Answered step by step

Verified Expert Solution

Question

1 Approved Answer

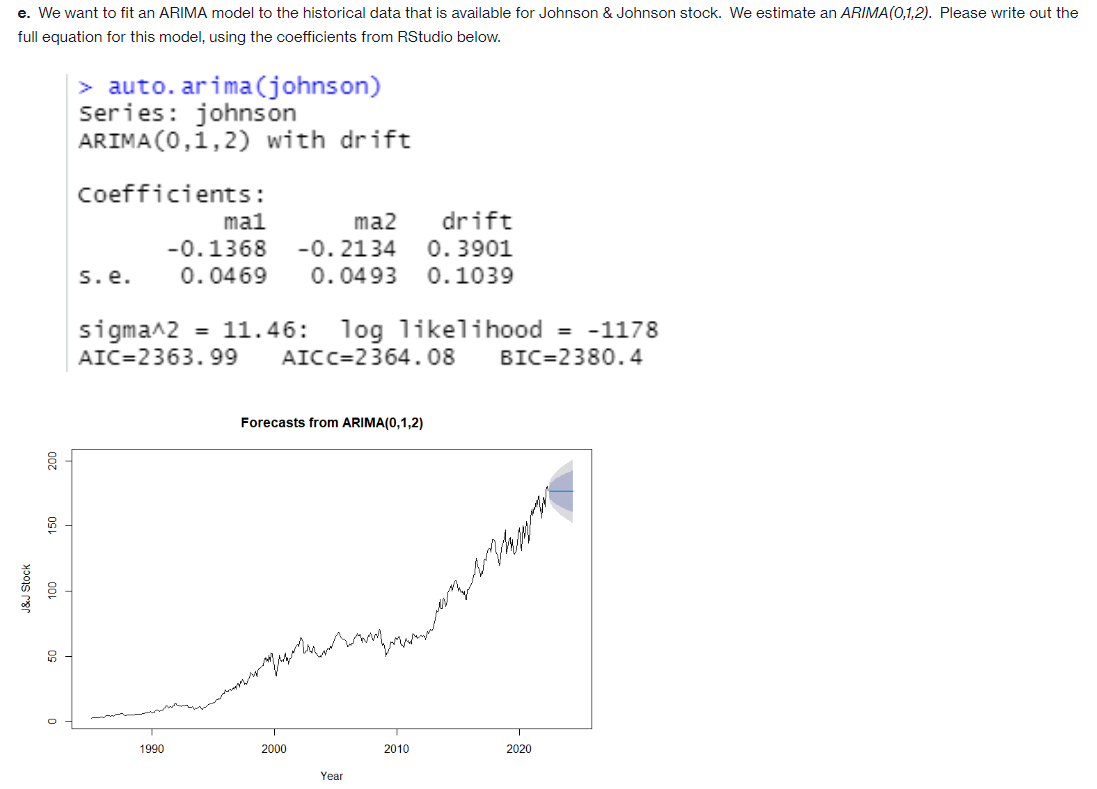

e. We want to fit an ARIMA model to the historical data that is available for Johnson & Johnson stock. We estimate an ARIMA(0,1,2). Please

e. We want to fit an ARIMA model to the historical data that is available for Johnson \& Johnson stock. We estimate an ARIMA(0,1,2). Please write out the full equation for this model, using the coefficients from RStudio below. > auto. arima(johnson) series: johnson ARIMA(0,1,2) with drift Coefficients: ma1 ma2 drift 0.13680.21340.3901 s.e. 0.04690.04930.1039 sigma^2 =11.46: log likelihood =1178 AIC =2363.99 AIC =2364.08 BIC =2380.4

e. We want to fit an ARIMA model to the historical data that is available for Johnson \& Johnson stock. We estimate an ARIMA(0,1,2). Please write out the full equation for this model, using the coefficients from RStudio below. > auto. arima(johnson) series: johnson ARIMA(0,1,2) with drift Coefficients: ma1 ma2 drift 0.13680.21340.3901 s.e. 0.04690.04930.1039 sigma^2 =11.46: log likelihood =1178 AIC =2363.99 AIC =2364.08 BIC =2380.4 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

New Issues In Financial Institutions Management

Authors: F Fiordelisi, P Molyneux, D Previati

2010th Edition

0230278108, 978-0230278103