Answered step by step

Verified Expert Solution

Question

1 Approved Answer

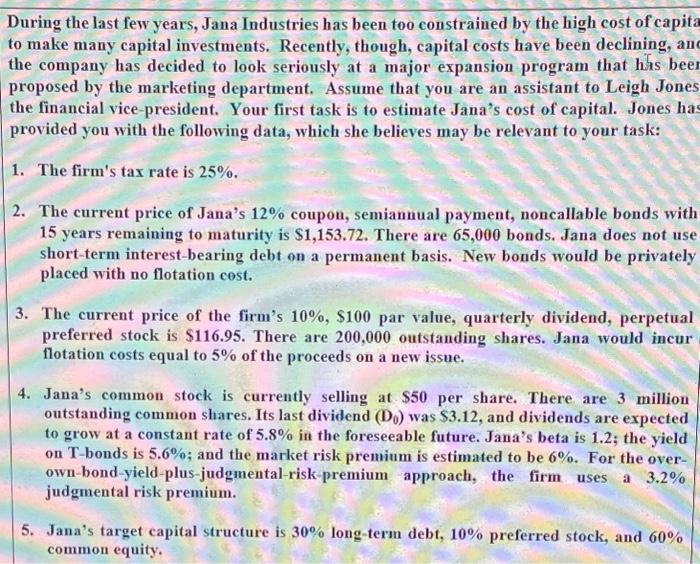

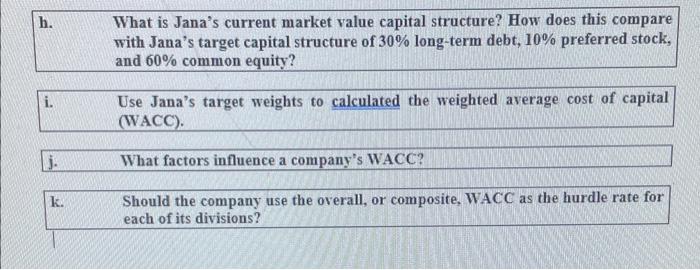

During the last few years, Jana Industries has been too constrained by the high cost of capita to make many capital investments. Recently, though, capital

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Portfolio Performance Measurement And Benchmarking

Authors: Jon Christopherson, David Carino, Wayne Ferson

1st Edition

0071496653, 978-0071496650