Question: ead the Harvard case study on Procter and Gamble. Then, answer the following questions. 1. What is business analytics? Why is it important to make

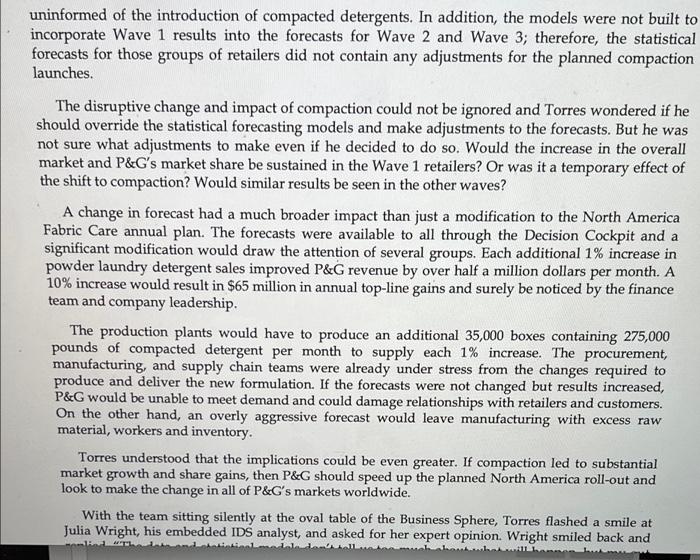

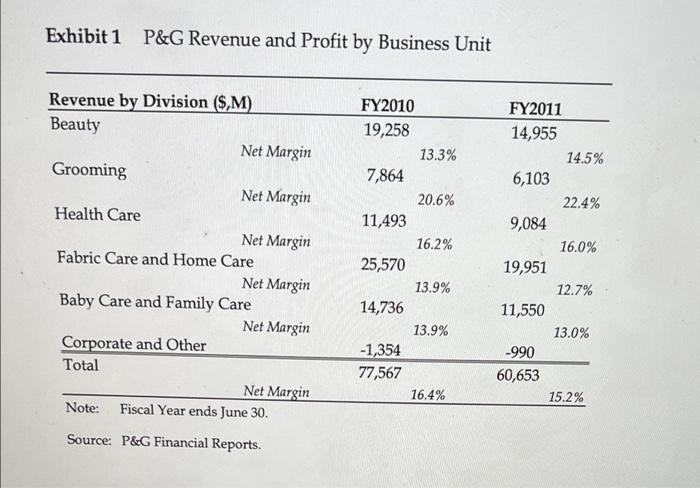

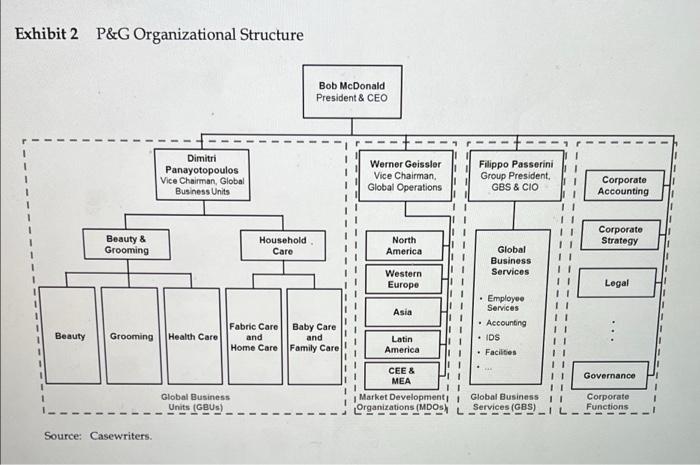

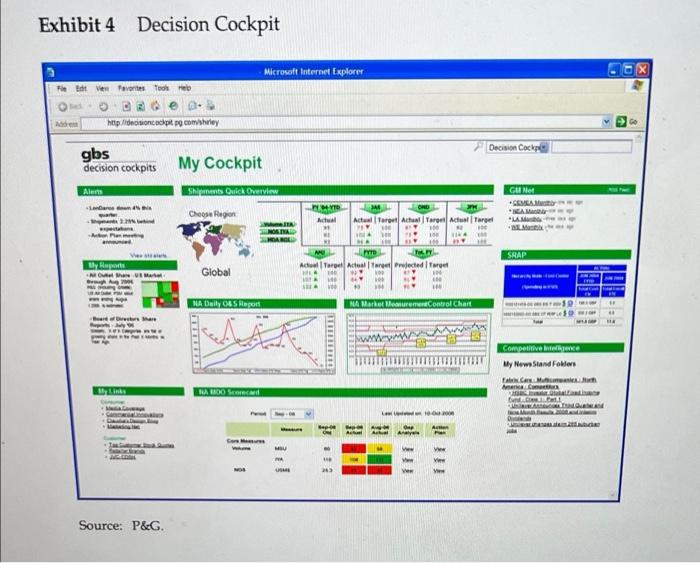

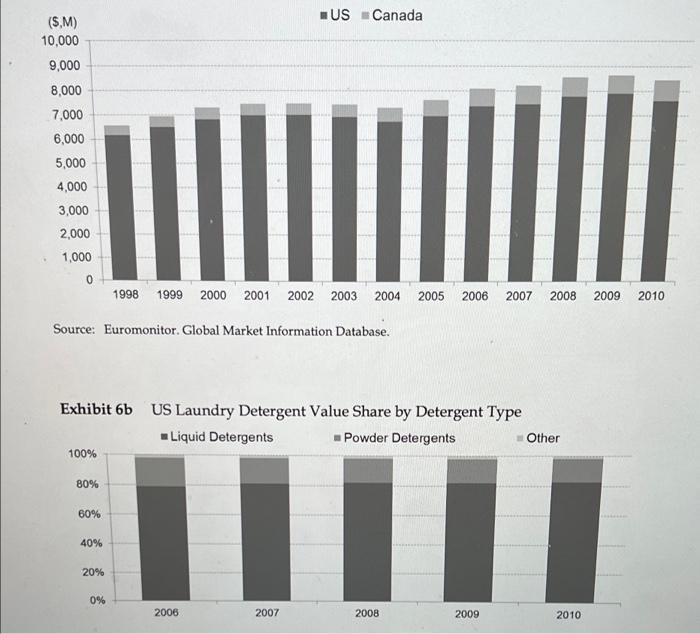

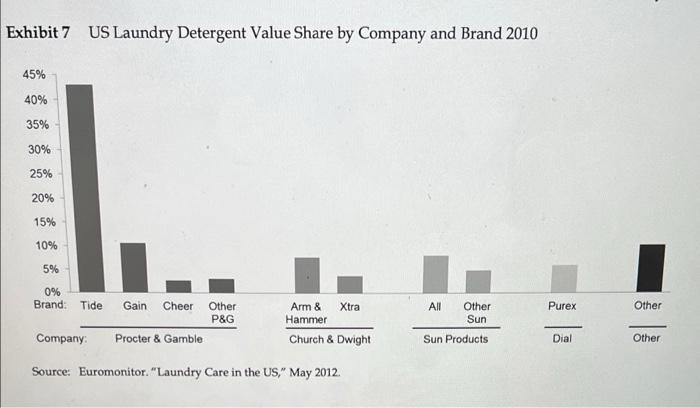

ead the Harvard case study on Procter and Gamble. Then, answer the following questions. 1. What is business analytics? Why is it important to make real-time decisions at P&G? What are the benefits of centralizing the data and analytics activities? 2. What are the functions of Information and Decision Solution (IDS) at P&G? Discuss how the decision cockpit developed by IDS in P&G works. 3. Discuss how business analytics affects P&G's corporate culture, forecasting, and supply chain performance. 4. What is the role of analytics software in organizations? What difficulties are associated with their development and implementation? 5. How does P&G management ensure everyone up and down the chain uses real-time data? 6. Has P&G been successful in using analytics so far? Why? What challenges lie ahead? 7. Should Torres override the statistical models and increase the forecasts? pm EST Alan Torres, vice-president of North America Fabric Care at Procter & Gamble (P&G), watched and listened as his embedded IDS analyst, Julia Wright, graphically displayed the initial results. Torres leaned back to take in the complete set of 12 graphs and charts on the massive 8-foot by 32- foot screens in a specialized meeting room called a Business Sphere at P&G's headquarters in Cincinnati, Ohio. The company had introduced a more concentrated, also called compacted, powder laundry detergent in Target stores at the end of February 2011 and results from the first two months were better than anyone had expected. Over the previous 8 years, Filippo Passerini, Group President of P&G's Global Business Services (GBS) organization and Chief Information Officer (CIO), had led the development of a series of systems and processes that enabled and emphasized the use of up-to-date data and advanced analytics to drive decision making throughout the company. Through these efforts, Torres and his team were able to see the results of this first wave of compaction as they became available. Data collected by P&G was seamlessly integrated so that Torres and Wright could simply click on higher level data to drill down and view performance by brand, initiative, retailer, and, in some cases, individual store. In addition, statistical forecasts for the next twelve months were automatically updated and made available. Equipped with these tools, Wright led Torres through a series of charts and graphs that showed a three percent increase in the overall detergent category in the stores where the compacted detergents were introduced. Torres had anticipated that the compacted format would provide a slight boost to the mature $8.5 billion North America laundry detergent market, where growth rarely exceeded 2%.1 But the market had contracted by 2% in 2010 after a gain of just 1% in 2009, so growth of over 2% was beyond all expectations. Even more surprising, P&G's powder detergent sales jumped 12% as the company's market leading brands, including Tide, Gain, and Cheer, gained market share. P&G already held more than a 50% share of the North America laundry detergent market that generated over $4 billion in revenue for the company in 2010.2 Compacted detergents were set to be introduced throughout the rest of North America in the coming months and Torres was cautiously optimistic about the impact they would have on the overall market and on P&G sales. The statistical models used to produce market size and P&G sales forecasts did not fully account for the market disruption caused by the introduction of compacted As Torres stared at the array of charts on the colossal screens of the Business Sphere, he wondered whether he should override the statistical models and increase the forecasts. Procter & Gamble Overview and Organization Pressured to join their businesses by their mutual father-in-law, William Procter and James Gamble partnered to form The Procter & Gamble Company in 1837. The Cincinnati, Ohio based company quickly became a leading supplier of candles and soap, achieving sales of $1 million by 1859. Three years after the introduction of Ivory brand soap, the company decided to launch the first ever national advertising campaign that directly targeted consumers.3 Since then, P&G has focused on innovation and branding to become the world's largest consumer packaged goods company. By 2011, P&G marketed personal care and cleaning products in 180 countries that were ultimately used by 4.2 billion people around the world. It was estimated that 98% of all North American households contained at least one P&G product.5 The company marketed approximately 300 brands, 25 of which generated over $1 billion in annual sales, including Always, Bounty, Charmin, Crest, Duracell, Gillette, Head & Shoulders, Olay, Pampers and Pantene. In total, P&G was on track to amass sales of over $80 