Answered step by step

Verified Expert Solution

Question

1 Approved Answer

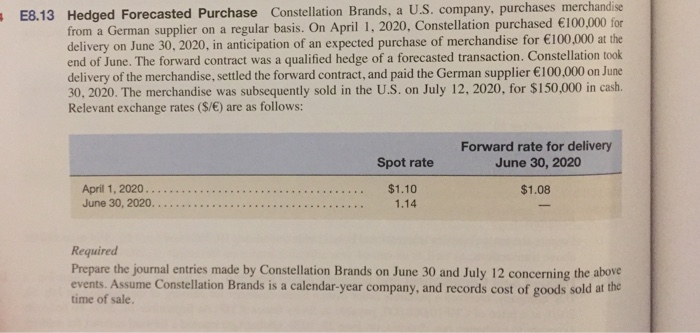

E8.13 Hedged Forecasted Purchase Constellation Brands, a U.S. company, purchases merchandise from a German supplier on a regular basis. On April 1, 2020, Constellation purchased

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting A Smart Approach

Authors: Mary Carey, Cathy Knowles

4th Edition

0198844808, 9780198844808