Answered step by step

Verified Expert Solution

Question

1 Approved Answer

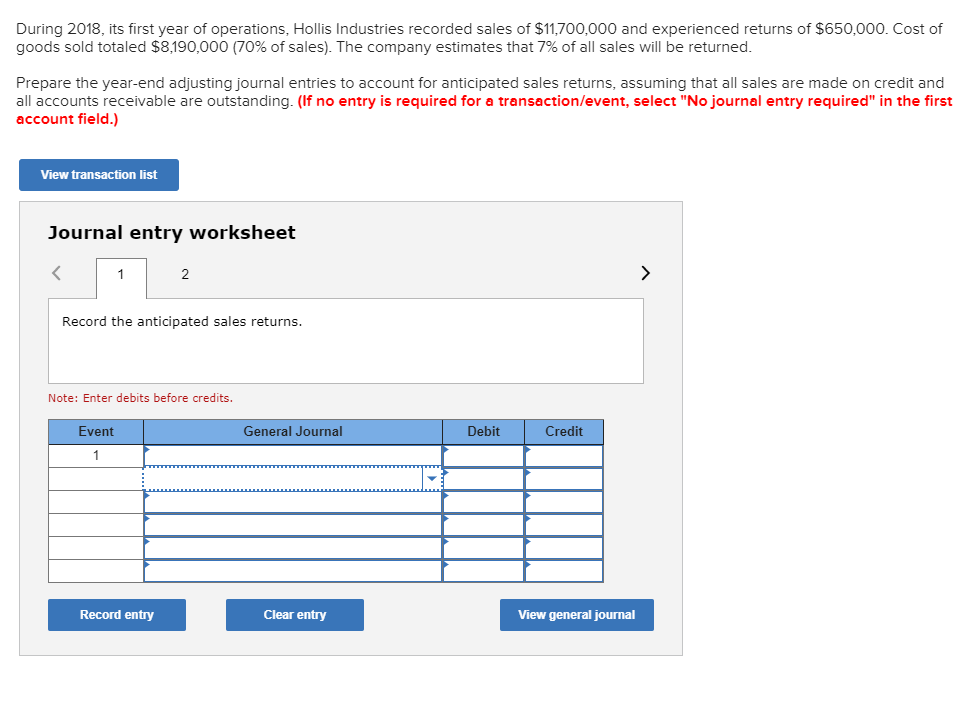

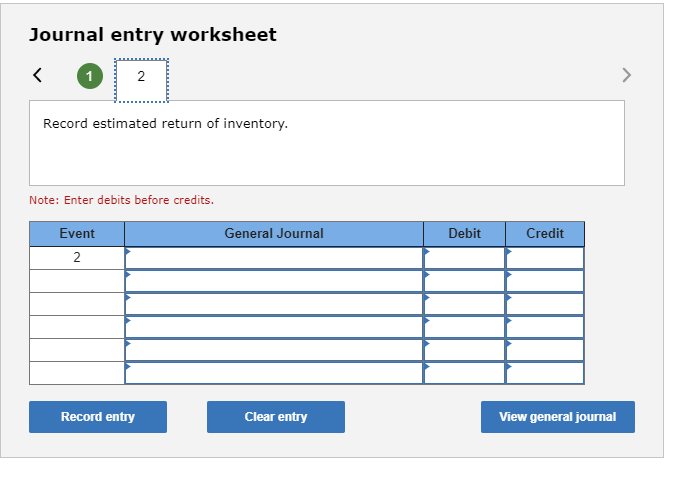

During 2018, its first year of operations, Hollis Industries recorded sales of $11,700,000 and experienced returns of $650,000. Cost of goods sold totaled $8,190,000 (70%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Teaching Calculation Audit And Test

Authors: Richard English

1st Edition

144627277X, 978-1446272770