Answered step by step

Verified Expert Solution

Question

1 Approved Answer

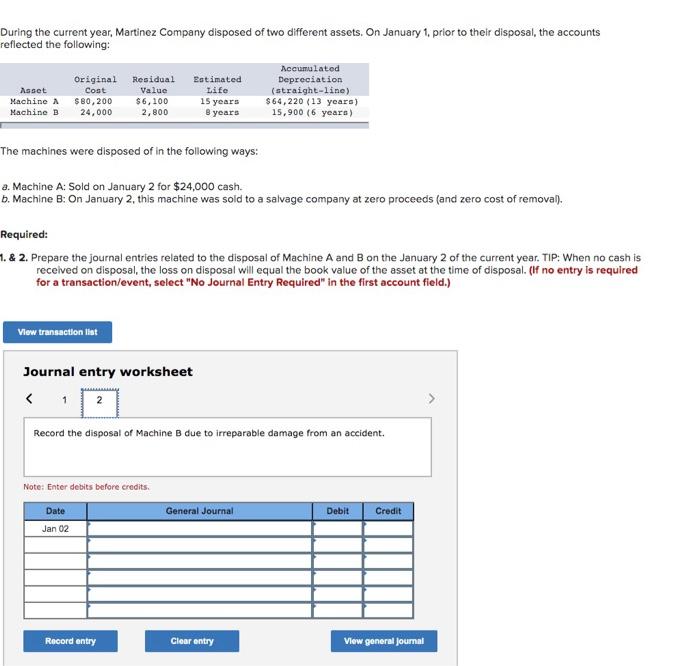

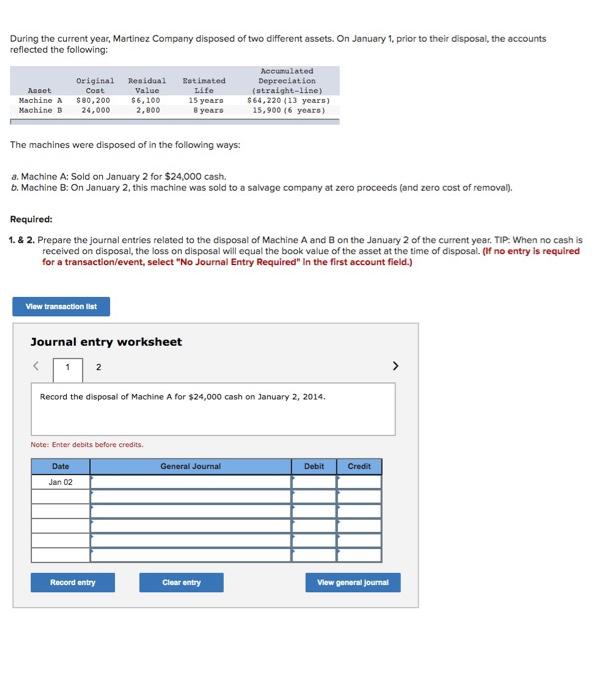

During the current year, Martinez Company disposed of two different assets. On January 1, prior to their disposal, the accounts reflected the following: Accumulated Original

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Trainer 3 0 Online For Albright/Ingram/Hills Managerial Accounting Information For Decisions

Authors: Thomas L. Albright, Robert W. Ingram, John S. Hill

4th Edition

0324233388, 978-0324233384