billion in fiscal year 2011 (ended June 30, 2011). (See Exhibit 1 for company revenue and profitability) Organizational Structure In an effort to spur profitable growth, P&G embarked on an aggressive two year-long corporate restructuring in 1999. The initiative, called Organization 2005, aimed to reorganize the many small, relatively independent businesses that had been loosely organized by region. By configuring as global product line-focused business units, the company hoped to more fully take advantage of P&G's established brands, tremendous scale, and worldwide presence. Critically, the new structure would allow P&G to more effectively develop and implement innovations on a global scale. The 1999 annual report described Organization 2005 as a "realignment of the organization structure, work processes and culture designed to accelerate growth by streamlining management decision-making, manufacturing and other work processes to increase the Company's ability to innovate and bring estructuring in 1999. The initiative, called Organization 2005, aimed to reorganize the many small elatively independent businesses that had been loosely organized by region. By configuring as global product line-focused business units, the company hoped to more fully take advantage of P&G's established brands, tremendous scale, and worldwide presence. Critically, the new structure would allow P&G to more effectively develop and implement innovations on a global scale. The 1999 annual report described Organization 2005 as a "realignment of the organization structure, work processes and culture designed to accelerate growth by streamlining management decision-making, manufacturing and other work processes to increase the Company's ability to innovate and bring initiatives to global markets more quickly." Following the restructuring, P&G's 129,000 employees were organized into four independent global organizations: (Exhibit 2) Global Business Units (GBUS) The primary driver of commercial activity at P&G was the GBU. The product line-based GBUS had primary responsibility for developing strategy, building brands, manufacturing products, developing and bringing to market innovations, contending with competitors, and delivering profits. By centralizing at the global level, GBUS were better able to standardize manufacturing processes, coordinate marketing activities, build global brands, identify significant innovations and bring new products to market quickly. As of 2011, P&G consisted of GBUS covering five product-based segments: Beauty, Grooming, Health Care, Fabric Care and Home Care, and Baby Care and Family Care. Market Development Organizations (MDOS) By maintaining a local presence, the MDOS provided P&G with the knowledge and relationships required to compete locally in each geographic region. MDOS were responsible for understanding the preferences of local consumers and retailers so that the global initiatives and brands of the GBUS could be tailored for local markets. In addition, 2 having leaders in each market enabled the company to identify trends in local markets faster. The MDOS were organized into five geographies: North America, Western Europe, Asia, Latin America, and Central & Eastern Europe, Middle East and Africa. Global Business Services (GBS) Business support services including accounting, payroll, employee services, information technology, order management, and logistics were moved into the newly formed GBS. Prior to the reorganization, these functions were duplicated in each unit. In centralizing these activities, P&G looked to gain efficiencies through scale, standardization of shared services and the transfer of best practices across the organization. Corporate Functions Corporate accounting, legal, communications, governance, corporate strategy, and other corporate support functions were provided by a lean Corporate Functions group. GBS GBS functioned as a service to the GBUS and MDOS across P&G. As the company's back office, GBS looked to provide the high quality services required by its internal customers "at lowest cost and with minimal capital investment."8 GBS had to break even each year, and, therefore, could only supply services that were valued by the GBUS and MDOS. In total, GBS provided more than 170 shared services and solutions to the various groups in the organization." (Exhibit 3) In 2003, Passerini was put in charge of GBS. A native of Italy, Passerini earned a doctorate in statistics and operations research from the University of Rome. He had served many roles across several geographies and product lines since joining P&G in 1981 and he understood both the technical demands of GBS and the needs of a diverse set of P&G business units. Shortly after joining GBS, Passerini embarked on the second phase of the reorganization of shared services at P&G. The company looked to achieve even greater scale efficiencies by leveraging external partners to deliver many of the services initially centralized into GBS. In 2003, P&G entered into contracts worth $4.2 billion for several activities where Passerini felt that the company could gain efficiencies without sacrificing strategic capabilities.10 Initially GBS planned