Answered step by step

Verified Expert Solution

Question

1 Approved Answer

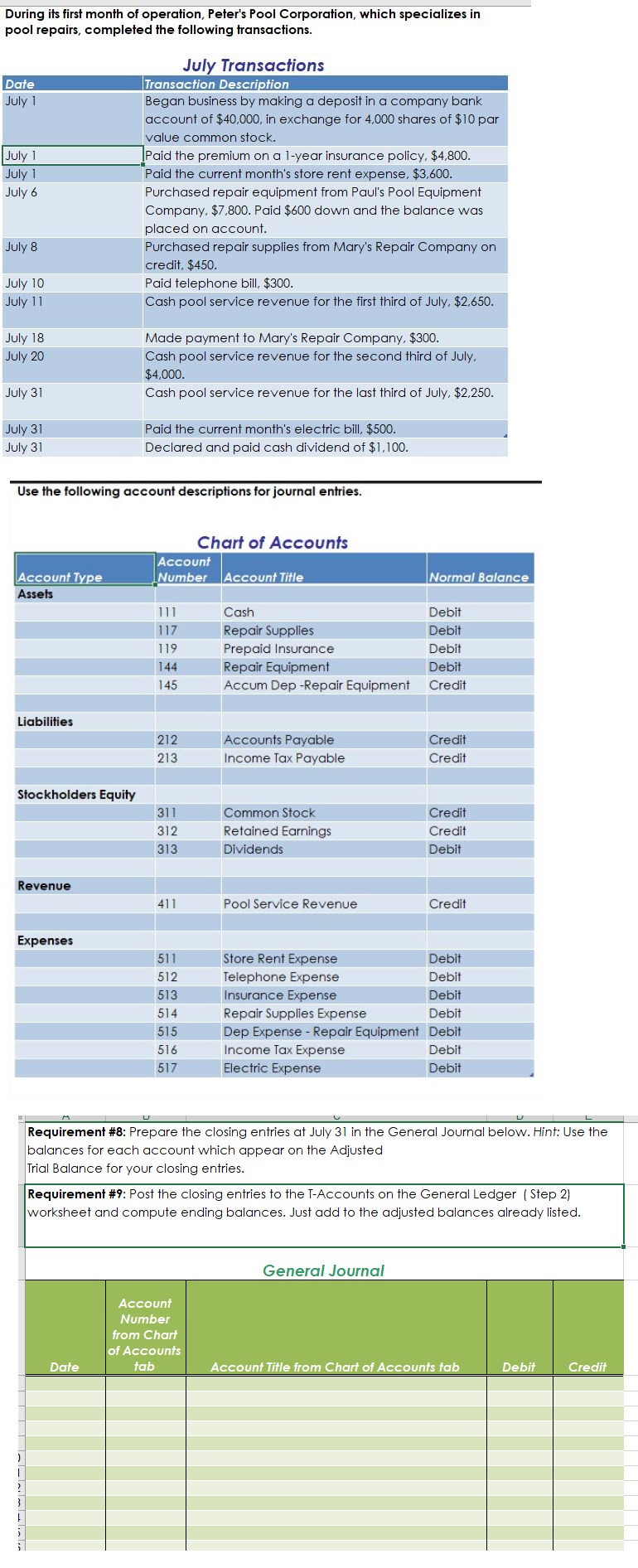

During its first month of operation, Peter's Pool Corporation, which specializes in pool repairs, completed the following transactions. Date July 1 July 1 July

During its first month of operation, Peter's Pool Corporation, which specializes in pool repairs, completed the following transactions. Date July 1 July 1 July 1 July 6 July 8 July 10 July 11 July 18 July 20 July 31 July 31 July 31 July Transactions Transaction Description Began business by making a deposit in a company bank account of $40,000, in exchange for 4,000 shares of $10 par value common stock. Paid the premium on a 1-year insurance policy, $4,800. Paid the current month's store rent expense, $3,600. Purchased repair equipment from Paul's Pool Equipment Company, $7,800. Paid $600 down and the balance was placed on account. Purchased repair supplies from Mary's Repair Company on credit, $450. Paid telephone bill, $300. Cash pool service revenue for the first third of July, $2,650. Made payment to Mary's Repair Company, $300. Cash pool service revenue for the second third of July, $4,000. Cash pool service revenue for the last third of July, $2,250. Paid the current month's electric bill, $500. Declared and paid cash dividend of $1,100. Use the following account descriptions for journal entries. Chart of Accounts Account Account Type Number Account Title Normal Balance Assets 111 Cash Debit 117 Repair Supplies Debit 119 Prepaid Insurance Debit 144 Repair Equipment Debit 145 Accum Dep-Repair Equipment Credit Liabilities 212 Accounts Payable Credit 213 Income Tax Payable Credit Stockholders Equity 311 Common Stock Credit 312 Retained Earnings Credit 313 Dividends Debit Revenue 411 Pool Service Revenue Credit Expenses 511 Store Rent Expense Debit 512 Telephone Expense Debit 513 Insurance Expense Debit 514 Repair Supplies Expense Debit 515 Dep Expense - Repair Equipment Debit 516 Income Tax Expense Debit 517 Electric Expense Debit ? 3 Requirement #8: Prepare the closing entries at July 31 in the General Journal below. Hint: Use the balances for each account which appear on the Adjusted Trial Balance for your closing entries. Requirement #9: Post the closing entries to the T-Accounts on the General Ledger (Step 2) worksheet and compute ending balances. Just add to the adjusted balances already listed. Date Account Number from Chart of Accounts tab General Journal Account Title from Chart of Accounts tab Debit Credit

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Libby, Short

6th Edition

978-0071284714, 9780077300333, 71284710, 77300335, 978-0073526881