Answered step by step

Verified Expert Solution

Question

1 Approved Answer

(e) Consider creating a portfolio of three assets denoted A, B and C. Assume the following information [0.10 0.30 0.10 = 0.04,= 0.30 0.15

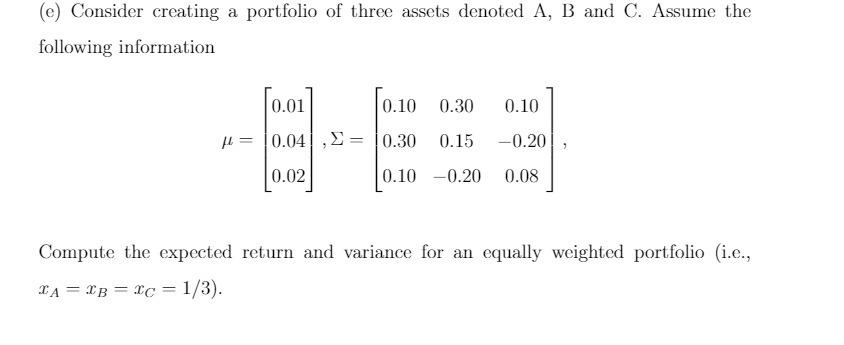

(e) Consider creating a portfolio of three assets denoted A, B and C. Assume the following information [0.10 0.30 0.10 = 0.04,= 0.30 0.15 -0.20 0.10 -0.20 0.08 0.01 0.02 Compute the expected return and variance for an equally weighted portfolio (i.e., TA=TB = IC = 1/3).

Step by Step Solution

★★★★★

3.47 Rating (150 Votes )

There are 3 Steps involved in it

Step: 1

To compute the expected return and variance for an equally weighted portfolio with three assets ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Basic Statistics

Authors: Charles Henry Brase, Corrinne Pellillo Brase

6th Edition

978-1133525097, 1133525091, 1111827028, 978-1133110316, 1133110312, 978-1111827021