Question

Dropdown 1st blank: distribution, payment, accumulation 2nd: distribution, payment, accumulation 3rd: buyer, annuitant, contributor 4th: paid for and retirement, paid for and survivorship distribution, paid

Dropdown

1st blank: distribution, payment, accumulation

2nd: distribution, payment, accumulation

3rd: buyer, annuitant, contributor

4th: paid for and retirement, paid for and survivorship distribution, paid for and distributed

5th: remainder, survivorship, unused

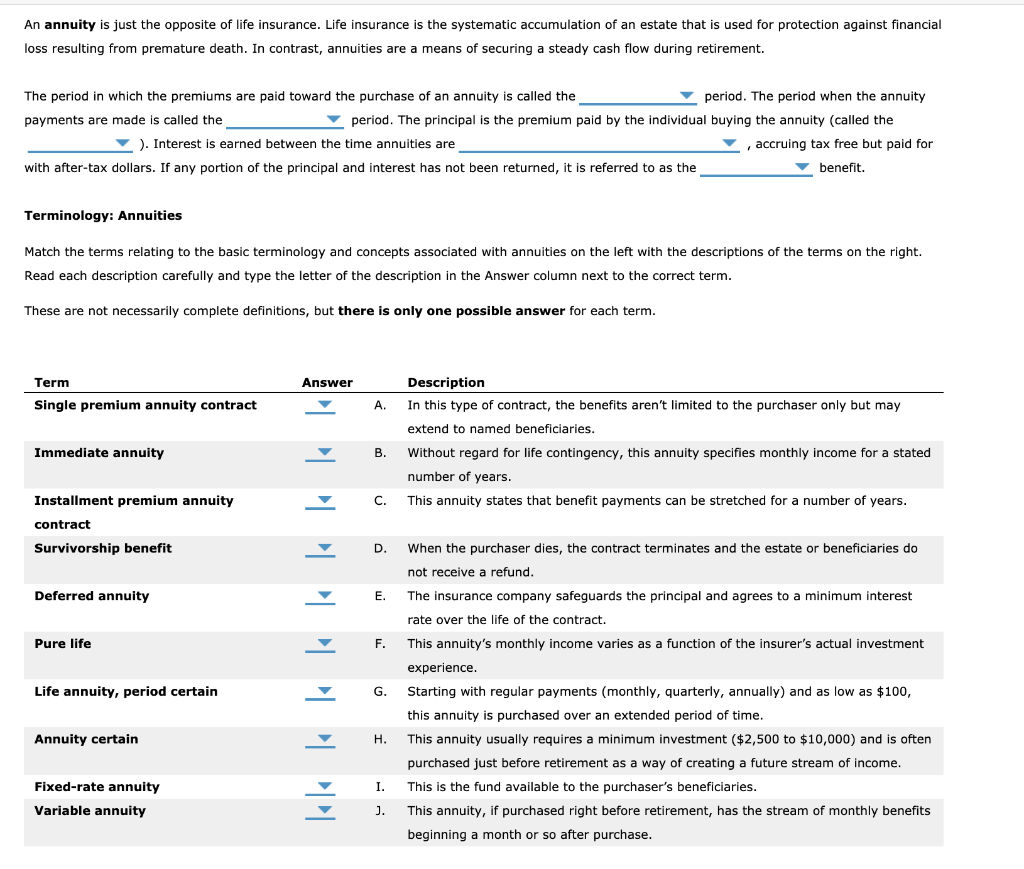

An annuity is just the opposite of life insurance. Life insurance is the systematic accumulation of an estate that is used for protection against financial loss resulting from premature death. In contrast, annuities are a means of securing a steady cash flow during retirement. The period in which the premiums are paid toward the purchase of an annuity is called the period. The period when the annuity payments are made is called the period. The principal is the premium paid by the individual buying the annuity (called the ). Interest is earned between the time annuities are accruing tax free but paid for with after-tax dollars. If any portion of the principal and interest has not been returned, it is referred to as the benefit. Terminology: Annuities Match the terms relating to the basic terminology and concepts associated with annuities on the left with the descriptions of the terms on the right. Read each description carefully and type the letter of the description in the Answer column next to the correct term. These are not necessarily complete definitions, but there is only one possible answer for each term. Answer Term Single premium annuity contract A. Description In this type of contract, the benefits aren't limited to the purchaser only but may extend to named beneficiaries. Immediate annuity Without regard for life contingency, this annuity specifies monthly income for a stated number of years. This annuity states that benefit payments can be stretched for a number of years. C. Installment premium annuity contract Survivorship benefit D. Deferred annuity E. MMMMMMMM Pure life F. Life annuity, period certain G. When the purchaser dies, the contract terminates and the estate or beneficiaries do not receive a refund. The insurance company safeguards the principal and agrees to a minimum interest rate over the life of the contract. This annuity's monthly income varies as a function of the insurer's actual investment experience. Starting with regular payments (monthly, quarterly, annually) and as low as $100, this annuity is purchased over an extended period of time This annuity usually requires a minimum investment ($2,500 to $10,000) and is often purchased just before retirement as a way of creating a future stream of income. This is the fund available to the purchaser's beneficiaries. This annuity, if purchased right before retirement, has the stream of monthly benefits beginning a month or so after purchase. Annuity certain H. Fixed-rate annuity Variable annuity I. J. An annuity is just the opposite of life insurance. Life insurance is the systematic accumulation of an estate that is used for protection against financial loss resulting from premature death. In contrast, annuities are a means of securing a steady cash flow during retirement. The period in which the premiums are paid toward the purchase of an annuity is called the period. The period when the annuity payments are made is called the period. The principal is the premium paid by the individual buying the annuity (called the ). Interest is earned between the time annuities are accruing tax free but paid for with after-tax dollars. If any portion of the principal and interest has not been returned, it is referred to as the benefit. Terminology: Annuities Match the terms relating to the basic terminology and concepts associated with annuities on the left with the descriptions of the terms on the right. Read each description carefully and type the letter of the description in the Answer column next to the correct term. These are not necessarily complete definitions, but there is only one possible answer for each term. Answer Term Single premium annuity contract A. Description In this type of contract, the benefits aren't limited to the purchaser only but may extend to named beneficiaries. Immediate annuity Without regard for life contingency, this annuity specifies monthly income for a stated number of years. This annuity states that benefit payments can be stretched for a number of years. C. Installment premium annuity contract Survivorship benefit D. Deferred annuity E. MMMMMMMM Pure life F. Life annuity, period certain G. When the purchaser dies, the contract terminates and the estate or beneficiaries do not receive a refund. The insurance company safeguards the principal and agrees to a minimum interest rate over the life of the contract. This annuity's monthly income varies as a function of the insurer's actual investment experience. Starting with regular payments (monthly, quarterly, annually) and as low as $100, this annuity is purchased over an extended period of time This annuity usually requires a minimum investment ($2,500 to $10,000) and is often purchased just before retirement as a way of creating a future stream of income. This is the fund available to the purchaser's beneficiaries. This annuity, if purchased right before retirement, has the stream of monthly benefits beginning a month or so after purchase. Annuity certain H. Fixed-rate annuity Variable annuity I. J

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Development Finance Innovations For Sustainable Growth

Authors: Nicholas Biekpe, Danny Cassimon, Andrew William Mullineux

1st Edition

331954165X, 978-3319541655