Question

e. Your client has decided that the risk of the bond portfolio is acceptable and wishes to leave it as it is. Now your client

e. Your client has decided that the risk of the bond portfolio is acceptable and wishes to leave it as it is. Now your client has asked you to use historical returns to estimate the standard deviation of Blandy's stock returns. (Note: Many analysts use 4 to 5 years of monthly returns to estimate risk and many use 52 weeks of weekly returns; some even use a year or less of daily returns. For the sake of simplicity use Blandy's ten annual returns.) f. Your client is shocked at how much risk Blandy stock has and would like to reduce the level of risk. You suggest that the client sell 25% of the Blandy stock and create a portfolio with 75% Blandy stock and 25% in the high risk Gourmange stock. How do you suppose the client will react to replacing some of the Blandy stock with high risk stock? Show the client what the proposed portfolio return would have been in each of year of the sample. Then calculate the average return and standard deviation using the portfolio's annual returns. How does the risk of this two-stock portfolio compare with the risk of the individual stocks if they were held in isolation? g. Explain correlation to your client. Calculate the estimated correlation between Blandy and Gourmange. Does this explain why the portfolio standard deviation was less than Blandy's standard deviation? h. Suppose an investor starts with a portfolio consisting of one randomly selected stock. As more and more randomly selected stocks are added to the portfolio, what happens to the portfolio's risk?

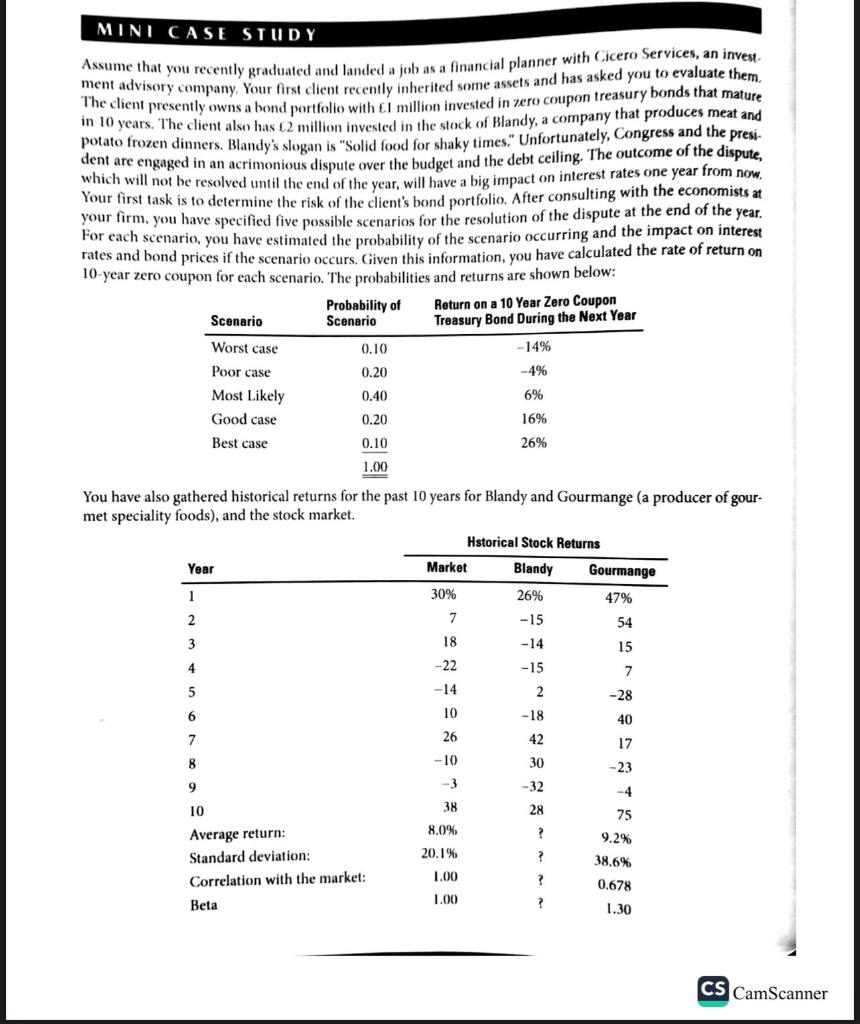

MINI CASE STIIDY Assume that you recently graduated and landed a job as a financial planner with Cicero Services, an invest. ment advisory company. Your first client recently inherited some assets and has asked you to evaluate them. The client presently owns a bond portfolio with 1 million invested in zero coupon treasury bonds that mature in 10 years. The client also has 2 million invested in the stock of Blandy, a company that produces meat and potato frozen dinners. Blandy's slogan is "Solid food for shaky times." Unfortunately, Congress and the president are engaged in an acrimonious dispute over the budget and the debt ceiling. The outcome of the dispute, which will not be resolved until the end of the year, will have a big impact on interest rates one year from now. Your first task is to determine the risk of the client's bond portfolio. After consulting with the economists at your firm, you have specified five possible scenarios for the resolution of the dispute at the end of the year. For each scenario, you have estimated the probability of the scenario occurring and the impact on interest rates and bond prices if the scenario occurs. Given this information, you have calculated the rate of return on 10-year zero coupon for each scenario. The probabilities and returns are shown below: You have also gathered historical returns for the past 10 years for Blandy and Gourmange (a producer of gourmet speciality foods), and the stock marketStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Oxford Handbook Of Sovereign Wealth Funds

Authors: Douglas J. Cumming, Geoffrey Wood, Igor Filatotchev, Juliane Reinecke

1st Edition

0198754809, 978-0198754800