held by several of her clients. Identify which of the following portfolios is likely to have the smallest standard deviation: O A portfolio with 10 randomly selected international stocks O A portfolio with 10 randomly selected stocks from U.S. and international markets O A portfolio with 10 randomly selected U.S. stocks Portfolio managers pick stocks for their clients' portfolios based on the investment objective of the portfolio and several other factors. One key consideration is each stock's contribution to portfolio risk and its statistical relationship with the portfolio's other stocks. Based on your understanding of portfolio risk, which of the following statements are true? Check all that apply. Because of the effects of diversification, the portfolio's risk is likely to be more than the average of all stocks' standard deviations. Portfolio risk will increase if more stocks that are negatively correlated with other stocks are added to the portfolio. A portfolio's risk is likely to be smaller than the average of all stocks' standard deviations, because diversification lowers the portfolio's risk. The unsystematic risk component of the total portfolio risk can be reduced by adding negatively correlated stocks to the portfolio