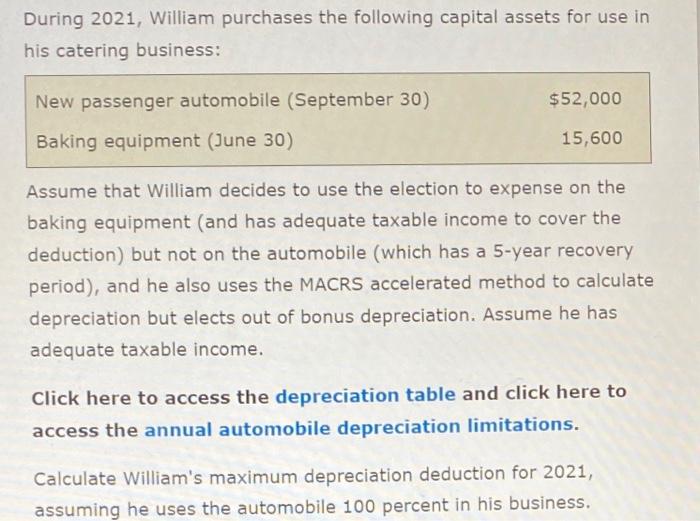

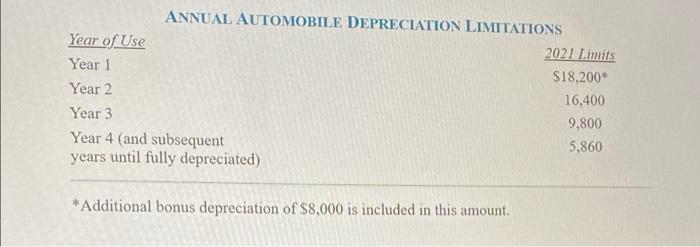

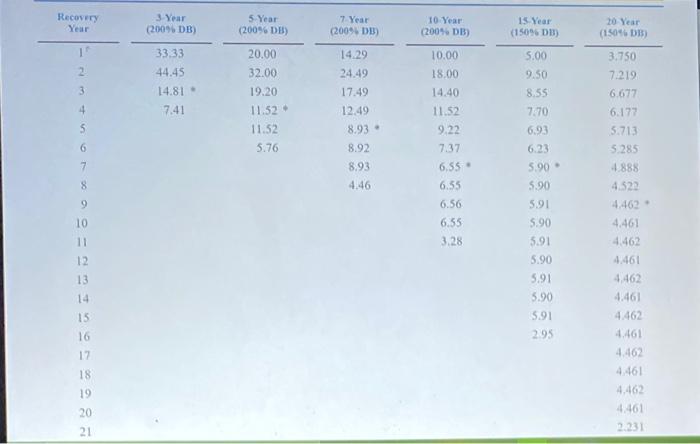

During 2021, William purchases the following capital assets for use in his catering business: New passenger automobile (September 30) $52,000 Baking equipment (June 30) 15,600 Assume that William decides to use the election to expense on the baking equipment (and has adequate taxable income to cover the deduction) but not on the automobile (which has a 5-year recovery period), and he also uses the MACRS accelerated method to calculate depreciation but elects out of bonus depreciation. Assume he has adequate taxable income. Click here to access the depreciation table and click here to access the annual automobile depreciation limitations. Calculate William's maximum depreciation deduction for 2021, assuming he uses the automobile 100 percent in his business. ANNUAL AUTOMOBILE DEPRECIATION LIMITATIONS Year of Use Year 1 Year 2 Year 3 Year 4 (and subsequent years until fully depreciated) Additional bonus depreciation of $8,000 is included in this amount. 2021 Limits $18,200* 16,400 9,800 5,860 Recovery Year 15 3 4 6 8 9 10 11 12 13 14 15 16 17 18 19 20 21 3-Year (200 % DB) 33.33 44.45 14.81 7.41 5-Year (200% DB) 20.00 32.00 19.20 11.52 11.52 5.76 17 Year (200% DB) 14.29 24.49 17.49 12.49 8.93. 8.92 8.93 4.46 10 Year: (200% DB) 10.00 18.00 14.40 11.52 9.22 7.37 6.55 6.55 6.56 6.55 3.28 15 Year (150% DB) 5.00 9.50 8.55 7.70 6.93 6.23 5.90 5.90 5.91 5.90 5.91 5.90 5.91 5.90 5.91 2.95 20 Year (150% DB) 3.750 7.219 6.677 6.177 5.713 5.285 4.888 4.522 4.462. 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 2.231 During 2021, William purchases the following capital assets for use in his catering business: New passenger automobile (September 30) $52,000 Baking equipment (June 30) 15,600 Assume that William decides to use the election to expense on the baking equipment (and has adequate taxable income to cover the deduction) but not on the automobile (which has a 5-year recovery period), and he also uses the MACRS accelerated method to calculate depreciation but elects out of bonus depreciation. Assume he has adequate taxable income. Click here to access the depreciation table and click here to access the annual automobile depreciation limitations. Calculate William's maximum depreciation deduction for 2021, assuming he uses the automobile 100 percent in his business. ANNUAL AUTOMOBILE DEPRECIATION LIMITATIONS Year of Use Year 1 Year 2 Year 3 Year 4 (and subsequent years until fully depreciated) Additional bonus depreciation of $8,000 is included in this amount. 2021 Limits $18,200* 16,400 9,800 5,860 Recovery Year 15 3 4 6 8 9 10 11 12 13 14 15 16 17 18 19 20 21 3-Year (200 % DB) 33.33 44.45 14.81 7.41 5-Year (200% DB) 20.00 32.00 19.20 11.52 11.52 5.76 17 Year (200% DB) 14.29 24.49 17.49 12.49 8.93. 8.92 8.93 4.46 10 Year: (200% DB) 10.00 18.00 14.40 11.52 9.22 7.37 6.55 6.55 6.56 6.55 3.28 15 Year (150% DB) 5.00 9.50 8.55 7.70 6.93 6.23 5.90 5.90 5.91 5.90 5.91 5.90 5.91 5.90 5.91 2.95 20 Year (150% DB) 3.750 7.219 6.677 6.177 5.713 5.285 4.888 4.522 4.462. 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 2.231