Answered step by step

Verified Expert Solution

Question

1 Approved Answer

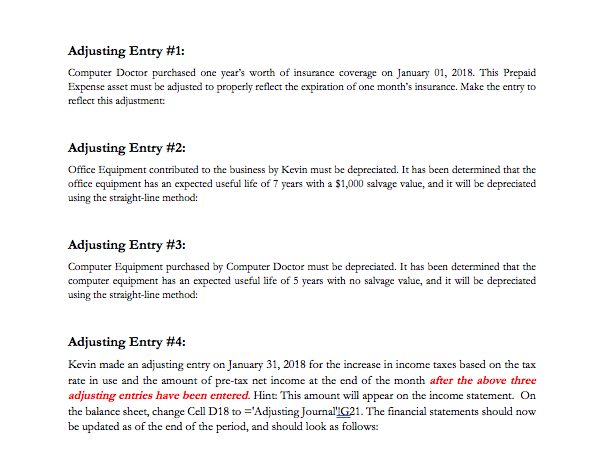

Enter Adjusting Journal entries Adjusting Entry #1: Computer Doctor purchased one years worth of insurance coverage on January 01, 2018. This Prepaid reflect this adjustment:

Enter Adjusting Journal entries

Adjusting Entry #1: Computer Doctor purchased one years worth of insurance coverage on January 01, 2018. This Prepaid reflect this adjustment: Adjusting Entry #2: Office Equipment contributed to the business by Kevin must be depreciated. It has been determined that the office equipment has an expected useful life of 7 years with a $1,000 salvage value, and it will be depreciated using the straight-line method: Adjusting Entry #3: Computer Equipment purchased by Computer Doctor must be depreciated. It has been determined that the computer equipment has an expected useful life of 5 years with no salvage value, and it will be depreciated using the straight-line method: Adjusting Entry #4 Kevin made an adjusting entry on January 31, 2018 for the increase in income taxes based on the tax rate in use and the amount of pre-tax net income at the end of the month after the above three adjusting entries have been entered. Hint: This amount will appear on the income statement. On the balance sheet, change Cell D18 to -Adjusting Journal G21. The financial statements should now be updated as of the end of the period, and should look as follows: Adjusting Entry #1: Computer Doctor purchased one years worth of insurance coverage on January 01, 2018. This Prepaid reflect this adjustment: Adjusting Entry #2: Office Equipment contributed to the business by Kevin must be depreciated. It has been determined that the office equipment has an expected useful life of 7 years with a $1,000 salvage value, and it will be depreciated using the straight-line method: Adjusting Entry #3: Computer Equipment purchased by Computer Doctor must be depreciated. It has been determined that the computer equipment has an expected useful life of 5 years with no salvage value, and it will be depreciated using the straight-line method: Adjusting Entry #4 Kevin made an adjusting entry on January 31, 2018 for the increase in income taxes based on the tax rate in use and the amount of pre-tax net income at the end of the month after the above three adjusting entries have been entered. Hint: This amount will appear on the income statement. On the balance sheet, change Cell D18 to -Adjusting Journal G21. The financial statements should now be updated as of the end of the period, and should look as followsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

New Markets Tax Credit IRS Audit Technique Guide

Authors: Internal Revenue Service

1st Edition

1304112896, 978-1304112897