Answered step by step

Verified Expert Solution

Question

1 Approved Answer

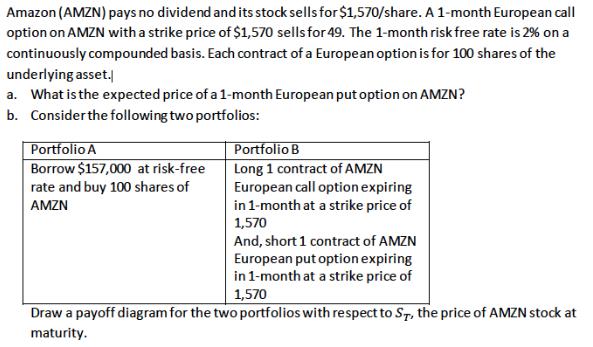

Amazon (AMZN) pays no dividend and its stock sells for $1,570/share. A 1-month European call option on AMZN with a strike price of $1,570

Amazon (AMZN) pays no dividend and its stock sells for $1,570/share. A 1-month European call option on AMZN with a strike price of $1,570 sells for 49. The 1-month risk free rate is 2% on a continuously compounded basis. Each contract of a European option is for 100 shares of the underlying asset. a. What is the expected price of a 1-month European put option on AMZN? b. Consider the following two portfolios: Portfolio A Borrow $157,000 at risk-free rate and buy 100 shares of AMZN Portfolio B Long 1 contract of AMZN European call option expiring in 1-month at a strike price of 1,570 And, short 1 contract of AMZN European put option expiring in 1-month at a strike price of 1,570 Draw a payoff diagram for the two portfolios with respect to ST, the price of AMZN stock at maturity.

Step by Step Solution

★★★★★

3.35 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

Answer Calculation of Price of Put optionP0 Here Put Call parity concept shall ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Statistical Quality Control

Authors: Douglas C Montgomery

7th Edition

1118146816, 978-1-118-3225, 978-1118146811