to utilize third party providers for all of P&G's IT capabilities. But managers realized that it would be difficult for an outeido antity to work closely with P&C avantivon the number of services offered and improving service levels, which demonstrated the increased valu that the GBUS and MDOs placed on the services provided by GBS. Analytics at P&G We see business intelligence as a key way to drive innovation, fueled by productivity, in everything we do. To do this, we must move business intelligence from the periphery of operations to the center of how business. gets done. - Bob McDonald, President, CEO, and Chairman, P&G Initially, P&G's management felt that IT could support data analysis throughout the company by acting as a central repository for data and by providing software tools to aid analysts. Passerini, however, envisioned a much larger role. IDS, he proposed, would support business leaders by performing much of the analytics and by making data as accessible as possible. The P&G website described the division's broad role, "IDS stretches far beyond the traditional aspects of 'hardware and software. Instead, we are a key business enabler that advances technology tools, strategic development, collaboration, and decision making."14 By the end of the decade, Passerini felt that P&G had the systems, data, and people within IDS to change the process of managerial decision making at the company. Fortunately for Passerini and IDS, in July 2009, Bob McDonald became the President and CEO, and later Chairman of the Board, of P&G. Having studied operations research, computer science, and engineering at West Point, McDonald shared Passerini's enthusiasm for data and analytics. McDonald, who had previously served as Chief Operations Officer and Vice-Chairman, Global Operations, had long understood that the analytics capabilities of IDS were critical to P&G's continued success. The Global Operations section of the 2005 annual report, for which McDonald was responsible, stated that "GBS provides P&G with an often-unseen competitive advantage. GBS combines information management and analysis capabilities to take P&G's use of information to a far more strategic level. These efforts help P&G's Market Development Organizations and Global Business Units make better, smarter, real-time business decisions."15 When McDonald became CEO, the effective use of information and technology at P&G became business collected and stored data in independent systems. By bringing together the data collectic activities, IDS was able to establish standards for data type and quality. Additionally, aggregatir and comparing data across product lines and regions became significantly less complicated with th data stored in standard formats in the central data warehouse. Over time, managers found that the single, company-wide database played a much more strategic role in aiding decision making by serving as the "one truth" for the entire corporation. As Passerini explained, "Instead of spending our time debating the data, we eliminate the need for those discussions. The data is the data, and leaders can spend their time concentrating on the business and the decisions that need to be made to move the business--instead of which set of data points is correct. This speeds decision-making and ultimately improves time to market."18 IDS automated the generation of many reports that were used across multiple business units. In addition to simplifying the task of retrieving data and performing some basic analyses, the reports served to standardize the way data was visualized across the company. The same types of charts and graphics used to track sales and market share of Old Spice deodorant in the US were also used to monitor lams dog food in the Philippines and Oral-B toothbrushes in Brazil. With consistent visuals, analysts and managers from one unit could step into a role, or even a meeting, with a different product or region and quickly understand the situation. The centralized IDS team also acted as a hub for sharing analytic techniques and ideas. McDonald explained that prior to the integration of analytics as a centralized service there were "5,000 people in the company who used to do demand planning. So, each one would have their own spreadsheet. And they would try to plan demand based upon the inputs that they saw. Of course, they all had their own technique."19 IDS served as a platform for sharing best practices, which improved the overall quality of analytics at P&G. Data and Enabling Technologies As a service, IDS had to respond to the needs of the GBUS and MDOS. Any unit within P&G was able to request that IDS provide a new service, but IDS focused on building out scaled solutions that could be performed centrally and leveraged in multiple markets. arop razors in Austrana, the "what," she could quickly understand the "why" by looking at sales by city or retailer, shipments, prices, promotions and competitor actions. With a few clicks of a mouse, or touches on her tablet computer, she could check if the overall market dropped or just the P&G brand. She could also check if a particular retailer decreased orders, or if customers just purchased lower