Answered step by step

Verified Expert Solution

Question

1 Approved Answer

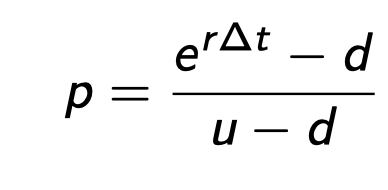

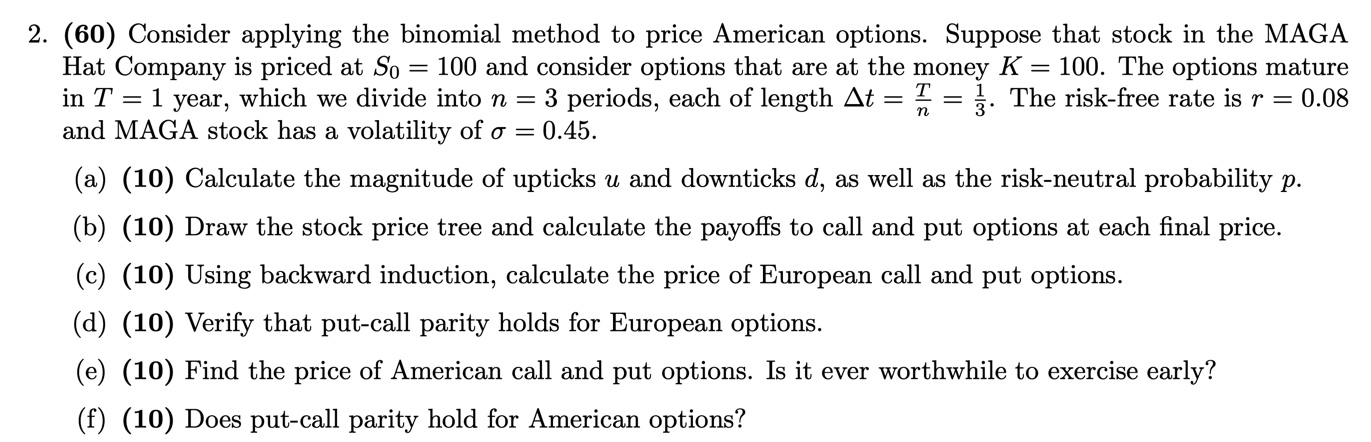

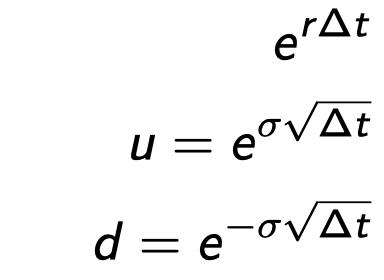

e rAt p = U - d2. (60) Consider applying the binomial method to price American options. Suppose that stock in the MAGA Hat Company

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Nonlinear Systems And Their Remarkable Mathematical Structures Volume 3, Contributions From China

Authors: Norbert Euler, Da jun Zhang

1st Edition

1000423301, 9781000423303