Answered step by step

Verified Expert Solution

Question

1 Approved Answer

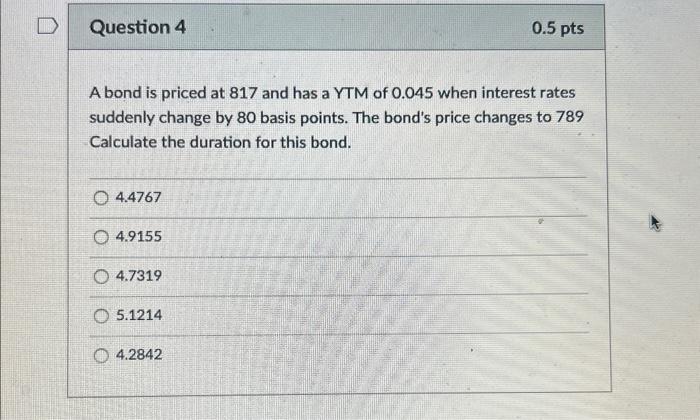

EOM L11 A bond is priced at 817 and has a YTM of 0.045 when interest rates suddenly change by 80 basis points. The bond's

EOM L11

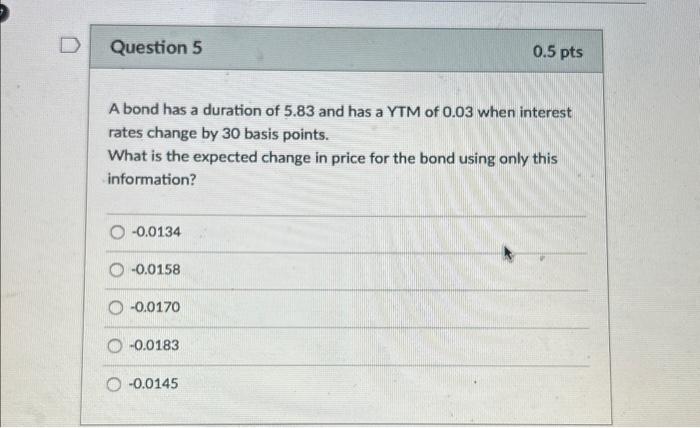

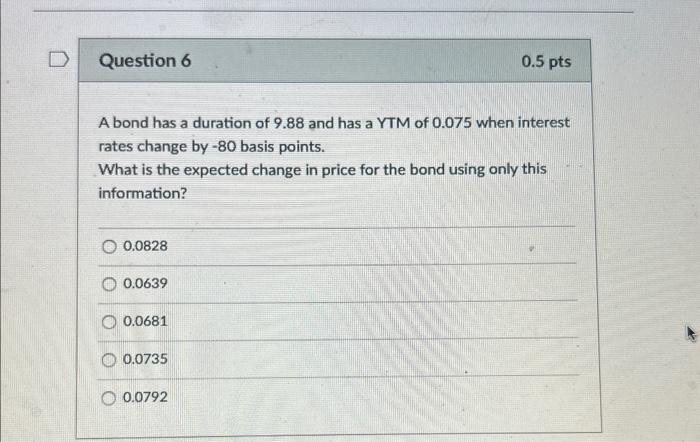

A bond is priced at 817 and has a YTM of 0.045 when interest rates suddenly change by 80 basis points. The bond's price changes to 789 Calculate the duration for this bond. 4.4767 4.9155 4.7319 5.1214 4.2842 A bond has a duration of 5.83 and has a YTM of 0.03 when interest rates change by 30 basis points. What is the expected change in price for the bond using only this information? 0.0134 0.0158 0.0170 0.0183 0.0145 A bond has a duration of 9.88 and has a YTM of 0.075 when interest rates change by -80 basis points. What is the expected change in price for the bond using only this information? 0.0828 0.0639 0.0681 0.0735 0.0792 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Developments In Entrepreneurial Finance And Technology

Authors: David B. Audretsch, Maksim Belitski, Nada Rejeb, Rosa Caiazza

1st Edition

1800884338,1800884346