quantities. Just as easily, she could investigate if there were any changes in pricing, if a competitor came out with a new product or if a competitor launched a new marketing campaign. With much less time needed to identify the "what" and understand the "why," leaders were able to quickly move to the crucial decision making of "how" to fix the problem or maintain improved performance. IDS worked with P&G business units, suppliers, customers and external vendors, such as Nielsen and IRI, to collect data about the "what," "why" and "how." Passerini and his team continuously looked for ways of improving the data available both in type and frequency. To collect data from social media, IDS developed Consumer Pulse, which provided real-time sentiment analysis for web buzz of each P&G brand. It leveraged best-in-class technology, including approaches used by the intelligence community to monitor terrorism. For management teams, P&G developed a patent-pending physical environment for information- based decision-making called the Business Sphere. (Exhibit 5) The meeting room, located adjacent to the executive offices at P&G's headquarters in Cincinnati, was spherical in shape with a conference table in the center. What made the Business Sphere unique was the computing and network capabilities to bring data, images, voice, and videoconferences into the room. Most noticeable was the surrounding set of two oversize 8-foot by 32-foot screens to display visualizations of data and analyses. Drawing on the 200 terabytes of data in P&G's data warehouse, leaders could drill down into the data "on-the-spot" using color coded charts and displays to visualize all the relevant information at once. 20 Passerini explained that the Business Sphere provided an environment that was "physically surrounding business leaders with the data they need to make actionable decisions. The visualization of the data makes it easy to focus on the exceptions and realize business opportunities and where interventions are necessary."21 Leadership teams would typically gather in the Business Sphere at regular intervals, generally weekly or monthly, to review product and market performance for the previous periods and make decisions about how to proceed going forward. McDonald, for example, held his Monday morning global meetings of direct reports in the Business Sphere. They could also be used for ad hoc meetings The initial forecasting models only provided point forecasts, single numbers for each time period that represented the most likely outcome. To give managers a more complete picture of the potential result, the team decided to provide probabilistic ranges that showed the spread of prospective outcomes. The forecasting team ran thousands of virtual simulations of how the future might unfold and tracked each to determine the likelihood of being, for example, 10% above the forecast. The ranges alerted managers to markets with higher uncertainty and variability, shifting the focus from large but stable markets to those that warranted increased attention. P&G employed two types of statistical models for forecasting. The first type, generally time series- based forecasting models, produced the most accurate forecasts. These models constructed forecasts using previous results as well as macroeconomic conditions and other basic inputs. Although the outputs were precise, this set of models provided little insights as to why the outcome would occur. Propensity models, on the other hand, attempted to better understand the causes, or drivers, of the outcomes. By incorporating information on drivers such as new product introductions, marketing campaigns, and competitor actions, propensity models served as useful tools to measure the potential impact of management actions. The forecasts and ranges were extended to a set of seven "Business Sufficiency Models" developed by IDS in conjunction with senior executives. These models captured the most recent data and conducted a large number of simulations to provide leaders with a measure of the likelihood that the business would be able to deliver on previously set goals and targets. Areas that seemed unlikely to meet objectives were highlighted so that leaders could quickly move to explore actions of "how" to rectify the situation and alert other parts of the organization that may be impacted. Andy Walter, who headed the Business Intelligence area within P&G, explained the concept of Business Sufficiency Models: The concept of business sufficiency is that we commit to a performance goal, and the key question is whether I have sufficiency to deliver that goal. It may be a supply chain goal, a production goal, or a sales volume goal. We want to make sure that we have all the factors lined up to achieve it, and the models provide data on those factors. They are mostly backward-looking reports now, but in some areas we're producing forecasts and projections. With the seven models we cover about 90% of the information the company needs to run itself. obvious candidates. IDS embedded analysts within the business units, each dedicated to working alongside leaders and managers of a particular team on a daily basis. In some cases, the