Answered step by step

Verified Expert Solution

Question

1 Approved Answer

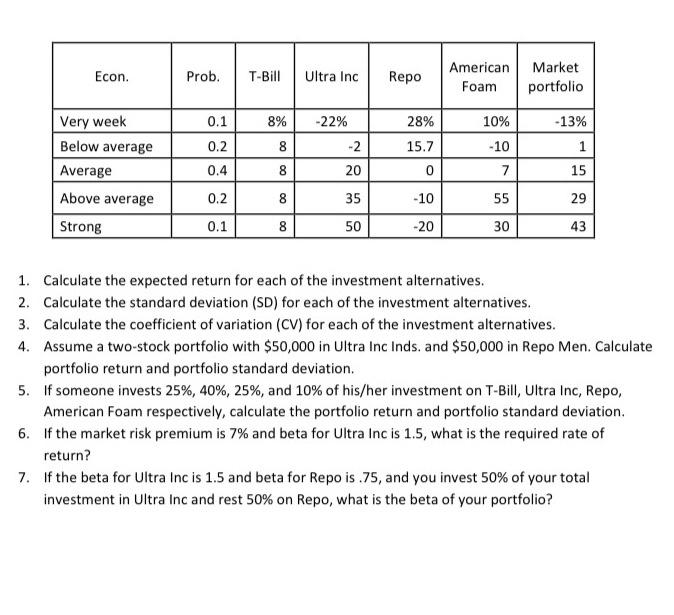

Econ. Prob. T-Bill Ultra Inc Repo American Foam Market portfolio 0.1 8% -22% 28% - 13% 0.2 8 -2 15.7 Very week Below average Average

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Collateralized Debt Obligations A Moment Matching Pricing Technique Based On Copula Functions

Authors: Enrico Marcantoni

1st Edition

365804845X,3658048468