embedded IDS analyst was a member of the business unit's leadership team. The embedded IDS analyst role had multiple components. The analyst was responsible for bringing technology, visualization, and automated alerting functions to the business unit. They were responsible for integration across diverse data domains and models (as in the Korea Swiffer example above). They were required to develop analytical models driving forward-looking insights and simulations within and across the business domains they supported. And, they led market performance review meetings in the Business Spheres, guiding business unit managers and leaders through the "what" and the "why" and providing on-the-fly analysis of the "how" actions proposed. Guy Peri, a director in IDS who also headed P&G's analytical capabilities, noted that "GBSers are embedded into the business to understand where technology can help. We are business people first, then technology experts. We invest in the business needs and solutions, not technology."22 Successful performance in the role required a high level of business domain and technology understanding, as well as communication and leadership skills to engage with senior executives. Embedded analysts rotated through multiple business units to gain a broad understanding of the company's activities and needs. Some IDS analysts had "graduated" to become business leaders themselves. To help support these embedded IDS analysts, P&G created the Business Intelligence Analytics Service Line. The formal organization and "home" for these employees offered a challenging and rewarding career path for those IDS employees who were passionate about analytics. In addition, centralization provided the ability to drive scale and reapplication of analytic models, quickly reapplying proven techniques and processes globally. For example, an analytic model created in Singapore could potentially get scaled globally in 24 hours. Bob McDonald believed that the IDS talent was critical to the success of business intelligence at P&G. However, McDonald emphasized that it wasn't just IDS analysts who had to embrace analytics and data-based decision-making, but every manager at P&G. "I gather there are still some MBAs who believe that all the data work will be done for them by subordinates. That won't fly at P&G. It's every manager's job here to understand the nature of statistical forecasting and Monte Carlo simulation. You have to train them in the technology and techniques but you also have to train them in the To help support these embedded IDS analysts, P&G created the Business Intelligence Analytics Service Line. The formal organization and "home" for these employees offered a challenging and rewarding career path for those IDS employees who were passionate about analytics. In addition, centralization provided the ability to drive scale and reapplication of analytic models, quickly reapplying proven techniques and processes globally. For example, an analytic model created in Singapore could potentially get scaled globally in 24 hours. Bob McDonald believed that the IDS talent was critical to the success of business intelligence at P&G. However, McDonald emphasized that it wasn't just IDS analysts who had to embrace analytics and data-based decision-making, but every manager at P&G. "I gather there are still some MBAs who believe that all the data work will be done for them by subordinates. That won't fly at P&G. It's every manager's job here to understand the nature of statistical forecasting and Monte Carlo simulation. You have to train them in the technology and techniques, but you also have to train them in the transformation of their behavior," he noted. Impact on the Culture of P&G The various initiatives marked a dramatic cultural change in how P&G managed itself. Like many organizations, P&G had previously managed by a "preview" culture; any data could be previewed and digested by middle and business unit managers before business leaders saw it, and there was time to develop a plan to address any issues. The new approaches meant that information could be viewed at the same time by everyone. As one P&G president described the first time he worked in a Business Sphere, "My region was a big red spot on the map [indicating below-plan results]. It was like seeing your performance review in front of everyone in a 30-point font." Passerini hoped that real-time availability of information would lead to real-time decisions and actions by decision-makers and "radically increase the pace at which they do business."23 IDS had worked with human resources on how best to manage this cultural transformation, one leader at a time. The embedded IDS analysts provided coaching to the business leaders on how to use the new management tools effectively. The ability to easily access information, quickly identify areas in need of attention, and rapidly assess potential responses provided a new level of transparency to the organization. "What it does is, it allows you to flatten the organization...Everybody gets the same data at the same time," explained McDonald.24 Within a couple of years, the company reduced the number of reporting levels from seven to five and eliminated over 15% of senior management positions. Overall, a greater emphasis was placed on the tools and analytics provided by IDS as managers across the organization identified analytics as a means for gaining competitive advantage. The shift in strategic and cultural focus at P&G was summarized by Passerini, "It would be heretical in this company to say that data are more valuable than a brand, but it's the data sources that help create the brand and keep it dynamic. So those data sources are incredibly important."25 The North America Laundry Detergent Market For centuries, standard soaps had been used to clean clothing as well as hands and bodies. The original Ivory soap bars were designed to be broken in two, one half to be used for bathing and the other for cleaning soiled clothing and linens. In the 1930s, P&G introduced Dreft, the first synthetic detergent designed specifically for cleaning dirty laundry that was commercially available in North America. Synthetic laundry detergents quickly became the standard for laundry care and by 2010, the average American household used laundry detergents to clean approximately 600 loads of laundry each year.26 The North America laundry detergent sector was one of the largest and most important markets for P&G. The total market was estimated to be $8.5 billion at the retail level in 2010.27 By all measures, the laundry detergent market was mature and showed little growth. Penetration was very high as virtually all households in North America used laundry detergents. Growth was driven primarily by population increases, which averaged about 1% per year. The previous two years had been particularly challenging as annual market growth was 1.1% and -2.2% in 2009 and 2010, respectively. Overall, the market grew with an average annual rate of 1.5% between 2000 and 2010.28 During that span, the gradual change in consumer preference from powder detergents to liquid detergents continued and, by 2010, powders represented just 15% of the market. As a result, the $1.3 billion nowder laundry detergent market in North America cos if to worked with manufacturers to find ways to deliver the same cleaning power in smaller and lighter forms. Increasing the concentration level of detergents appealed to both producers and consumers as well. Producers would require less packaging materials and would save significantly on transportation and warehousing costs. Consumers would be better served with a product that was easier to carry and maneuver. In addition, the reduction in packaging, water usage, and transportation would be beneficial to the environment. Compacting powder laundry detergents required more than just increasing concentration by packaging the product more densely in each box. A complete reformulation of the cleansing compounds that made up the detergent was needed to achieve the same cleaning power with a smaller amount of detergent. And with many variants, such as detergents with added stain removers and detergents designed for high efficiency washing machines, the reformulation of a complete line of detergents was a challenging and time consuming undertaking. Although the benefits to all parties were quite clear, most manufacturers hesitated in bringing compacted products to market. Many worried that consumers would not believe that the smaller doses would be as effective in cleaning laundry. P&G North America Compaction Roll Out In September 2010, after years of development, P&G executives decided to introduce 1/3 compacted powder laundry detergents in the following year. Torres elected to stop producing the standard formulation and to supply all P&G brands and varieties in compacted form only. The compacted products were branded "Ultra" and prices were adjusted so that the consumer cost per wash-load remained about the same. A 56 ounce carton of the new Ultra Tide was 20% lighter than a 70 ounce box of the standard non-compacted Tide and was 33% smaller in size, but both would wash 40 loads of laundry. (Exhibit 8) Torres and his team did not anticipate that the introduction of compacted products would have any significant impact on overall market growth, since consumers would still wash the same number P&G North America Compaction Roll Out In September 2010, after years of development, P&G executives decided to introduce 1/3 compacted powder laundry detergents in the following year. Torres elected to stop producing the standard formulation and to supply all P&G brands and varieties in compacted form only. The compacted products were branded "Ultra" and prices were adjusted so that the consumer cost per wash-load remained about the same. A 56 ounce carton of the new Ultra Tide was 20% lighter than a 70 ounce box of the standard non-compacted Tide and was 33% smaller in size, but both would wash 40 loads of laundry. (Exhibit 8) Torres and his team did not anticipate that the introduction of compacted products would have any significant impact on overall market growth, since consumers would still wash the same number of loads. There was some debate around the way customers would respond to the compacted detergents. Customers that were skeptical of the compacted detergent's cleaning ability could switch to competitor products that were not compacted. On the other hand, other customers might find compacted products more convenient and environmentally-friendly and increasingly choose the concentrated P&G products. The team planned a large marketing effort to help consumers better understand the change to compacted powder laundry detergents. To measure consumer response to the new formulations, Cedar Rapids, Iowa served as a test market for the compacted products in the winter of 2010. All P&G powder laundry detergents were replaced with the compacted varieties in the city of a couple of hundred thousand people where no other competitors offered concentrated formulations. Consumers seemed comfortable with the shift to the concentrated detergents and, during the two-month trial, P&G saw a modest increase in powder detergent sales of just under 3%. In order to produce the compacted detergents, all of the powder laundry detergent manufacturing facilities spread out across North America had to be reconfigured. Each plant would shut down for a few weeks while the production equipment was updated at a cost of hundreds of thousands of dollars per facility. Once converted, the plants would no longer be able to supply non-compacted detergents. To ease the changeover, Torres planned to introduce the compacted detergents in three waves. In Wave 1, compacted detergents were to be released to Target and a few other selected retailers in February 2011. Next, Wave 2 would bring compacted detergents to most of the major discount retailers, supermarkets and online retailers beginning June 2011. Finally, the remaining retail and distribution channels would be converted to compacted detergents in August 2011 in Wave 3. Wave 1 In February 2011, P&G embarked on Wave 1 of the compaction roll-out. The company switched over a couple of production facilities and began to ship compacted products to the introductory group of retailers including Target. The first compacted P&G detergents reached store shelves by the end of the month. Over the first few weeks of the launch, the North America Laundry Care team and IDS had difficulty collecting data to measure the consumer response to the new formulations. The usual data sources, scanner data from large retailers and Nielsen, were difficult to interpret. Many retail outlets still had inventory of the non-compacted detergent, so customers were still able to purchase the old formulations in some stores. At the same time, several competitors introduced compacted versions and it was not always clear which UPC codes were associated with the more concentrated detergents. To get a clearer picture of the market, Torres sent teams to stores across the country to monitor product availability and consumer purchases. By the end of April, IDS compiled data that provided a clearer picture of the consumer response. On the screens of the Business Sphere, Wright presented the surprising increase in sales to Torres and the North America Laundry Care leadership team. Total category sales in the stores covered by Wave 1 increased by slightly above 2% over the same period the year prior. Powder laundry detergent sales jumped 8% as customers increased purchases and stemmed the shift from powder to liquid. Sales of powdered Tide, Gain, Cheer and other P&G laundry detergent brands improved by 12% and P&G gained a couple of percent market share in the powder segment. In comparison, the laundry 1 increased by slightly above 2% over the same period the year prior. Powder laundry detergent sales jumped 8% as customers increased purchases and stemmed the shift from powder to liquid. Sales of powdered Tide, Gain, Cheer and other P&G laundry detergent brands improved by 12% and P&G gained a couple of percent market share in the powder segment. In comparison, the laundry detergent sales at retailers that were not part of Wave 1 showed no growth during that time and P&G market share was virtually unchanged. Forecasting the Impact of P&G's Compaction Rollout Torres congratulated his team on the successful implementation in Wave 1 and then quickly focused them on the future. Raw material orders and production plans for Wave 1 had to be set for the next few months. Preparations for Wave 2 were already underway; upgrades to the manufacturing plants had begun and the first shipments were expected in less than two months. Wave 3 was scheduled for August, meaning compacted products had to start shipping to the final set of retailers in July. The forecasts that had been produced by IDS before the start of Wave 1 showed the category achieving 1% annual growth. Updated with the results of March and most of April, the statistical forecasting models produced slightly higher forecasts for Wave 1 and showed no change for Wave 2 and Wave 3. Wright explained to the North America Fabric Care leadership team that the statistical models did not account for the disruptive changes in the market. The models for Wave 1 responded to what seemed to be an unanticipated increase in market volumes and P&G market share, uninformed of the introduction of compacted detergents. In addition, the models were not built to incorporate Wave 1 results into the forecasts for Wave 2 and Wave 3; therefore, the statistical forecasts for those groups of retailers did not contain any adjustments for the planned compaction launches. The disruptive change and impact of compaction could not be ignored and Torres wondered if he should override the statistical forecasting models and make adjustments to the forecasts. But he was not sure what adjustments to make even if he decided to do so. Would the increase in the overall market and P&G's market share be sustained in the Wave 1 retailers? Or was it a temporary effect of the shift to compaction? Would similar results be seen in the other waves? A change in forecast had a much broader impact than just a modification to the North America Fabric Care annual plan. The forecasts were available to all through the Decision Cockpit and a significant modification would draw the attention of several groups. Each additional 1% increase in powder laundry detergent sales improved P&G revenue by over half a million dollars per month. A 10% increase would result in $65 million in annual top-line gains and surely be noticed by the finance team and company leadership. The production plants would have to produce an additional 35,000 boxes containing 275,000 pounds of compacted detergent per month to supply each 1% increase. The procurement, manufacturing, and supply chain teams were already under stress from the changes required to produce and deliver the new formulation. If the forecasts were not changed but results increased, P&G would be unable to meet demand and could damage relationships with retailers and customers. On the other hand, an overly aggressive forecast would leave manufacturing with excess raw material, workers and inventory. Torres understood that the implications could be even greater. If compaction led to substantial market growth and share gains, then P&G should speed up the planned North America roll-out and look to make the change in all of P&G's markets worldwide. With the team sitting silently at the oval table of the Business Sphere, Torres flashed a smile at Julia Wright, his embedded IDS analyst, and asked for her expert opinion. Wright smiled back and about what Exhibit 1 P&G Revenue and Profit by Business Unit Revenue by Division ($,M) FY2010 FY2011 Beauty 19,258 14,955 Net Margin 13.3% 14.5% Grooming 7,864 6,103 Net Margin 20.6% 22.4% Health Care 11,493 9,084 Net Margin 16.2% 16.0% Fabric Care and Home Care 25,570 19,951 Net Margin 13.9% 12.7% Baby Care and Family Care 14,736 11,550 Net Margin 13.9% 13.0% Corporate and Other -1,354 -990 Total 77,567 60,653 Net Margin 16.4% 15.2% Note: Fiscal Year ends June 30. Source: P&G Financial Reports. Exhibit 2 P&G Organizational Structure Dimitri Panayotopoulos Vice Chairman, Global Business Units Bob McDonald President & CEO Werner Geissler Vice Chairman, Global Operations. Filippo Passerini Group President, GBS & CIO Corporate Accounting Beauty & Grooming Asia Fabric Care Beauty Grooming Health Care and Baby Care and Home Care Family Care Latin America Household Care North America Corporate Strategy Global Western Europe Business Services Employee Services Accounting .IDS Legal Facilities CEE & MEA Governance Global Business Units (GBUS) Market Development Organizations (MDOS) | Global Business Corporate L Services (GBS) IL Functions Source: Casewriters. Exhibit 3 GBS Services Employee Services Employee Services People Management Facilities Computers & Communications Meeting Services Travel Services Business Services Strategic Sourcing & Procurement Financial Services & Solutions Product Innovation Supply Network Solutions Consumer Solutions Customer Solutions Initiative Management Business Performance Solutions Source: P&G. Exhibit 4 Decision Cockpit Fie Edt View Favorites Took Addrem gbs http://decisioncockpit pg.com/shrley decision cockpits My Cockpit Alerts My Reports Microsoft Internet Explorer Shipments Quick Overview Choose Region Global NA Daily O&S Report My Links NA MOO Scorecard Source: P&G. Decision Cockp GM Net CEMEA MO CAM Actual Actual Target Achaal Target Actual Targe LAM SRAP Actual Target Actual | Target Projected | Target NA Market MeasurementControl Chart Competitive Intelligence My News Stand Folders Go Exhibit 5 Business Sphere Conference Room Source: P&G. gbs (S,M) 10,000 9,000 8,000 7,000 6,000 5,000 4,000 3,000 2,000 1,000 0 US Canada 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 Source: Euromonitor. Global Market Information Database. Exhibit 6b US Laundry Detergent Value Share by Detergent Type 100% 80% 60% 40% Liquid Detergents Powder Detergents 2008 2009 2010 Other 20% 0% 2006 2007 2008 2009 2010 Exhibit 7 US Laundry Detergent Value Share by Company and Brand 2010 45% 40% 35% 30% 25% 20% 15% 10% 5% 0% Brand: Tide Gain Cheer Other P&G Arm & Xtral Hammer All Other Sun Purex Other Company: Procter & Gamble Church & Dwight Sun Products Dial Other Source: Euromonitor. "Laundry Care in the US," May 2012. CONCENTRATED use 1/3 less menos 40 LAVADAS 40 LAVADAS Dreft Source: P&G. Tide SAME LOADS LESS PACKAGING P&G FUTURE FRIENDLY cheer SNOW IVORY brightCLEAN GAIN Original

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts